The Two Most Dangerous Months 07-29-16

Since I was traveling on vacation last week, and did not write a weekly report, I want to use this opportunity to update the previous analysis and model positioning for the current environment. This is particularly important as we enter into what has historically been two of the most dangerous months of the year.

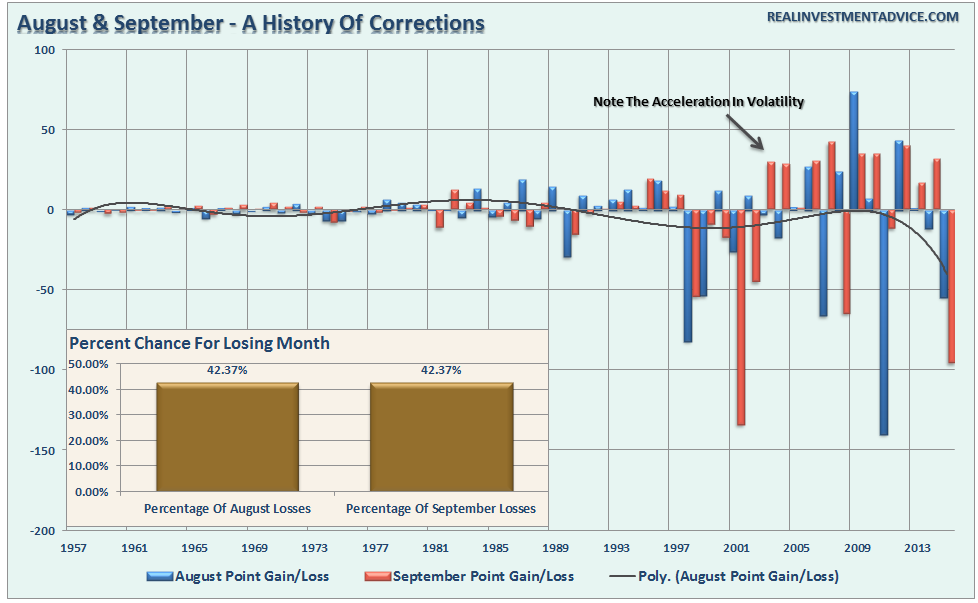

First, why do I say that? The chart below shows the historical return patterns by month for the S&P 500.

The months of August and September have a higher rate of corrections than other months with both standing at 42.37%. Furthermore, the rise of computerized trading, as shown in the chart above, has led to a substantial increase in volatility of point gain/loss during these two months. However, notice the polynomial trend line has trended more negatively in recent years reinforcing my concerns heading into the next two months.

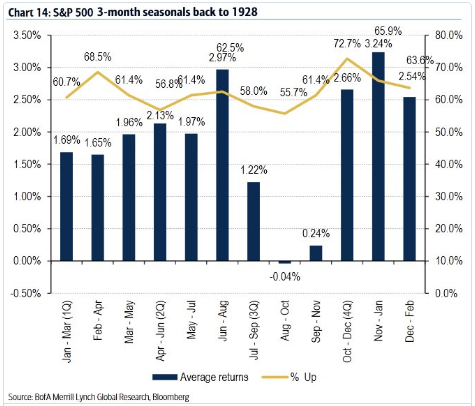

Then there is this tidbit:

We’re about to step into seasonality ditch: lowest 3-month returns Aug-Oct for S&P going back to 1928

source: BoA ML pic.twitter.com/Q5S5JSQdvr

— Babak (@TN) July 29, 2016

It is not just historical statistics that suggest caution, but primarily it is the current extension of the market itself. As I discussed two weeks ago:

“This week, I am adjusting the model allocations up to 75%. Review last week’s missive for the individual sector analysis for recommendations leading up to the model change.”

“However, while I am changing the model, this does not mean going out and clicking the “buy” button on everything you can find. We must now wait for the right entry point to increase equity allocations to the new model weights.

