The Market Hangs Onto Support…Again

On Thursday morning, as the market dropped below its 200-dma, I got numerous emails asking about the break. I wrote the following in response:

“I have often discussed that as a portfolio manager I am not too concerned with what happens during the middle of the trading week. The reason is daily price volatility can lead to many false indications about the direction of the market. These false indications are why so many investors suggest that technical analysis is nothing more than ‘voodoo.’

For me, price analysis is more about understanding the ‘trend’ of the market and the path of least resistance for prices in the short and intermediate-term. This analysis allows for portfolio positioning to manage risk.

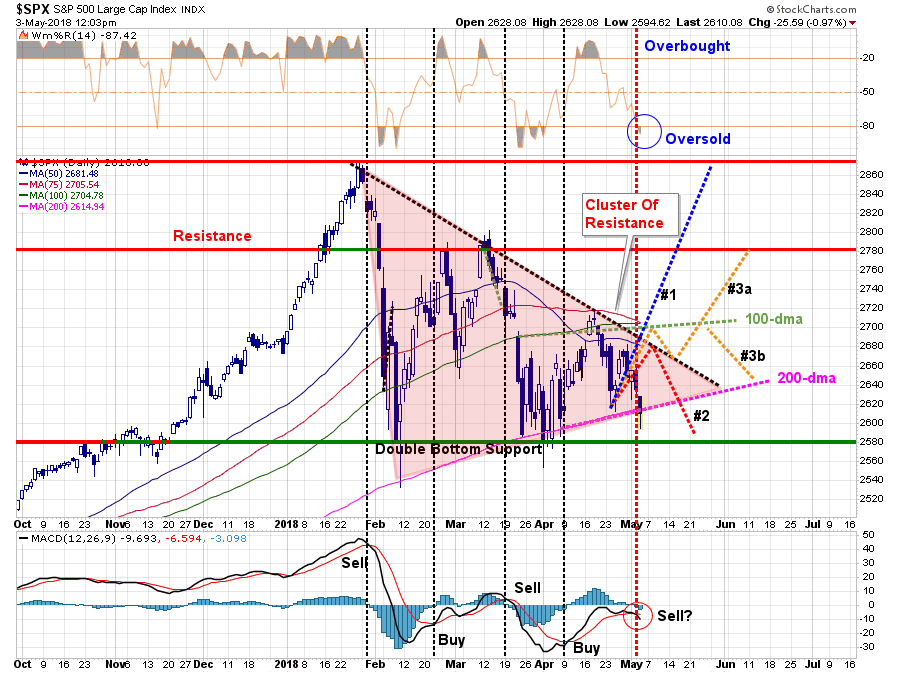

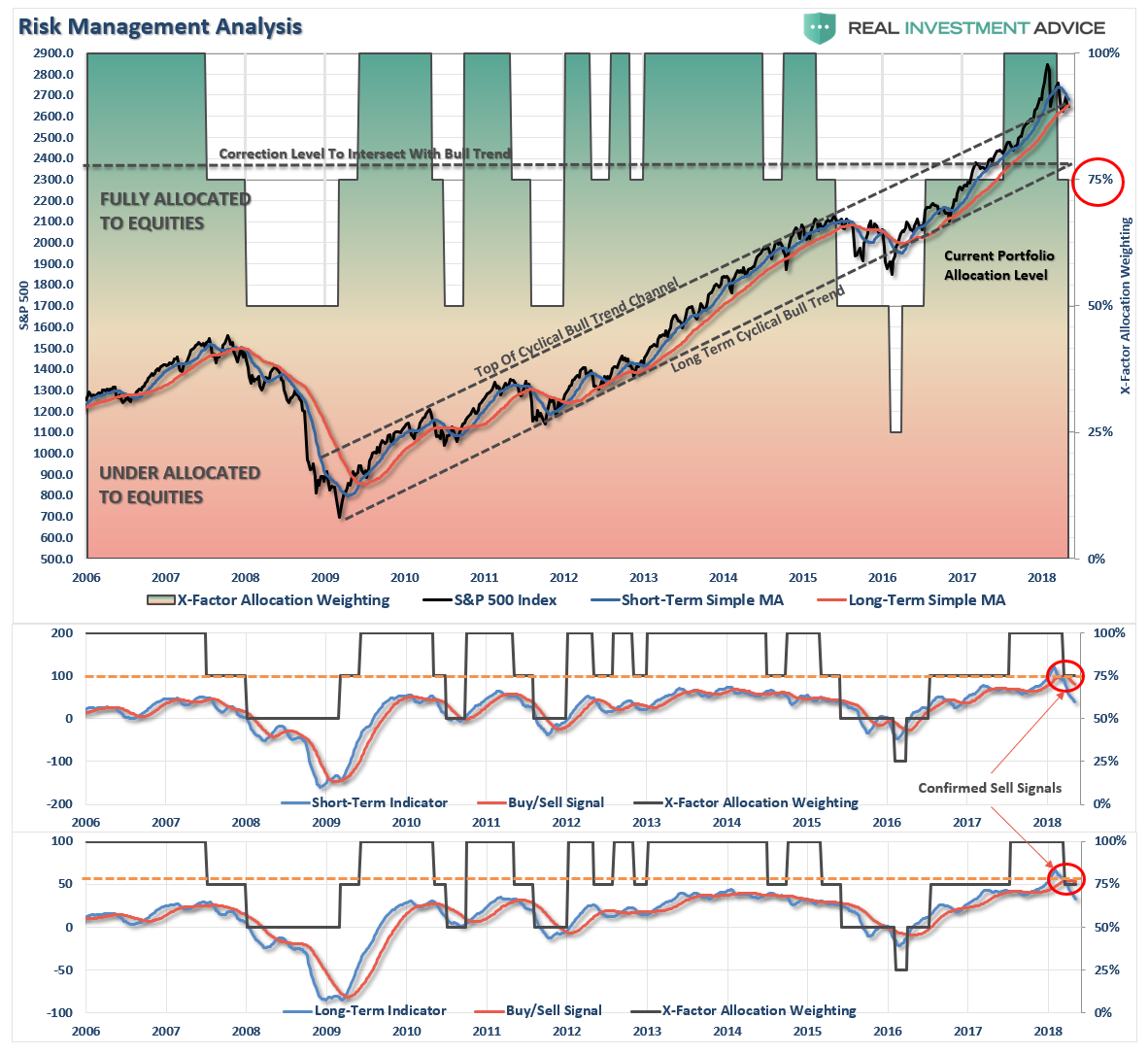

Over the last several weeks, I have been mapping out the ongoing correction in the market and have noted the important support that has been provided by the running 200-day moving average. The chart below is updated through this morning.”

“The break of the 200-dma today is not a good sign. Consolidation processes are much akin to the “coiling of a spring.”As prices become compressed, when those prices break out there is a “release of energy” from that compression which tends to lead to rather sharp moves in the direction of the breakout.

Importantly, the break of support today is NOT a signal to run out and sell everything. It is, however, a worrisome warning that should not be entirely dismissed.

As stated, nothing matters for me until we see where the market closes on Friday.”

Of course, almost immediately after posting that article, the market began to rally back and closed in the green, and above the 200-dma, thereby negating the break.

In other words, despite all the volatility, nothing changed (for better or worse) which would affect our current portfolio allocations.

