Markets Go On Alert

Let me start with what I wrote on Friday:

“In my money management process, portfolio ‘risk’ is ‘ratcheted’ up and down based on a series of signals which tend to indicate when market dynamics are either more, or less, favorable for having capital exposed to the market.”

As you will notice, portfolios NEVER reach 100% cash levels. The reason is purely for psychological reasons.

Let me explain.

Back in 2008, we had gone to almost all cash in portfolios between April and June. I thought it would be a relatively simple process of reallocating portfolios once the right opportunity came along. I learned that was not to be the case due to the psychological trauma caused by a major bear market.

This realization came in February 2009 when I wrote the article “8-Reasons For A Bull Market” which stated:

“Any weakness next week will most likely warrant a push down to 800 for first support and then the November lows of 750. We believe that these lows will hold although we are aware that if the market doesn’t get ‘it’ together soon further weakness could show itself.

We are cautious here and still holding on to a lot of cash waiting for some signal that the market is making a turn for the short term to the better. March, April, and May tend to be fairly strong months for the market and any ‘real’ assistance next week for homeowners could push the markets higher. A move above 900 will be a signal for a move higher in the markets.“

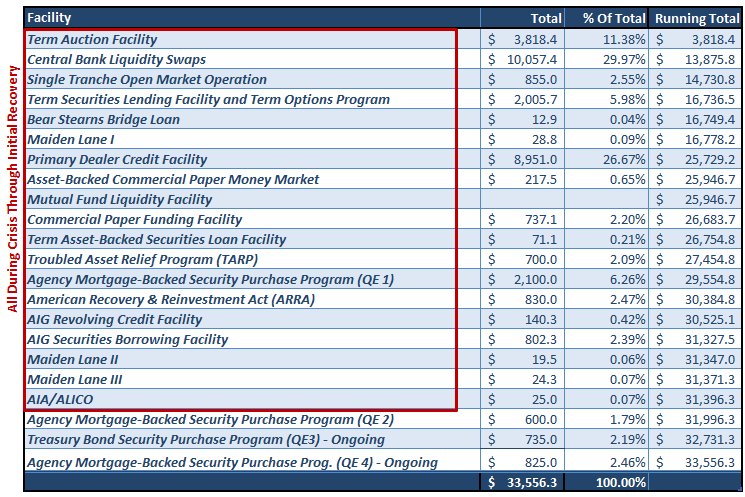

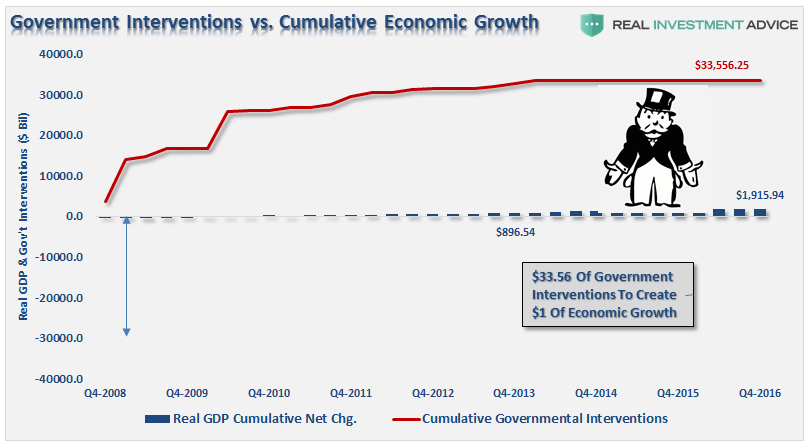

Of course, the market bottomed on March 9th at 666 and never looked back as an estimated $33 Trillion in various bailouts, workouts, subsidies, and QE followed as shown in the table below. (This does not include the ongoing reinvestment from the Fed’s balance sheet)

Of course, the problem is that despite the massive interventions since the financial crisis, there has been very little relative return on those investments.

But I digress.

When the markets bounced above 900, suggesting it was time to re-enter the market, I faced extremely tough resistance from clients. In fact, I lost clients because they were afraid the markets would only continue lower.

While this moment was the epitome of Baron Rothschild’s statement, “The time to buy is when there’s blood in the streets,” the psychological damage was so deep, that investors could not make the switch from “absolute safety” to some “risk.”

Of course, this psychological problem is the reason why investors consistently “buy high” and “sell low.” It is also why I learned it is far easier add to an existing allocation, which can be completely hedged,as improvement is already understood.

So, why do I bring this up?