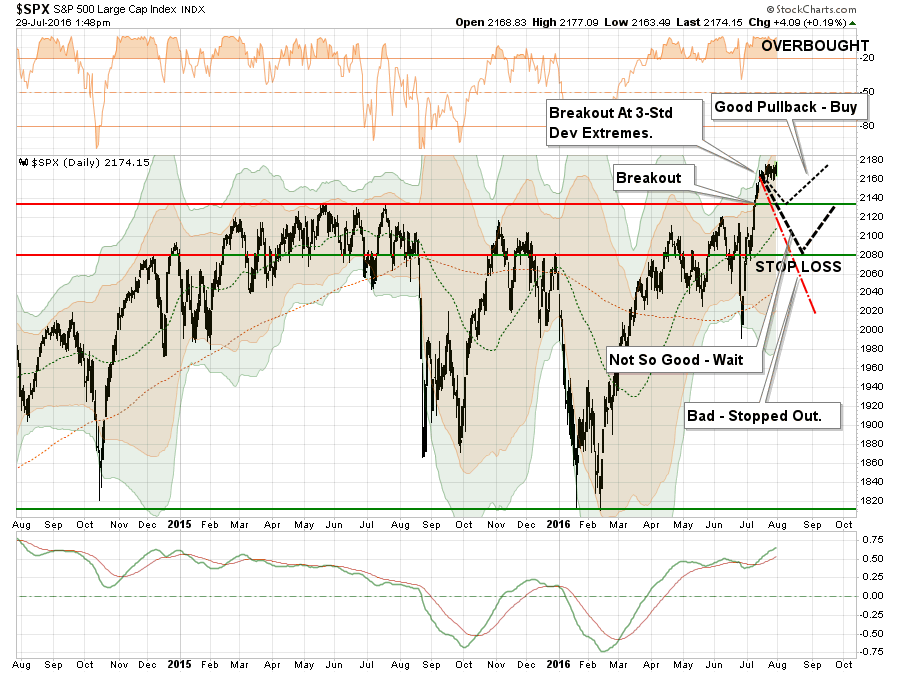

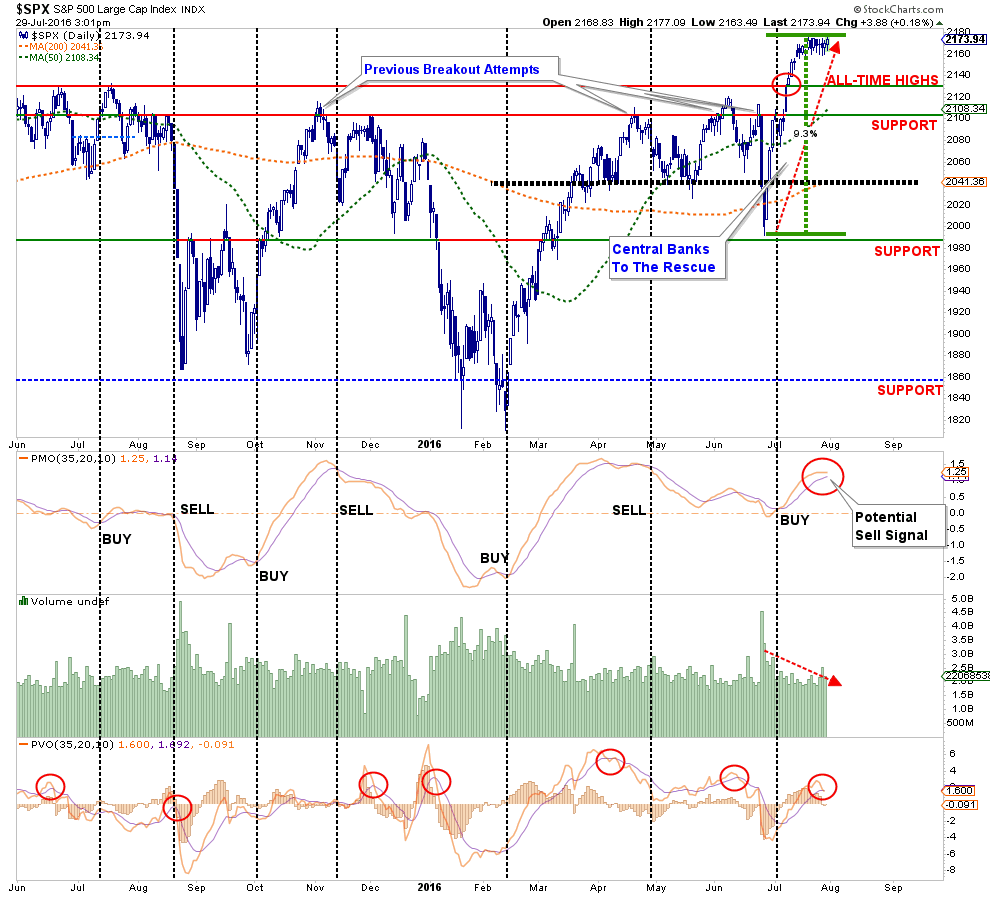

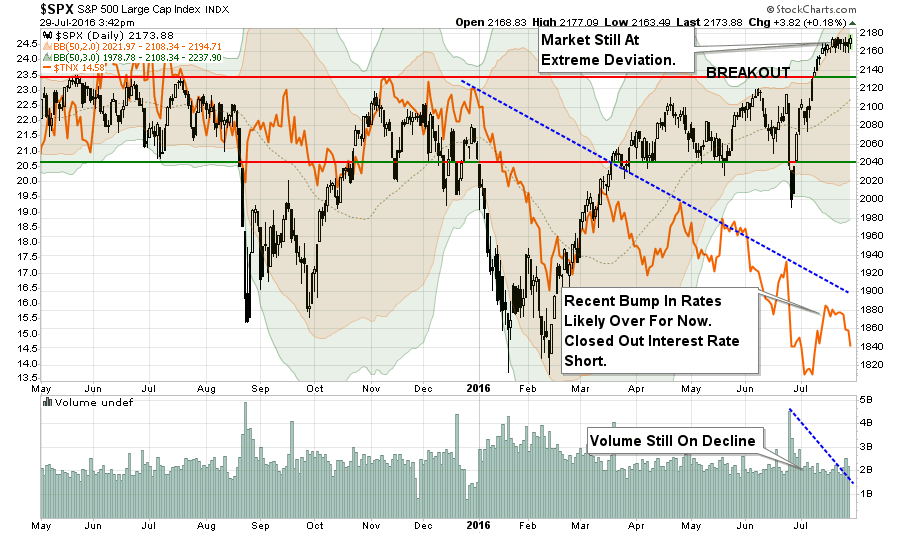

As shown below, the market is currently 3-standard deviations above its 50-day moving average. This is “rarefied air” in terms of price extensions and a pullback is now necessary to provide a better entry point for increasing equity allocations.”