So, with that said, let’s update the progress on our potential pathways from last week.

As stated, the market did defend its 200-dma and is very close to reversing its short-term “sell signal.”

That’s the good news.

The not so good news is that while the market did muster a rally on Friday, it still remains well-entrenched within the ongoing consolidation/correction process.

Interestingly, as I stated on Thursday’s radio broadcast:

“A bad employment number may actually be ‘good’ for the market. If the number comes in weaker than expected this will likely ease concerns about more aggressive Fed rates hikes which could buoy stocks.”

Not surprisingly, that is exactly what happened.

The problem is that with all the economic data coming in weaker than expected, this may well be a very short-lived rally.

In reviewing our three primary pathways above, pathway #3a and #3b remain the most viable currently. From last week’s missive:

- Pathway #1 is the most bullish of potential outcomes. With earnings continuing next week, and short-term conditions mildly oversold, the market is able to push through resistance and rally back towards old highs. (Probability = 20%)

- Pathway #2 is the most bearish with the market failing at the cluster of overhead resistance once again but this time violating the 200-dma. This decline begins a process of a deeper correction as we head into the summer months. (Probability = 30%)

- Pathway #3a and #3b suggest a further rally to the 100-dma, a pullback to the previous downtrend and then either an advance that breaks above the 100-dma and begins a more bullish rise, OR a failure and another test of the 200-dma.(Probability =50%)

Simply, we can not predict the future, we can only react to it. These pathways are educated “guesses” of where the market may trade. However, without analysis of what “might” happen, the process of portfolio management becomes nothing more than a dart throwing contest. Such tends to not work out well.