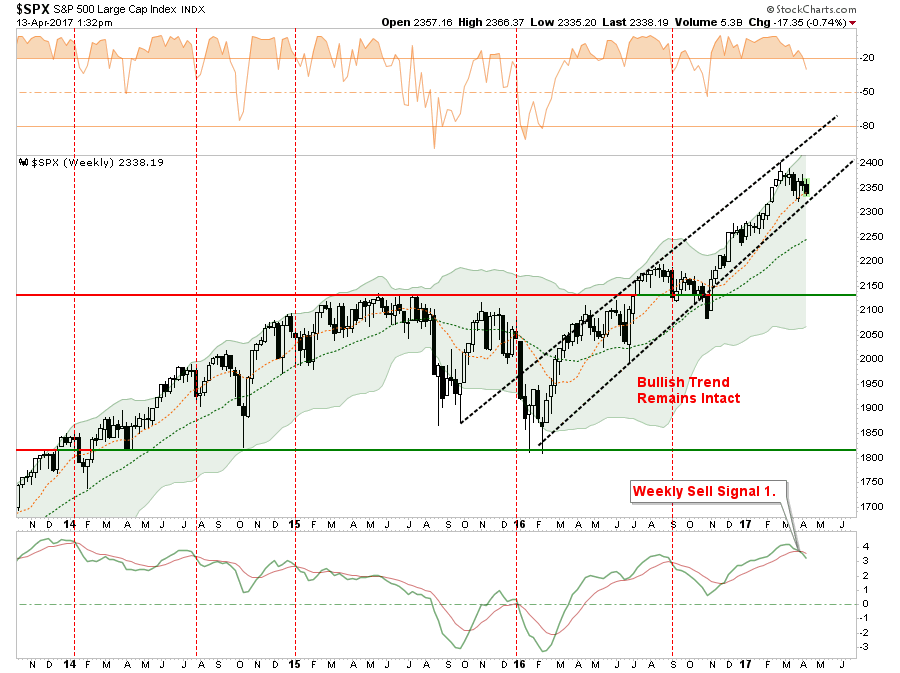

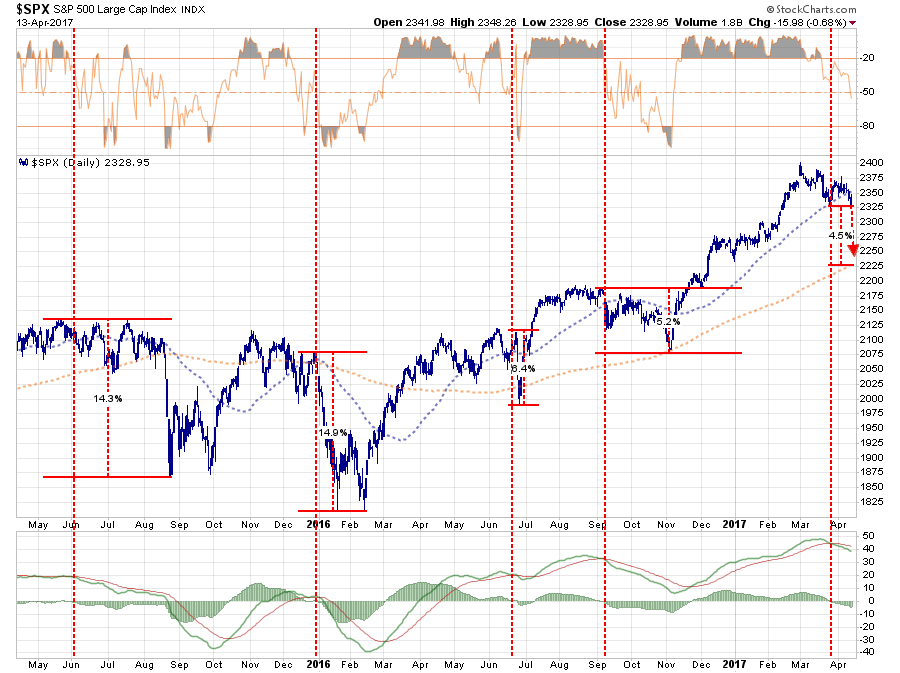

Because the market has now tripped the first signal as shown above, and below, sending a warning that further weakness could ensue. With the first signal registered, combined with a break of the 50-dma, we are now on “a signal-1 alert.”

With portfolios already hedged, as we added a lot of bond and interest rate sensitive holdings back in January, there is no action to take currently. This is why, for now, it is only an “alert” that something more important is developing.

The bullish trend remains intact, and the two primary signals (2 & 3), which would initiate further equity reductions, remain on “buy signals” currently.

But this signal should be of no surprise to readers as we have been watching the development over the last few weeks. As I noted last week in “Questioning The Bullish Trend:”

“As stated, portfolios remain bullishly allocated for now but with a cautious underpinning.We are still maintaining hedges until the current corrective action completes.