Chart Updated Through Friday

The consolidation over the past week did pull the deviation back from 3-standard deviations above the 50-dma to just 2-standard deviations. This didn’t solve much of the problem as of yet.

Importantly, there are two ways to solve an overbought and overextended market advance. The first is for the market to continue this very tight trading range long enough for the moving average to catch up with the price.

The second is a corrective pullback, which is notated in the chart above. However, not all pullbacks are created equal.

- A pullback to 2135, the previous all-time high, that holds that level will allow for an increase in equity allocations to the new targets.

- A pullback that breaks 2135 will keep equity allocation increases on “HOLD” until support has been tested.

- A pullback that breaks 2080 will trigger “stop losses” in portfolios and confirm the recent breakout was a short-term “head fake.”

The next chart shows the 9.3% advance from the “Brexit” low. The momentum “buy” signal was triggered fairly early in the advance along with an upturn in volume. However, both of those indicators are now beginning to turn lower which would also suggest that a corrective action is likely in store in the days or weeks ahead.

Note that while the technical model has suggested an increase in equity exposure currently, that increase is DEPENDENT on whether the recent breakout is confirmed by a corrective action that does not violate OR reverse the current trend. There is a decent probability that such could occur, so we wait for the market to dictate our next portfolio moves.

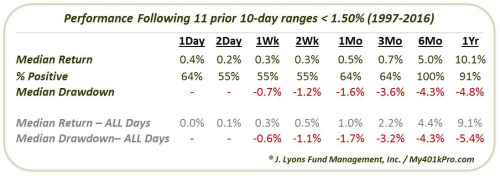

Furthermore, my friend Dana Lyons recently made some excellent comments on the extremely tight trading range as of late. To wit:

“It is particularly noteworthy considering the fact that, after today’s trading, the S&P 500 is exhibiting its 2nd tightest 10-day trading range ever.

Specifically, we looked at the prior occasions since 1997 that saw the S&P 500 trade in a range of less than 1.50% over a 2-week period. As it happens, there have been 11 such prior tight ranges since 1997, all occurring since 2005.”

“If you look carefully at the last 4 occurrences (prior to this one), it appears that each of them ran into some trouble almost immediately. Indeed, following tight ranges on 7/31/2013, 1/10/2014, 9/11/2014 and 12/8/2014, the S&P 500 experienced 1-month drawdowns of -3.3%, -5.5%, -4.6% and -4.3% respectively. Therefore, if there is something to the notion that more recent precedents are the most relevant to present circumstances, this tight range may be a bit of a red flag in the near-term.

(Btw, if you’re wondering – like we usually do – about the performance following these tight ranges when the S&P 500 is trading close to a 52-week high, don’t bother. As it turns out, these ranges occur almost exclusively near highs. For example, since January 1995, all 42 days showing a 10-day range of < 1.50% occurred within 3% of a 52-week high.)“

As I warned last time:

“There is also a possibility this central bank driven liquidity push is a giant ‘trap’ waiting to be sprung on unwitting investors.

The current rally is built on a substantially weaker fundamental and economic backdrop. Therefore, it is extremely important to remember that whatever increase in equity risk you take, could very well be reversed in short order due to the following reasons:

- We are moving into the latter stages of a cyclical bull market.

- Economic data continues to remain weak

- Earnings are only positive by not sucking as bad as estimates

- Volume is weak

- Longer-term technical underpinnings remain bearish.

- It is the summer of a Presidential election year which tends to be weak.

- Share buybacks are slowing

- The yield curve is flattening

It is worth remembering that markets have a very nasty habit of sucking individuals into them when prices become detached from fundamentals. Such is the case currently and has generally not had a positive outcome.

The chart below illustrates point #5 above. There are still WAY too many negative divergences in underlying indicators to suggest an ‘all clear’ for investors currently.”