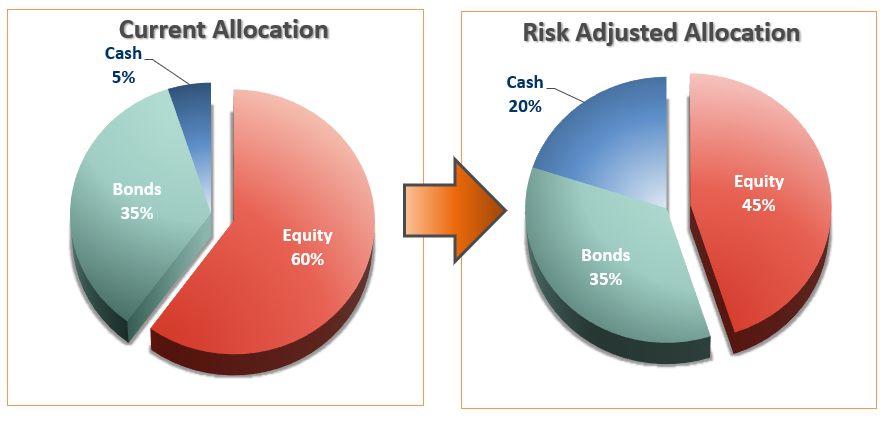

This is why we have raised cash over the last couple of months on rallies. Currently, given the backdrop of the intermediate-term outlook, updated below, there isn’t much we need to do at the moment.

However, the weakness in the market, combined with longer-term sell signals as discussed on Tuesday, still suggests the market has likely put in its top for the year.

We remain cautious and suggest the time to “buy” has not yet arrived.

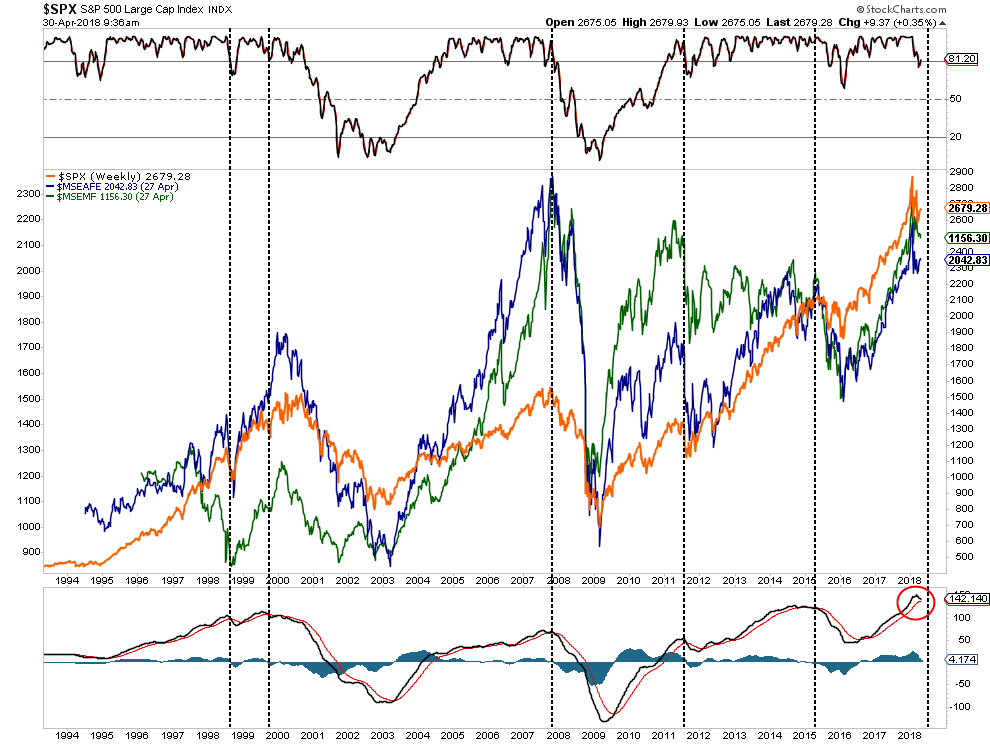

Intermediate-Term Picture Remains Bearish

On an intermediate-term basis, both of our weekly “sell signals” remain, and as shown below, despite the sharp rally on Friday, the market once again failed at its overhead trend line and closed lower for the week. Furthermore, the intermediate-term moving average has turned sharply lower and is beginning to threaten crossing below the longer-term average. This is not a good setup for a bull market continuation.

With confirmed “sell signals” still firmly intact, the easiest path for prices currently remains lower. This does not mean you can not have sharp reversal rallies from short-term oversold conditions as we saw last week, but those rallies should be used to reduce risk.