Furthermore, we are currently maintaining “new money” in short-term cash positions and only selectively stepping into core long-term holdings with tight stop-loss levels.”

Such remains the case this coming week.

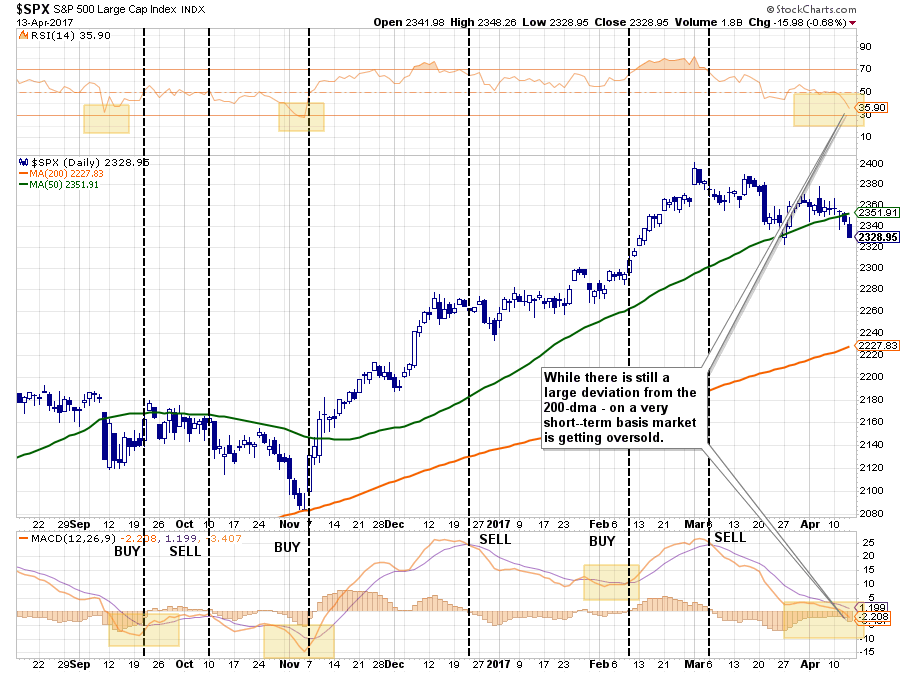

IMPORTANT: By the time weekly signals are issued on an intermediate-term basis, the market is generally oversold, with “bearish” sentiment increasing, on a short-term (daily) basis. Given those short-term conditions, it is quite likely the markets will rally next week.

IMPORTANT: It is the success or failure of that rally attempt that will dictate what happens next.

- If the market can reverse course next week, and move back above the 50-dma AND break the declining price trend from the March highs, then an attempt at all time highs is quite likely. (Probability Guess = 30%)

- However, a rally back to the 50-dma that fails will likely result in a continuation of the correction to the 200-dma as seen previously. From current levels that would suggest a roughly -5%drawdown. However, as shown below, those drawdowns under similar conditions could approach -15%. (Probability Guess = 70%)

PORTFOLIO ACTION GUIDELINES

Given this is only a “warning signal” currently, any RALLY in the next week should be used to take some action within portfolios. The following list provides some basic guidelines.

- Trimming back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

These actions will temporarily reduce portfolio risk and raise cash levels which either provides a “hedge” against a subsequent downturn OR cash to buy better performing assets if conditions improve.

It’s a win/win in either case.

Bond Bull Is Back

I have been unabashedly bullish bonds since 2013, when calls from Gundlach, Gross, and others are declared the early death of the bond bull.