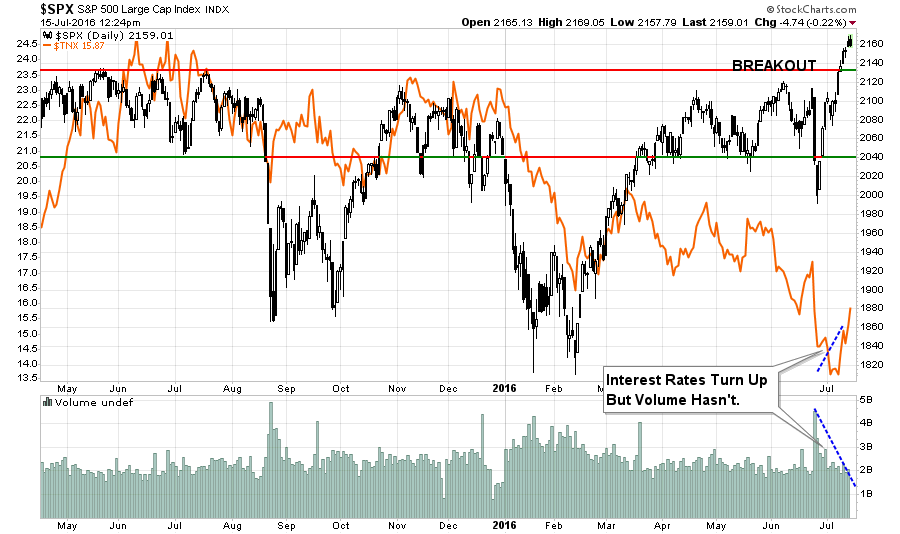

Interest Rates

I discussed previously that interest rates had gotten so oversold (bonds overbought) due to the “Brexit” that a reversal was very possible. As I noted previously, the rotation from bonds to stocks confirmed the push higher in the markets.

“Much of the sustainability of the rally going forward is dependent upon the ongoing rotations from ‘safety’ back into ‘risk.'”

This was the chart I posted at that time as I disclosed that I had taken a “short position” on interest rates using the exchange-traded fund (TBT).

Given the strength of the run-up in stocks which pushed into extreme overbought territory, I began discussing the potential for a short-term correction. Therefore, I closed out the short position on TBT this past Monday given that money would like reverse flows from “risk” back into “safety.”

If I am correct, and the markets do experience a short-term correction, or worse, interest rates will likely retest recent lows. One thing is for sure…“Rates ain’t going significantly higher anytime soon.”

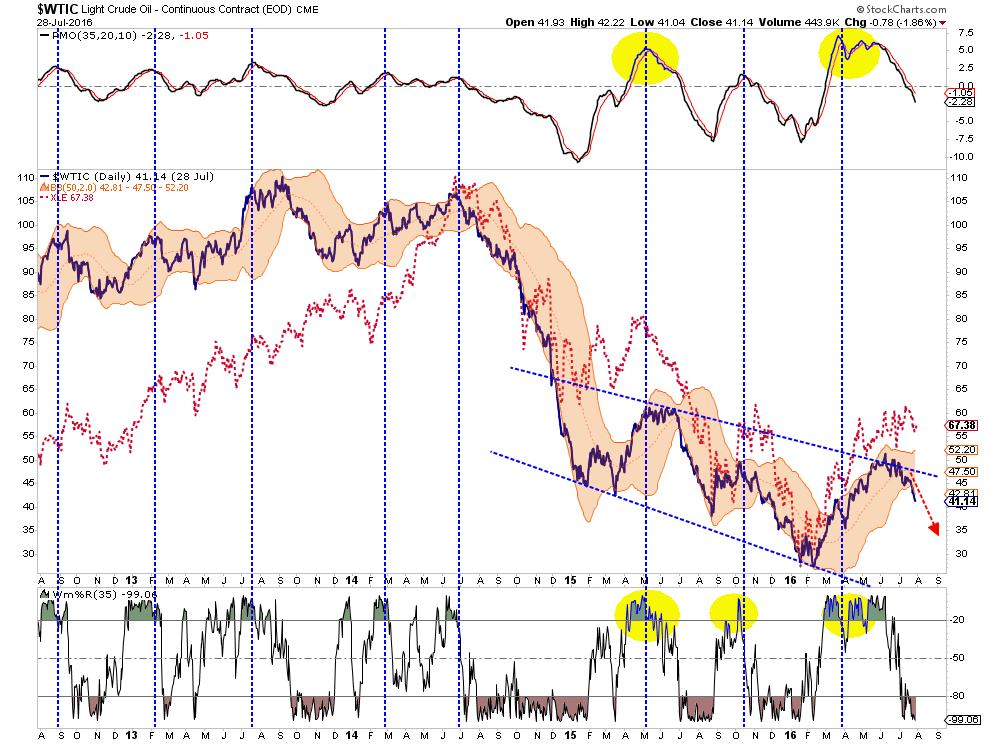

Oil & The Dollar

At the beginning of July I wrote:

“There are two things about the energy sector. While the push from the lows has been fairly strong in recent months, the ongoing downtrend remains intact. If the market does turn lower in the August/September period as expected the potential to retest lows is fairly high.

As shown in the longer term oil chart below, there is little to suggest a recovery back to old levels is in the offing anytime soon. With oil prices back to extreme overbought conditions, a retracement to $35 or $40/bbl would not be surprising particularly if, and when, the US Dollar strengthens. Remain underweight this sector as valuations for energy stocks have entered into ‘moon shot’ territory.”

That call was quite prescient as shown.