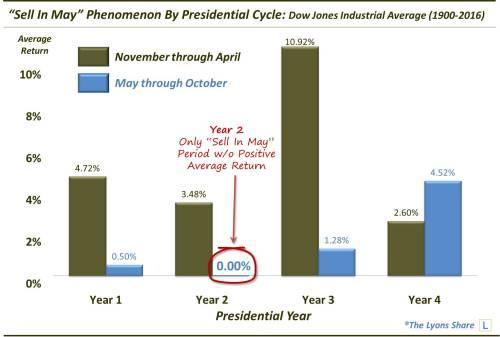

Furthermore, as we discussed last week, the “seasonally strong” period of the year has come to an end. My friend Dana Lyons made another interesting observation with reference to the Presidential cycle. To wit:

“There is some evidence to suggest that stock investors would be well served by selling in May and going away this year.

In parsing the data, however, we have found one historical trend that may suggest that the ‘Sell In May…’ advice may be better served this year than most.It is based on the (also relatively consistent) 4-year Presidential Cycle.Naturally, the average Sell In May returns are not uniform across all years. And specifically, we see dispersion, and a wide one at that, among the 4 years within the Presidential Cycle. For example, during ‘Year 4’s’, the May-October average returns actually exceed those of the November-April period.”

“It is a different story in ‘Year 2’s’, however. In fact, at +0.00%, the average May-October return during Year 2’s is the worst of any of the 4 years.”

Given the ongoing issues of “trade wars", tariffs, Russia, Syria and North Korea combined with an extraction of liquidity from both the Fed and the ECB, the risk of a policy misstep is certainly elevated. Furthermore, with the long-term weekly indicator very close to tripping a “sell-signal,” we certainly remain more cautious currently.

“Cash” remains a safety net for now.

The Fed Is Walking A Tight Rope

by Michael Lebowitz

In March 2012, Chris Cole of Artemis Capital wrote:

“Imagine the world economy as an armada of ships passing through a narrow and dangerous strait leading to the sea of prosperity. Navigating the channel is treacherous for to err too far to one side and your ship plunges off the waterfall of deflation but too close to the other and it burns in the hellfire of inflation. The global fleet is tethered by chains of trade and investment so if one ship veers perilously off course it pulls the others with it.”

At the time the letter was written, the most pressing concern for the global economy was clearly the “waterfall of deflation.” Now consider the actions of the Federal Reserve (Fed) since December 2015. They have raised the Fed Funds rate five times and more recently began reducing their balance sheet, aka quantitative tightening (QT). In measured fashion, they expect to continue both sets of actions which will progressively reduce financial liquidity for the foreseeable future.

The removal of stimulus despite economic growth and inflation that is well within the range of the last five years raises important questions about the Fed’s objectives.

Some will say that the Fed is concerned that inflationary pressures are building as witnessed by some corporate earnings comments and economic surveys. Others claim that the large fiscal deficits and tax reform are likely to provide a boost in the near future to economic growth and inflation and that their actions are pre-emptive. While we acknowledge the possibility for an uptick in inflation, we think the main factor driving the Fed is the normalization of policy, both interest rates, and balance sheet, to provide them monetary ammunition for when it is needed next. Said differently, they are looking beyond the current economy with an eye toward the next recession. As Chris Cole so graphically illustrated, however, the strait through which the global armada of ships now sail may appear less treacherous, but the reality is that accumulating global debt is actually guiding the fleet into even more treacherous waters.

Damned if they do– If the Fed’s overarching goal behind recent policy is normalization, they run the risk of stamping out the recent uptick in economic growth and inflation. Given the $70 trillion of government, consumer, and corporate debt, interest rates are economically more important today than any time in the past. As such, each step higher in interest rates and reduction in balance sheet increases the sensitivities to debt and therefore reduces economic activity.

Damned if they don’t– The flip side of the argument is that if they do not increase rates and reduce their balance sheet, they run the risk that recent fiscal stimulus and dollar weakness will stoke inflation. While the Fed has a 2% inflation goal, letting inflation rise much beyond 2% would also impose upward pressure on interest rates and harm economic activity.

On her way out, Janet Yellen assured us the pace of Fed tightening would be “gradual and predictable.” Mrs. Yellen seemed to understand the risks of moving too fast or too slow as summarized above but it was always couched in terms of the threat of derailing the recovery. What her analysis seems to have neglected was a long-forgotten scenario that has precedent in U.S. economic history.