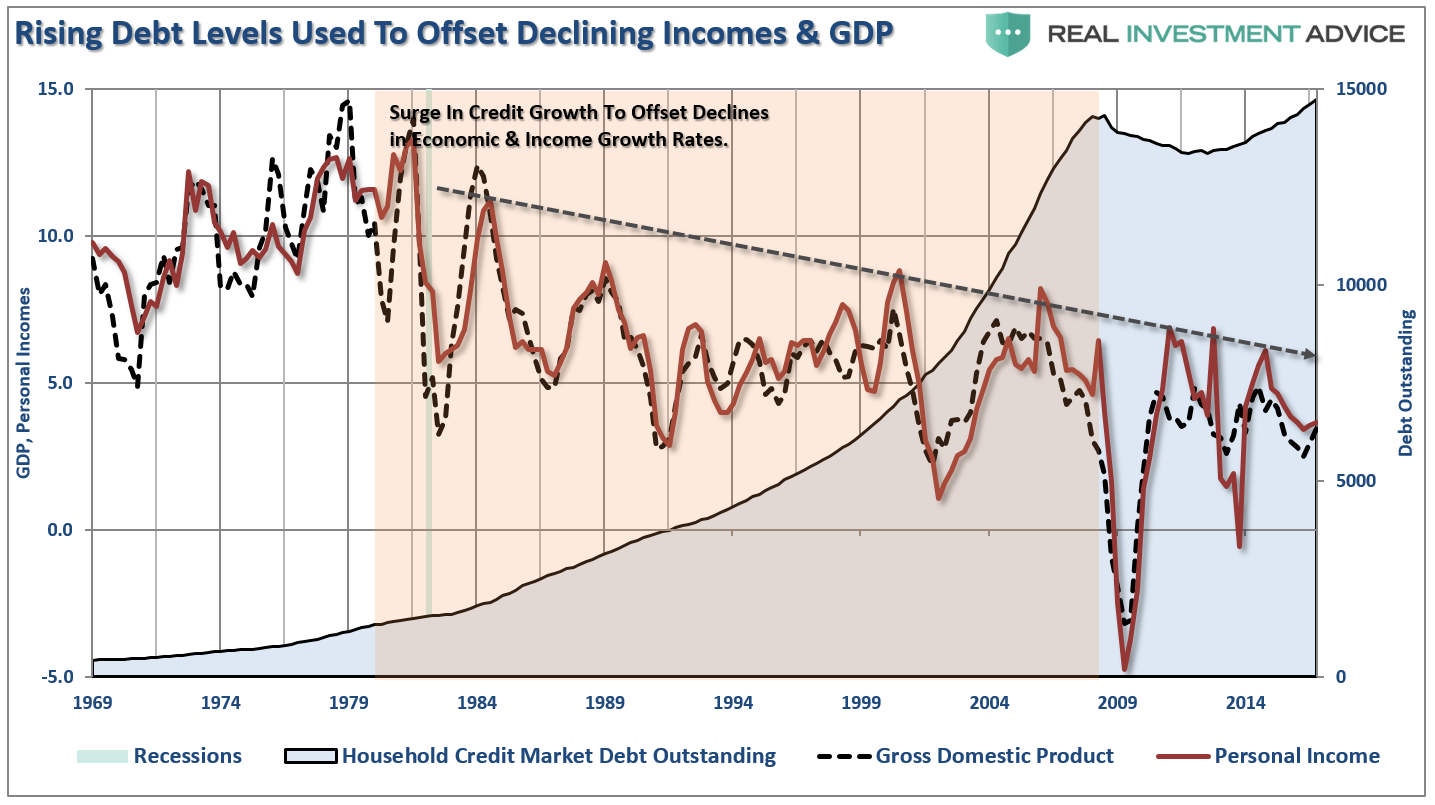

The reason is simple, and something I have discussed many times in the past, interest rates are NOT going to rise much given the long-term downtrend in economic growth, inflation and wages and rising debt. As I addressed in “The Long View:”

“Today, the U.S. is no longer the manufacturing epicenter of the world. Labor and capital flows to the lowest cost providers so that inflation is effectively exported from the U.S. and deflation can be imported. Technology and productivity gains ultimately suppress labor and wage growth rates over time. The chart below shows this dynamic change which began in 1980. A surge in consumer debt was the offset between lower rates of economic growth and incomes in order to maintain the ‘American lifestyle.’”

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds.

However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates, however, are an entirely different matter.

“While there is not much downside left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Since interest rates affect ‘payments,’ increases in rates quickly have negative impacts on consumption, housing, and investment.”

It is not surprising that even given the small bump in rates since the election that mortgage-related transactions, auto and retail sales, and economic growth have all slipped. The consumer is directly tied to the level and direction of rates from both a fiscal and psychological perspective.

- People buy payments – not houses, cars or phones. Therefore, rising rates put payments out of reach of many Americans.

- Psychologically, when rates rise, people hold off purchasing items “hoping” rates will come back down again.