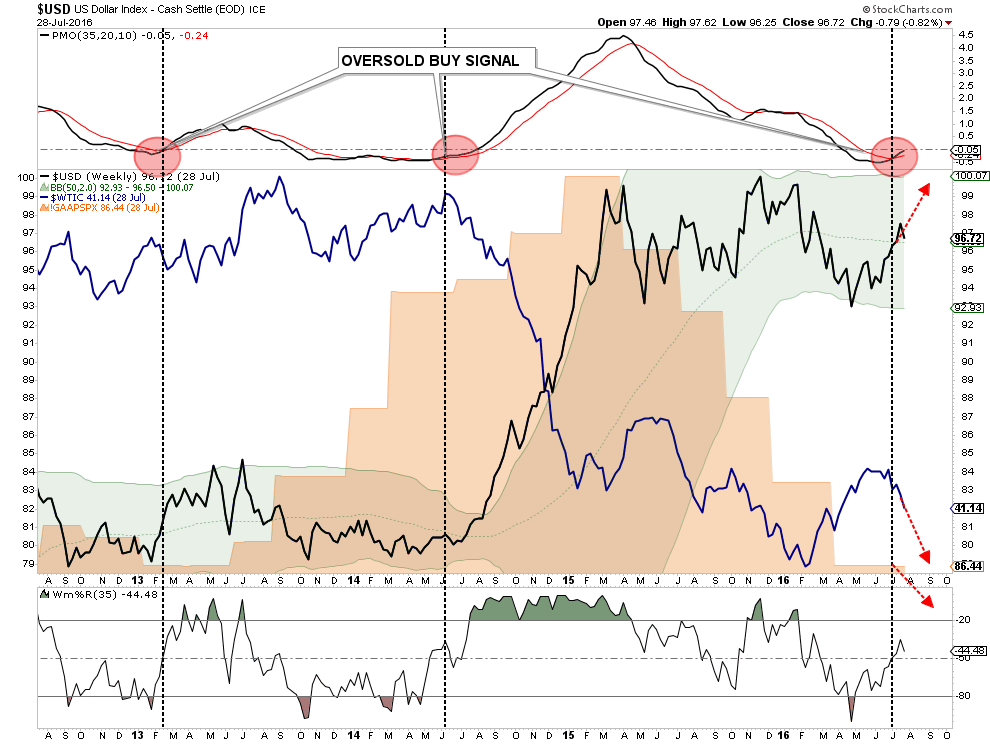

Furthermore, the rise in the dollar is likely to continue which will continue to suppress both oil prices and earnings. As noted:

“While earnings are set to decline again this quarter which will push valuations even further into the proverbial stratosphere, the real risk to watch is the US Dollar. While Central Banks have gone all in, including the BOJ with additional QE measures of $100 billion, to bail out financial markets and banks following the “Brexit” referendum, it could backfire badly if the US dollar rises from foreign inflows. As shown below, a stronger dollar will provide another headwind to already weak earnings and oil prices in the months ahead which could put a damper on the expected year-end “hockey stick” recovery currently expected. “

Unlike the stock market which is pushing extreme overbought levels, the dollar is at an extreme oversold condition and has only started a potential move higher. This is something to pay very close attention to in the months ahead.

As noted, with interest rates negative in many areas of the world, the push of capital into the U.S. for a higher return on reserves is very likely.

Quick Reminder On Taking Action

While Monday is NOT the day to go rushing headfirst into the markets, there are things that we can and should be doing to prepare for “whatever happens next.”

- Move slowly. There is no rush in adding equity exposure to your portfolio.Use pullbacks to previous support levels to make adjustments

- If you are heavily UNDER-weight equities, DO NOT try and fully adjust your portfolio to the model in one move. This could be disastrous if the market reverses sharply in the short term. Again, move slowly.

- Begin by selling laggards and losers. These positions are dragging on performance as the market rises and tend to lead when markets fall.Like “weeds choking a garden,” pull them.

- Add to sectors, or positions, that are performing with, or outperforming, the broader market.(See previous analysis for suggestions.)

- Move “stop loss” levels up to current breakout levels for each position. Managing a portfolio without “stop loss” levels is like driving with your eyes closed.

- While the technical trends are intact, risk considerably outweighs the reward. If you are not comfortable with potentially having to sell at a LOSS what you just bought, then wait for a larger correction to add exposure more safely. There is no harm in waiting for the “fat pitch” as the current market setup is not one.

- If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

What you decide to do with this information is entirely up to you. As I stated, I do think there is enough of a bullish case being built to warrant taking some equity risk on a very short-term basis give the right set up. However, we must wait and see what happens next week.

However, the longer-term dynamics remain bearish. When those negative price dynamics are combined with the fundamental and economic backdrop, the “risk” of having excessive exposure to the markets greatly outweighs the potential “reward. “

Please be careful.

Investing is not a competition.

It is a game of long-term survival.

THE MONDAY MORNING CALL

The Monday Morning Call – Analysis For Active Traders

Continue To Prepare

While we await a better entry point, assuming the recent bullish action is maintained, it is important to continue to prepare portfolios for further action.

I have often equated portfolio management to tending a garden in the past. Like a garden we must:

- Prepare the soil (accumulate enough cash to build a properly diversified allocation)

- Plant according to the season (build the allocation given the right “season”)

- Water and fertilize (add cash regularly to the portfolio for buying opportunities)

- Weed (sell loser and laggards, weeds will eventually “choke” off the other plants)

- Harvest (take profits regularly otherwise “the bounty rots on the vine”)

- Plant again according to the season (add new investments at the right time)

So, with this analogy in mind, here are the actions to continue taking to prepare portfolios for the next set of actions:

Step 1) Clean Up Your Portfolio

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Step 2) Compare Your Portfolio Allocation To The Model Allocation.

- Determine areas requiring new or increased exposure.