The biggest risk may not necessarily be slowing growth or higher inflation but the combination of both, otherwise known as stagflation. Such an environment is a worst-case scenario for the Fed where debts are harder to service due to higher rates combined with weaker wages, tax base, and corporate earnings. Stagflation would not only increase credit defaults but put significant pressure on stock prices and other risky assets that stand at elevated valuations based on low-interest rates. Perhaps most importantly, that scenario would greatly limit any ability of the Fed to intervene if the market swoons.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

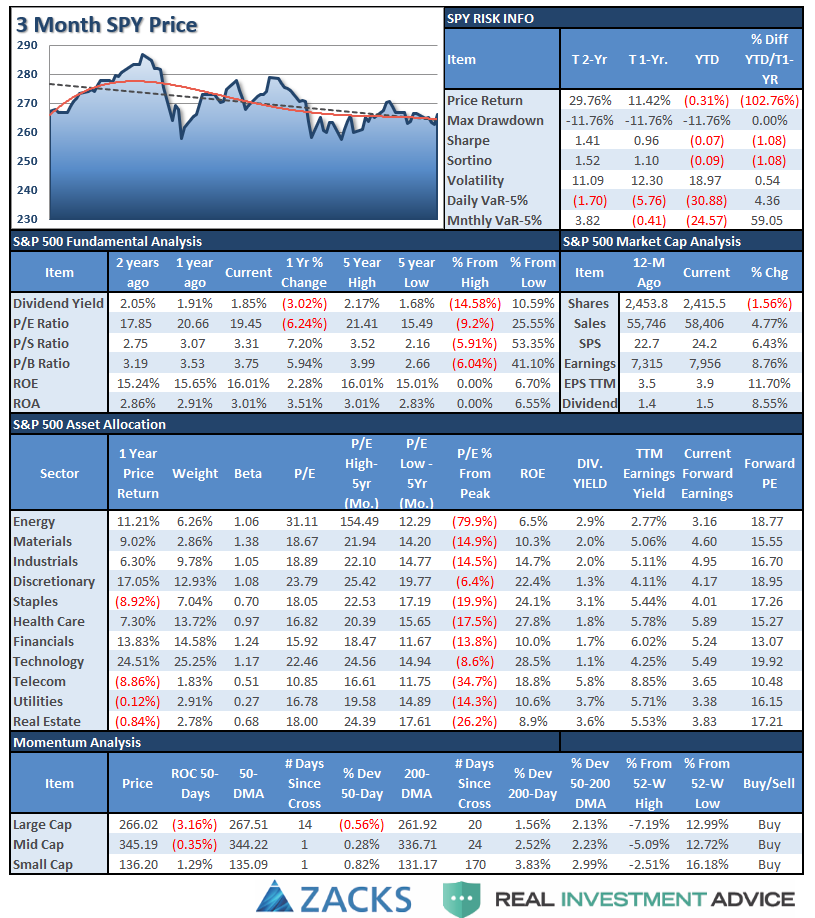

S&P 500 Tear Sheet

Performance Analysis

ETF Model Relative Performance Analysis

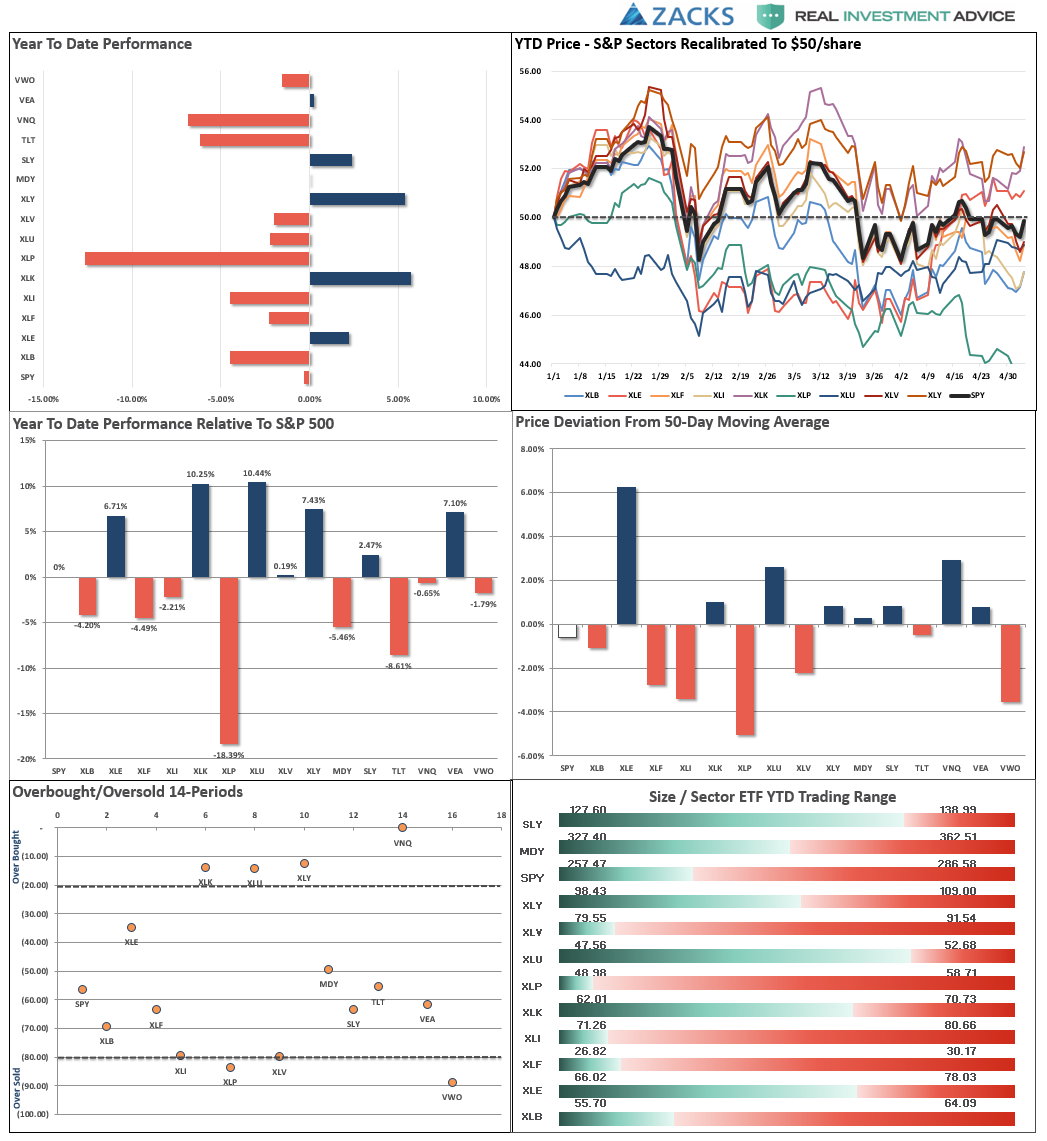

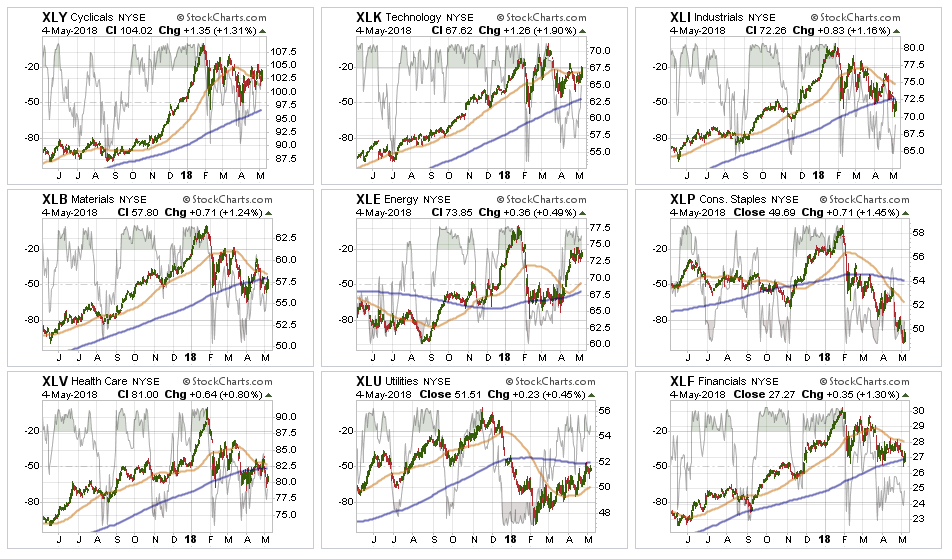

Sector & Market Analysis:

The action this past week has turned the very short-term trading “buy” signal almost to a “sell” had it not been for the sharp rebound on Friday. However, with the market still on longer-term “sell” signals, remaining below important resistance and still contained in a downtrend, any rally next should continue to be used for raising cash and reducing portfolio risk.

Discretionary, Technology, Energy are the only three sectors actually above their respective 50-dma currently., but just barely. Overall action in these sectors, while they are leading, has been very weak. As stated last week, the parabolic surge higher in Energy stocks faded and the advice to take profits remains this week as well.

Materials, and Industrials – we closed out of our positions in these two sectors earlier this year as “trade war” talk begin to gain momentum. With that threat still present, plus higher borrowing and energy costs, there is more downside risk currently. We remain watchful for a potential entry point, but with both sectors below their 200-dma we will sit on the sidelines and watch for now.

Financials and Health Care continue to lag on a relative performance basis and both sectors are threatening a break of their consolidation support. We are moving stops up to recent lows and remain cautious and underweight relative to normal positioning.