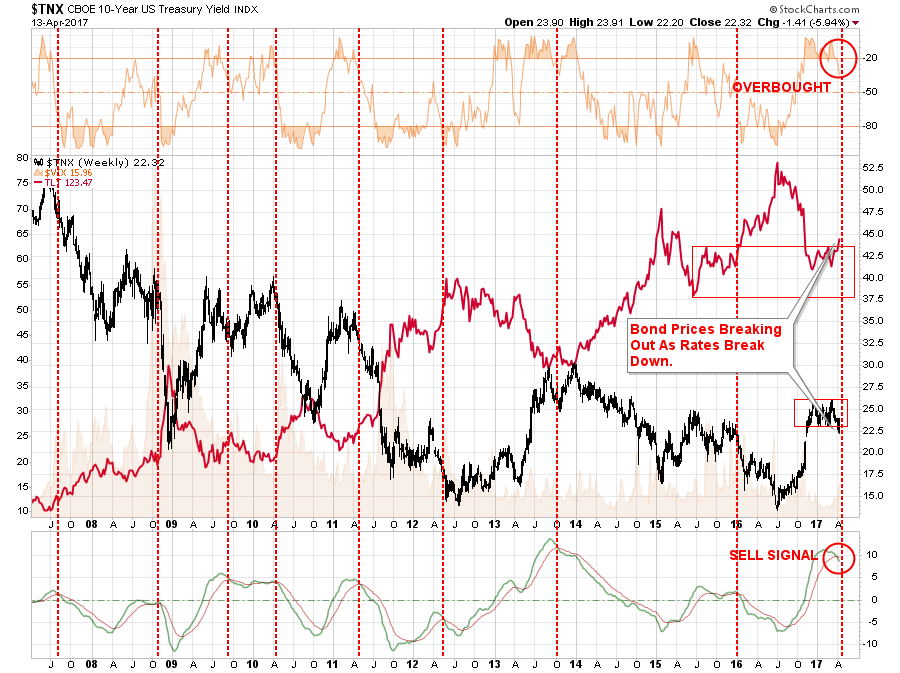

Therefore, when rates recently went to 2.6% and the bond bears once again growled their assertion rates could only go higher – I was aggressively buying bonds into portfolios. Since then, rates have fallen and have, on a weekly basis, pushed bonds back onto a “buy signal” as shown below.

The “red dashed” lines denote all the “sell signals” going back to 2007. The last time interest rates tripped a signal from a similarly high level was in 2013 where rates fell from 3.0% to 1.6%.

Given the still large short position in bonds, although it has been reduced substantially from its recent record levels, suggests that a run down in rates towards 2% or less is highly likely.

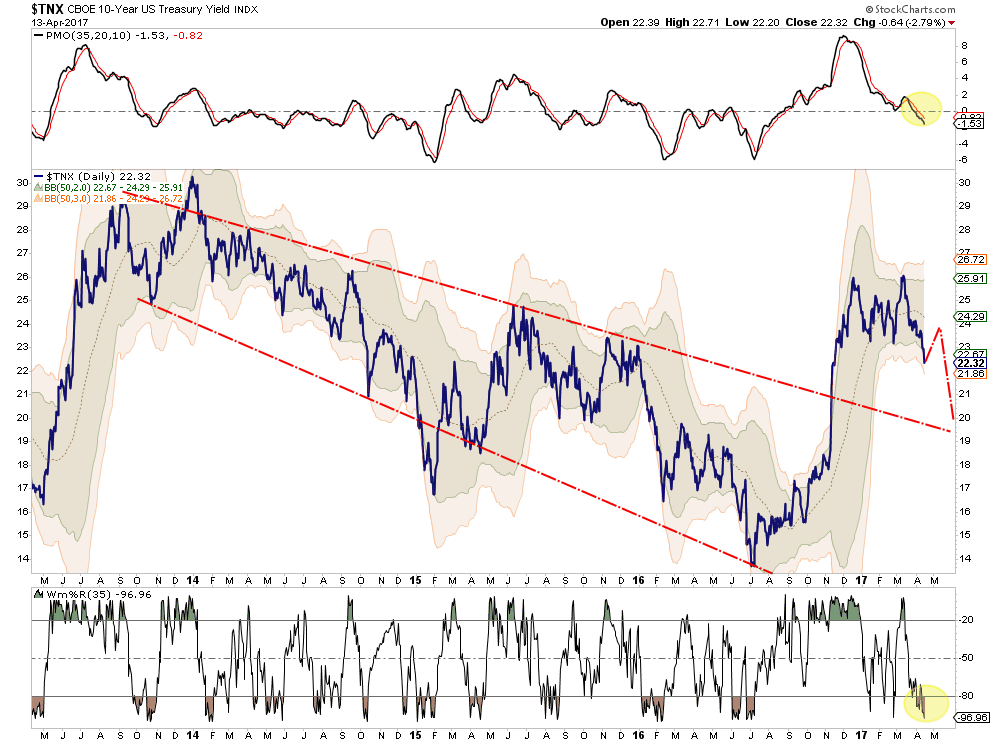

However, in the very short-term, the move in rates, and subsequent rise in bonds, has gotten a bit stretched. Therefore, IF we get a short-term reflexive rally in stocks next week, I would expect some selling pressure in bonds to emerge.

The recent gains from the “rotation” trade, as I discussed at the beginning of this year, has been largely capitalized on. Therefore, some profit taking and rebalancing portfolio weightings in bonds makes sense.