- Determine how many shares need to be purchased to fill allocation requirements.

- Determine cash requirements to make purchases.

- Re-examine portfolio to rebalance and raise sufficient cash for requirements.

- Determine entry price levels for each new position.

- Determine “stop loss” levels for each position.

- Determine “sell/profit taking” levels for each position.

(Note: the primary rule of investing that should NEVER be broken is: “Never invest money without knowing where you are going to sell if you are wrong, and if you are right.”)

Step 3) Have positions ready to execute accordingly given the proper market set up. In this case, we are looking for a pullback to reduce the extreme overbought condition of the market without violating any major levels of support.

IMPORTANT NOTE: Taking these actions has TWO specific benefits depending on what happens in the market next.

- If the market pulls back to support and confirms the recent breakout is indeed a continuation of the bullish long-term trend, the actions have cleared out the “weeds” and allowed for “new planting” to benefit from the next advance.

- If the recent breakout turns out to be a “head fake,” then the reduction of “risk” protects the portfolio against any substantial decline.

No one knows for sure where markets are headed in the next week, much less the next month, quarter, year, or five years. What we do know is that not managing risk in portfolios to hedge against something going wrong is far more detrimental to the achievement of long-term investment goals due to the inability to recover the “time” lost getting back to even.

This fallacy was clearly pointed out this past week in probably what ranks as the worst bit of financial analysis put out this year by Myles Udland via BI.

Okay. Let’s make a couple of real-world assumptions. Most people, by the time they enough to effectively invest and actually start doing so, is about 45 years of age. This gives them about 20-years to their retirement goal.

Here’s the problem, since most people “assume” the markets return 8% a year, a myth previously debunked here, a 26% return over 16-years is just 1.625% annually. Buying a bond fund would have yielded in excess of a 150% rate of return or 9.375% annually with substantially less volatility.

“Getting Back To Even” never has been, and never will be, a successful investment strategy.