Staples – after completely falling apart after a rally back to the 50-dma, the rotation from “risk” back into “safety” late last week gave the sector a bounce. There is likely an opportunity being formed currently, but it will take some more time to develop first. More importantly, the sector speaks much more broadly about the real health of the economy. Pay attention to the message.

Utilities have significantly picked up performance in recent weeks and have broken back above the 50-dma. We are not recommending adding to the position yet as the moving-average crossover remains negative and the sector remains below its 200-dma. However, performance is improving. Like Staples, the rotation from “risk” to “safety” last week is much more indicative of concerns about overall market risk.

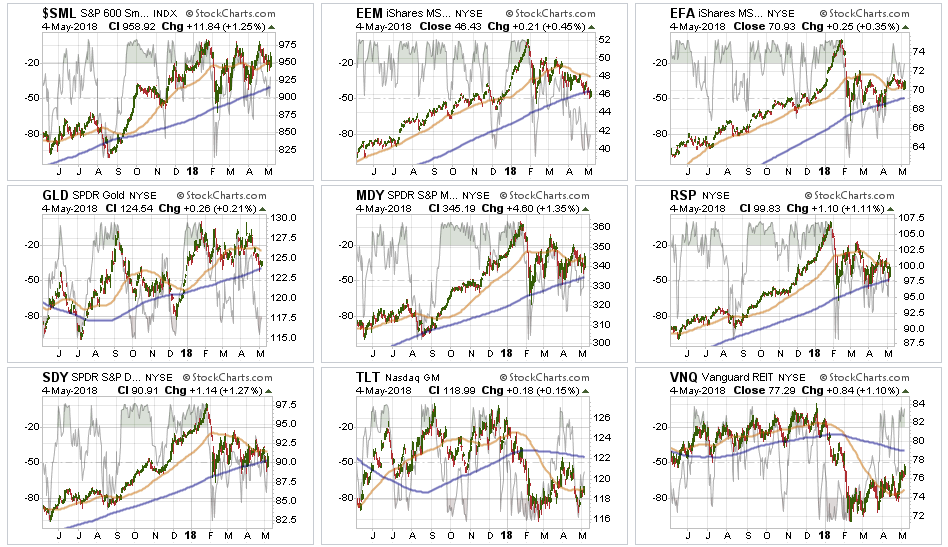

Small Cap, Mid Cap, and International indices all pushed back above their 50-dma but continue to struggle with multiple tops. This is particularly the case with Small-caps which have put in a triple top, Mid-cap is continuing to build a downtrend as well as International. Remain patient at the moment.

Emerging Markets continue to struggle and broke below its 200-dma this past week. The index is also beginning to flirt with important support, a break of which will lead to more significant declines. Despite all of the “poor analysis” of how “emerging markets are cheap relative to the U.S.,” as I penned last week, they are simply a reflection of U.S. consumption and economic trends. “If the U.S. gets a cold, emerging markets gets the flu.”

We previously removed our holdings in this sector and remain flat currently. We will continue to monitor performance for opportunity if it presents itself.

Dividends and Equal weight continue to hold their 200-dma. We continue to hold our allocations to these “core holdings", but are closely monitoring performance. The continued development of a downtrend channel is concerning.

Gold continues its volatile back-and-forth trade but remains confined below a massive level of multi-top resistance. Last week, I noted that Gold not only failed another test of recent highs but broke back below its 50-dma. Gold is now flirting with its 200-dma as actually inflationary pressures remain elusive at best. We currently do not have exposure to gold, and have been out for a long time, but if you are already long the metal hold for now. $123 on GLD is a hard stop.

Bonds and REITs – last week interest rates peaked over 3% for just a brief moment before plummeting back to earth. With a continued string of weak economic reports look for rates to continue to slide lower. The sharp whipsaw in bond prices proved profitable after adding to bond exposure last week. The 50-dma is flattening out which suggests the current sell-off may be near its end.REIT’s, on the other hand, continue to build an uptrend after finding support at the 50-dma. While the sector is very overbought, a correction that maintains the bullish trend will be buyable and we will be looking to add exposure.