Will the “bond bull” market eventually come to an end? Yes, eventually. However, the catalysts needed to create the type of economic growth required to drive interest rates substantially higher, as we saw previous to 1980, are simply not available today. This will likely be the case for many years to come as the Fed, and the administration, come to the inevitable conclusion that we are now caught in a “liquidity trap” along with the bulk of developed countries.

I am long bonds, and will continue to buy more whenever someone claims:

“The Great Bond Bull Market Is Dead.”

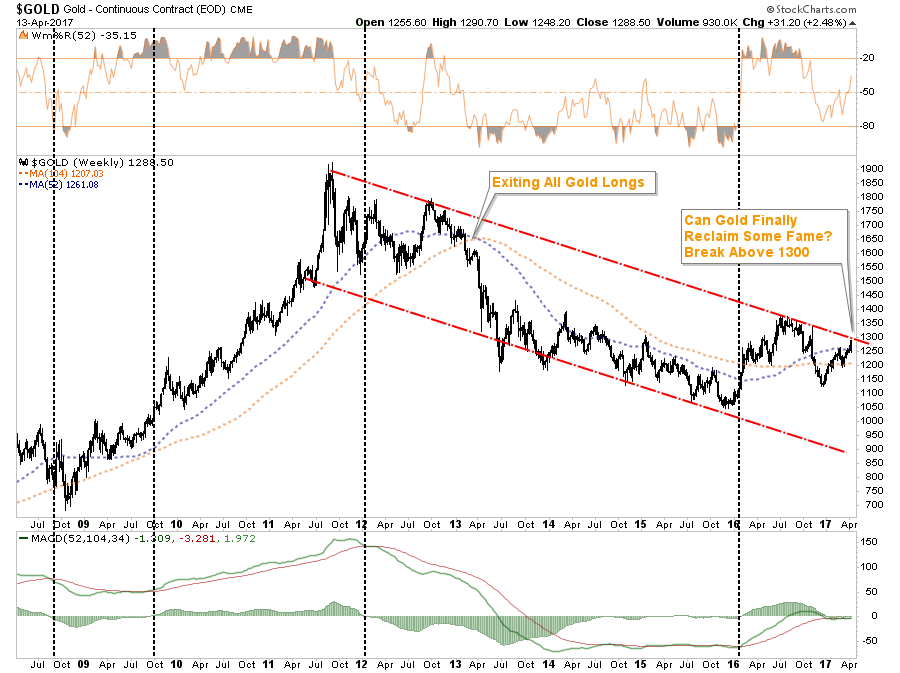

Gold Reclaims Some Fame

“War, huh, yeah

What is it good for

Absolutely nothing” – Edwin Starr

Well, actually, “war,” or the perceived threat of it, tends to be good for gold. This is particularly the case over the last couple of weeks as Syrian missile strikes have raised the ire of Russia while the Trump administration is sending not so subtle threats to North Korea.

From a weekly perspective, Gold is becoming more interesting. Back in 2013, I exited all of our long gold positions at the time due to the breakdown in the metal as QE-3 flooded the system with liquidity making the “safe haven” of gold unattractive at the time.

With the Fed now raising rates and discussing the reduction of their balance sheet, combined with rising economic policy uncertainty, the “mix of ingredients” to draw investors back into the shiny metal have improved.

As shown in the chart above, Gold is still contained in a well-defined downtrend. However, a break above $1300 an ounce will provide a reasonable setup to add gold back into portfolios from a trading perspective.

We will be watching for that opportunity as the bullish backdrop improves.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

If you have any suggestions or additions you would like to see, send me an email.

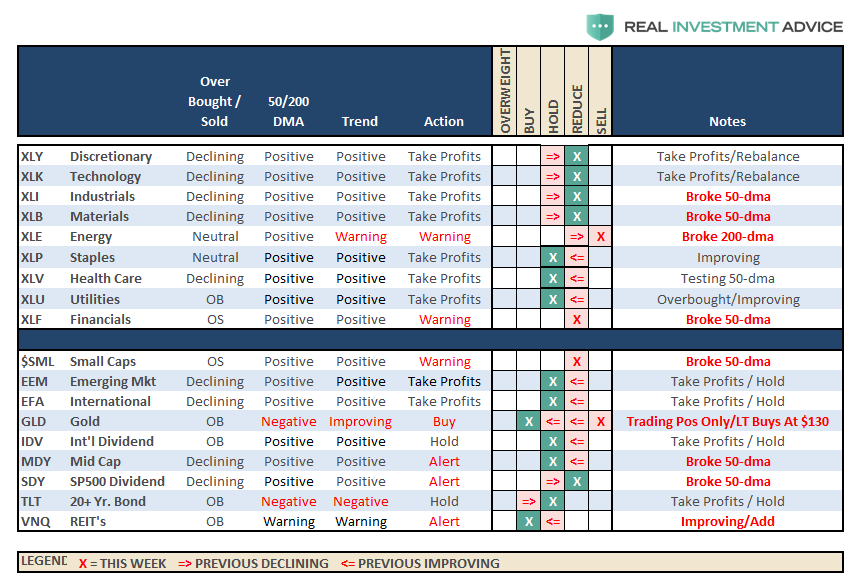

Sector Analysis

The slow-motion correction that began back in March continued this past week and picked up steam as the break below the 50-dma occurred triggering a weekly sell-signal as discussed above.