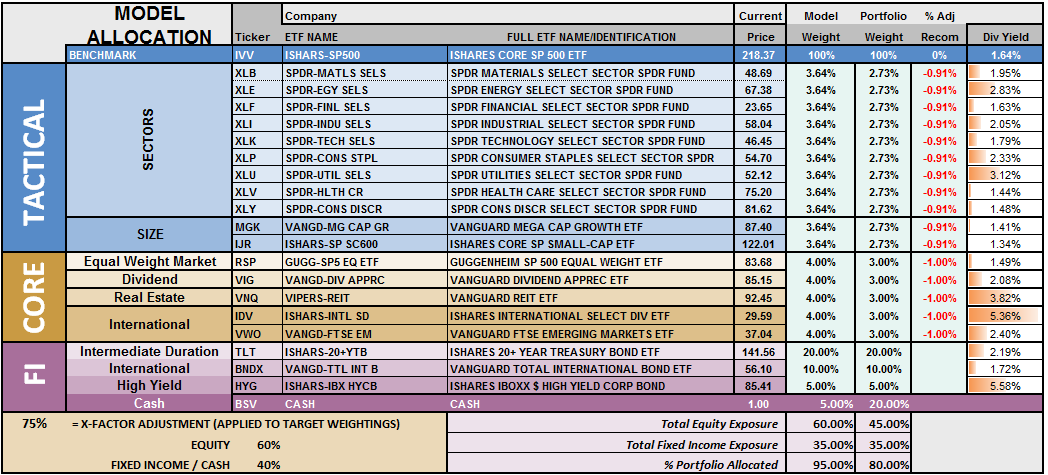

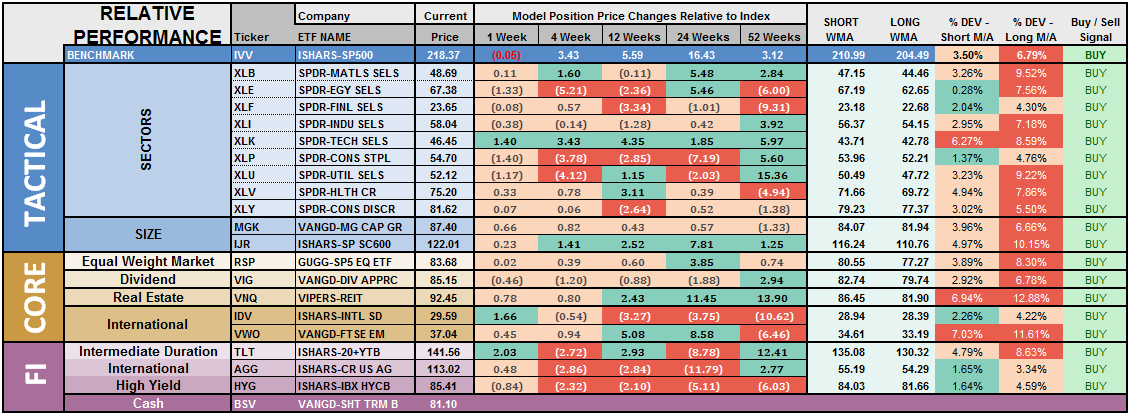

S.A.R.M. Sector Analysis & Weighting

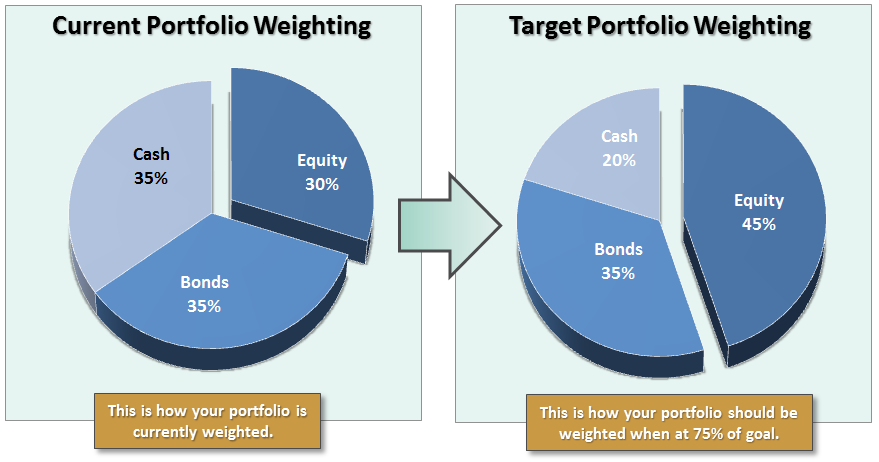

The current risk weighting remains at 50% this week but will increase to 75% given appropriate market conditions.

Again, we must be given the right “set up” to increase equity allocations. Begin by “averaging up”in existing holdings to match model allocation and weights. When, and IF, the market confirms the continuation of the “bullish trend,” then begin adding new holdings to the model.

(Note: This is an equally weighted model example and may differ from discussions of overweighting/underweighting specific sectors or holdings.)

Relative performance of each sector of the model as compared to the S&P 500 is shown below. The table compares each position in the model relative to the benchmark over a 1, 4, 12, 24 and 52-week basis.

Historically speaking, sectors that are leading the markets higher continue to do so in the short-term and vice-versa. The relative improvement or weakness of each sector relative to index over time can show where money is flowing into and out of. Normally, these performance changes signal a change that last several weeks.

The last column is a sector specific “buy/sell” signal which is simply when the short-term weekly moving average has crossed above or below the long-term weekly average. The number of sectors on“buy signals” has improved from just 2 several weeks ago to 19 this past week.

The risk-adjusted equally weighted model has been increased to 75%. However, as stated above, a pullback in the markets is needed before making any changes.

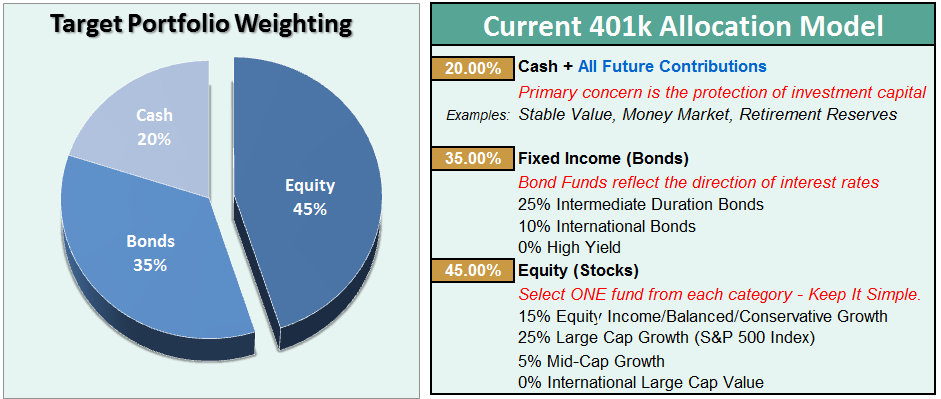

Such an increase will change model allocations to:

- 20% Cash

- 35% Bonds

- 45% in Equities.

As always, this is just a guide, not a recommendation. It is completely OKAY if your current allocation to cash is different based on your personal risk tolerance, time frames, and goals.

For longer-term investors, we still need to see improvement in the fundamental and economic backdrop to support the resumption of a long-term bullish trend. Currently, there is no evidence of that occurring.