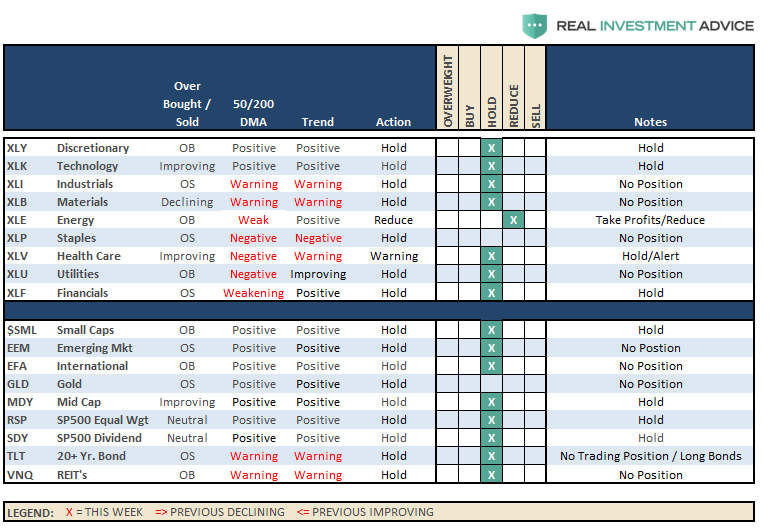

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

There is no change from last week’s update.

Over the last several weeks we have continued to maintain higher levels of cash than normal as market volatility has markedly increased. This past week, we tested the 200-dma once again and held support but continue to remain confined to a downtrend overall. This keeps us cautious at the moment and we continue to use rallies to sell “out of model” positions so portfolios can be positioned to enter into our models as the opportunity presents itself.

While we continue to honor the current “bullish trend", we remain very aware of the rising risks and continue to look for opportunities to derisk and re-hedge portfolios while “sell signals” remain firmly intact.

In our equity/option wrap model, we continue to just let options mature/expire and allow that process to derisk portfolios automatically. That model will be rebuilt as premiums in options in our selected equity screens rebalance to more profitable levels.

As noted last week, the rally has been extremely weak and lacked real conviction. However, if the market can break above the current downtrend channel on heavy volume, confirming a breakout, we will reallocate and rebuild portfolio models accordingly.

For the moment, we are just letting the markets determine the best course of action and we continue to raise cash on technical breakdowns. Our bigger concern, remains the relative risk to capital if the 9-year old bull market is ending. If the current correction expands into a more meaningful reversionary process, we will become much more aggressively risk adverse. There is plenty of evidence to support the latter case.

It is crucially important the market maintains the current uptrend from the recent lows. After having reduced exposure a couple of weeks ago, we remain on alert for the next opportunities.

We remain keenly aware of the intermediate “sell signal“ which has now been “confirmed” by the recent market breakdown. We will continue to take actions to hedge risks and protect capital until those signals are reversed.

THE REAL 401k PLAN MANAGER

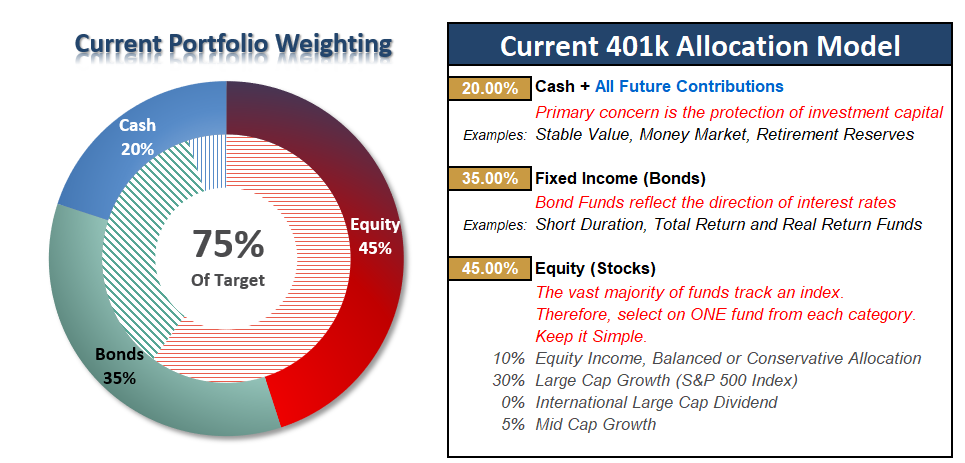

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Another Retest

Once again the markets testing and held support at the 200-dma. That is the good news.

The not so good news is the overall trend of the market continues to weaken which is pulling our short-term moving average down towards the long-term. A crossover of those two averages have historically not been a good indication or forward short-term returns.

As I wrote three weeks ago, the “reflexive rally” to reduce exposure finally got into the “neighborhood” of our initial target area that we laid out more than a month ago. We suggested raising cash at that point. However, for new readers, we continue to suggest the same course of action on any rally next week.

“With both confirmed “sell signals” in place, and becoming more negative, the risk to equity exposure currently remains to the downside. If conditions improve we will rebalance equity risk in portfolios back to full allocations but a LOT has to happen first.”

If you have already reduced equity exposure just sit tight this week and let’s see what happens.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more