The conditions currently present suggest a rally attempt over the next few days and any such attempt that fails to reclaim the 50-dma should be used to reduce portfolio risk.

Remain cautious currently as the “risk off” trade has continued to advance over the last week, again.

Technology, Healthcare, and Discretionary sectors continue to struggle with their respective 50-day moving averages. While still trending positively, relative performance has weakened substantially for now.

Energy continues to struggle after breaking its 50-dma and broke its 200-dma two weeks. While energy had a bit of a bounce last week, and tested resistance at the 50-dma, the bounce failed and the trend continues to materially weaken. Energy is very close to a major sector sell signal. Remain heavily underweight energy for the time being.

Materials, Financials, and Industrials have broken their 50-dma, as the “Trump Reflation Trade” has come to an end. With CPI contracting on Friday, the whole trade remains at risk. Underweight these sectors for now.

Bonds, Utilities, and Staples all continue to be the clear winners, which we were discussing back in January, as the Trump Trade was going to reverse. Those hedges have continued to perform well despite the weakness in other areas of the market.

Small and Mid-Cap stocks continued to weaken in terms of relative performance and have broken their respective 50-dma’s. The deterioration of relative strength continues to suggest caution.

Emerging Markets, International, and Dividend Yielding Stocks are also showing weakness but remain in a bullish trend currently. Some profit taking and rebalancing is advised.

Bonds and REIT’s got oversold three weeks ago and performance has continued to improve this past week. If the broad markets run into further trouble look for a continued rotation in the “safety trade.” However, bonds are now very overbought so taking some profits and waiting for a correction to add further exposure makes sense.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

After hedging our long-equity positions 17-weeks ago with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities, Health Care and Staples) we did rebalance some of our long-term CORE equity holdings back to original portfolio weightings harvesting a bit of liquidity.

While the bullish trend is still positive, which keeps us allocated on the long-side of the market, the weekly “sell signal” alert is not being dismissed.

Any rally next week that “fails” to but the market back onto more solid footing will be used to reduce risk in portfolios to some degree and rebalance back to target weightings.

As noted last week:

“We are still maintaining hedges until the current corrective action completes. Furthermore, we are currently maintaining ‘new money’ in short-term cash positions and only selectively stepping into core long-term holdings with tight stop-loss levels.”

We continue to maintain very tight trailing stops as the mid to longer-term dynamics of the market continue to remain very unfavorable.