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

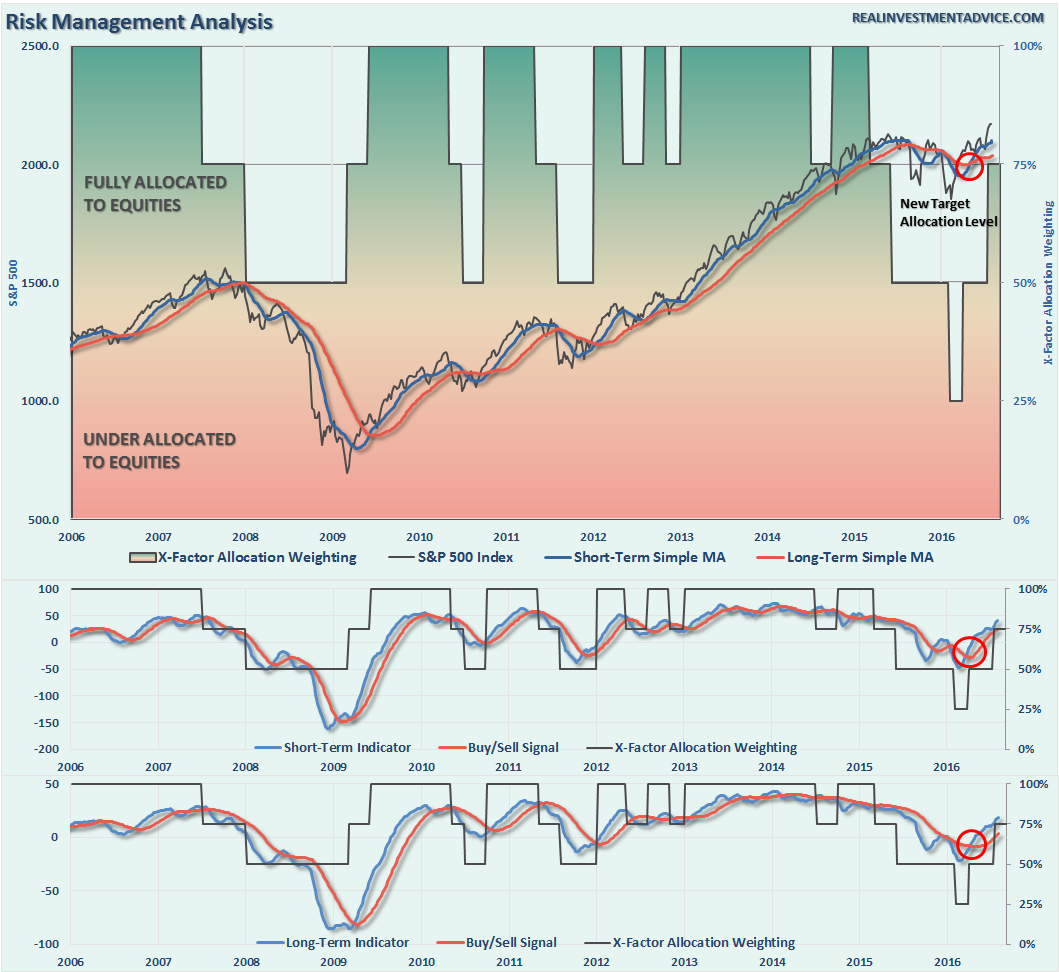

NOTE: I have redesigned the 401k plan manager to accurately reflect the changes in the allocation model over time. I have overlaid the actual model changes on top of the indicators to reflect the timing of the changes relative to the signals.

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Market Goes Nowhere, Still Waiting

As I noted last time:

“With the technical underpinnings still bullishly biased at the moment, we are now in the position to increase equity allocations over the next couple of weeks.”

However, as is always the case, by the time markets makes a significant technical change, prices are generally at an extreme overbought or oversold condition. This is the case currently with the recent breakout which has created an extreme overbought condition in the short term.

As discussed at length in the above missive, we certainly want to prepare ourselves to increase equity exposure in portfolios, however, we must patiently wait for the right conditions to apply those increases. Furthermore, while waiting for the relaxation of prices to make more prudent entries, it also enables investors to bypass potential “head fakes” of market actions.

While historically speaking, buying initial breakouts generally works to the advantage of the investor, there are plenty of precedents where breakouts marked the top of a price trend before the next major decline. Waiting to make prudent adjustments to allocations can help mitigate the risk of a false breakout.

- Review the allocation model adjustments below

- Identify the next course of actions in your 401k-plan

- Wait to make adjustments until technical conditions improve.

- Change allocations to target levels when conditions are right.

Patience remains a financial virtue.

If you need help after reading the alert; don’t hesitate to contact me.

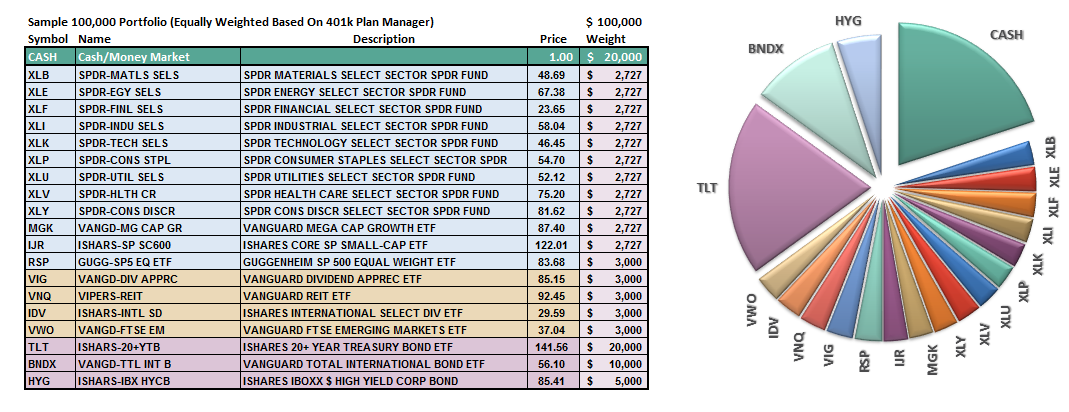

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principal. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

Comments

No Thumbs up yet!

No Thumbs up yet!