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

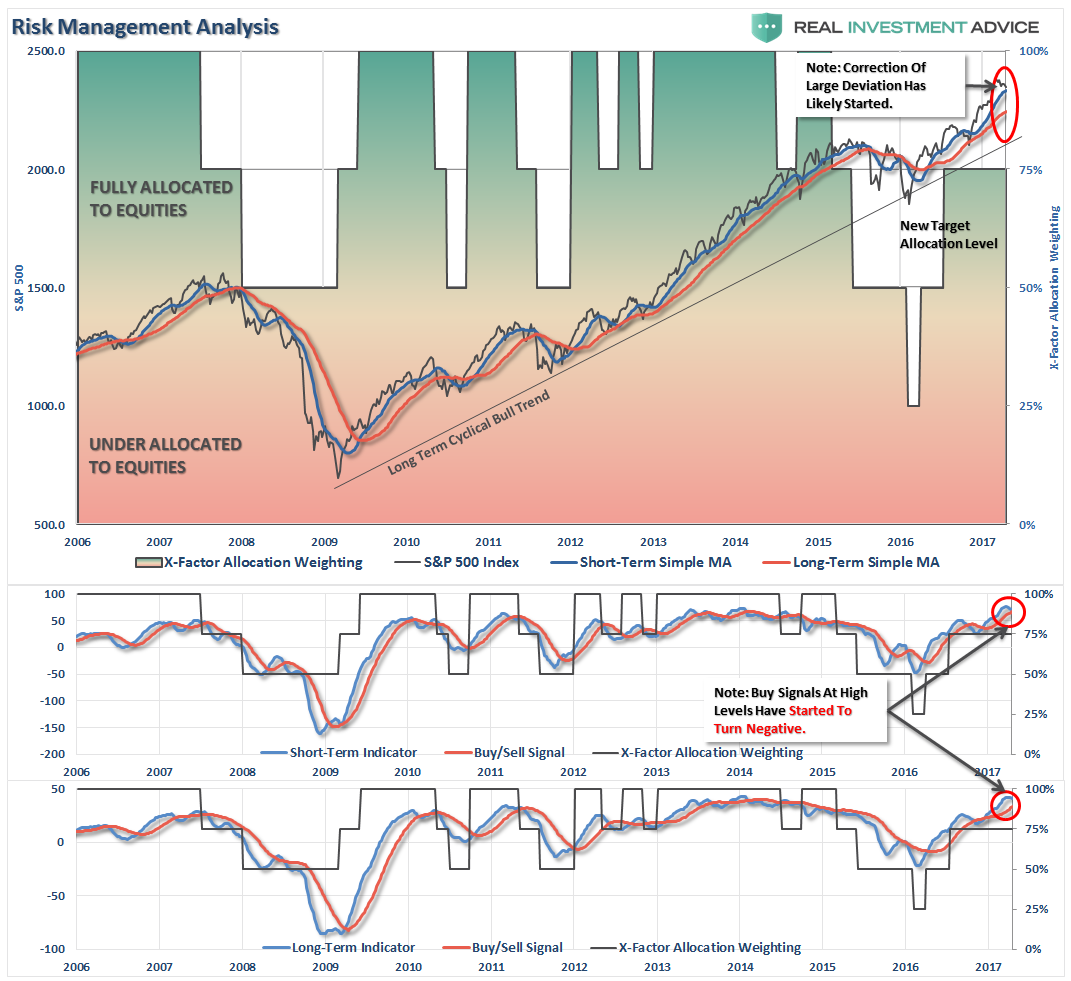

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Sell Signal Alert 1

The consolidation in the market over the last few weeks – failed.

As I had noted over the last month, I was looking for an opportunity to move allocations back to the 100% allocation target but the risk/reward dynamic for such a move had not been favorable.

This past week, as detailed in the main missive above, the market broke through support at the 50-dma and spun off an initial “alert” sell signal. As such, all allocation adjustments remain on hold until the market correction is completed or reversed.

As noted in the 401k-chart above, the current extension above the moving average has started to correct. The buy signals are beginning to contract and the deviation above the long-term average is being reduced.

Importantly, the “warning” signal is just that…a warning. As long as the correction process is confined to a bullish trend, a reversal of the corrective action will allow for an increase in the model exposure. But that time is not now.

Maintain cash, rebalance portfolio allocations and reduce risk. If the economic data continues its string of weakness, geopolitical tensions continue to mount or some other exogenous issue impacts the market in the short-term, you will be thankful for the extra cushion.

I did note a few weeks ago, the run-up in interest rates HAD put bonds into a favorable position to add exposure in portfolios. That suggestion played out very favorably but with rates now back to short-term overbought condition, refrain from adding further fixed income holdings for now but maintain exposures.

If you need help after reading the alert; don’t hesitate to contact me.

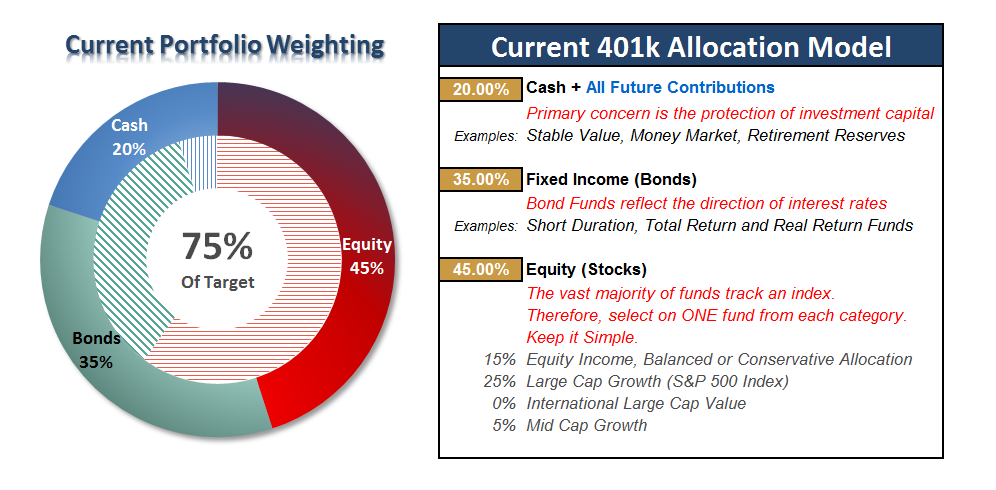

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principal. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more