One difficulty in analyzing our economic future is the sheer number of potential crises. When so much could go wrong (and really right, when the exponential technologies I foresee get here), it’s hard to isolate, let alone navigate, the real dangers. We are tempted to ignore them all. Ignoring them is usually the right response, too. We can “Muddle Through” almost anything.

But muddling through isn’t the same as smooth sailing. It’s difficult, unpleasant, and often keeps you from looking for better opportunities. Then there are times when you can’t even muddle through. Instead, you find yourself emotionally at a dead stop or even going backwards. When surviving the storm is your focus, taking those “blood in the streets” buying opportunities is hard.

Which leads to this week’s letter. Almost every day I read scores of finance and economic newsletters, websites, articles, and books. A few articles on pensions hit my inbox this week and pursuing them led me to today’s topic.

But dear gods, I can remember writing a decade ago that public pension funds were $2 trillion underfunded and getting worse. More than one person told me that couldn’t be right. They were correct: It was actually much worse. (See, I’m an optimist!)

Two years ago I wrote that Disappearing Pensions are The Crisis We Can’t Muddle Through. Nothing since then has changed my mind. In fact, failure at all levels to even begin solving the problem is making it worse. The latest estimates, as we will see, suggest that it has gotten $2 trillion or more worse in just a few years.

Note we are talking here about a specific kind of pension: defined benefit plans, usually those sponsored by state and local governments, labor unions, and a dwindling number of private businesses. Many sponsors haven’t set aside the assets needed to pay the benefits they’ve promised to current and future retirees. They can delay the inevitable for a long time but not forever. And “forever” is just around the corner.

As we will see below, the numbers are large enough to make this a problem for everyone, even those without affected pensions. The problem is “solvable”… but the solutions will be problems in themselves.

Underfunded Future

![]()

AddThis Sharing Buttons

Share to Facebook

259Share to TwitterShare to LinkedIn

Your Pension May Be Monetized

By John Mauldin

May 10, 2019

Options

Underfunded Future

Pension Fund Underfunding Is a Local Problem

Make the Children Pay

The Strategic Investment Conference and Possible Recessions

One difficulty in analyzing our economic future is the sheer number of potential crises. When so much could go wrong (and really right, when the exponential technologies I foresee get here), it’s hard to isolate, let alone navigate, the real dangers. We are tempted to ignore them all. Ignoring them is usually the right response, too. We can “Muddle Through” almost anything.

But muddling through isn’t the same as smooth sailing. It’s difficult, unpleasant, and often keeps you from looking for better opportunities. Then there are times when you can’t even muddle through. Instead, you find yourself emotionally at a dead stop or even going backwards. When surviving the storm is your focus, taking those “blood in the streets” buying opportunities is hard.

Which leads to this week’s letter. Almost every day I read scores of finance and economic newsletters, websites, articles, and books. A few articles on pensions hit my inbox this week and pursuing them led me to today’s topic.

But dear gods, I can remember writing a decade ago that public pension funds were $2 trillion underfunded and getting worse. More than one person told me that couldn’t be right. They were correct: It was actually much worse. (See, I’m an optimist!)

Two years ago I wrote that Disappearing Pensions are The Crisis We Can’t Muddle Through. Nothing since then has changed my mind. In fact, failure at all levels to even begin solving the problem is making it worse. The latest estimates, as we will see, suggest that it has gotten $2 trillion or more worse in just a few years.

Note we are talking here about a specific kind of pension: defined benefit plans, usually those sponsored by state and local governments, labor unions, and a dwindling number of private businesses. Many sponsors haven’t set aside the assets needed to pay the benefits they’ve promised to current and future retirees. They can delay the inevitable for a long time but not forever. And “forever” is just around the corner.

As we will see below, the numbers are large enough to make this a problem for everyone, even those without affected pensions. The problem is “solvable”… but the solutions will be problems in themselves.

Underfunded Future

Like what you’re reading? Subscribe now and receive the full version of John Mauldin's Thoughts from the Frontline delivered to your inbox each week.

Already have an account? Click here to log-in.

We never share your email with third parties.

Let’s begin with the enormity of the pension funding gap. As with the federal budget deficit, the large numbers are hard for our minds to process. They are also inherently uncertain. Let me explain.

A defined benefit pension plan for, say, a city’s police department, knows it owes a certain number of retirees certain monthly benefits for life. Their lifespans are fairly predictable when the pool is large enough. (I think new biotechnologies will change this soon, but that’s another topic.)

From that, it’s simple math to calculate how much money the plan should have right now in order to pay those benefits when they are due. But then the assumptions start. The plan must presume a future rate of return on the invested portfolio, an inflation rate, and in some cases future health care costs (medical benefits are part of many plans).

So, when we say a plan is “fully funded,” it may not be so if the assumptions are wrong. The amount a plan is underfunded could be much larger than the sponsor and auditors say. In theory, it could be smaller, too, but I have never seen that happen. The accounting rules that govern all this allow (some would say encourage) the sponsoring cities, counties, and states to understate their liabilities. This lets them avoid hard decisions like raising taxes, cutting benefits, or reducing other needed services.

Here’s a Wharton School note to place this huge number in context.

Sanitation workers, firefighters, teachers and other state and local government employees have performed their duties in the public sector for decades with the understanding that their often lackluster salaries were propped up by excellent benefits, including an ironclad pension. But Moody’s Investors Service recently estimated that public pensions are underfunded by $4.4 trillion. That amount, which is equivalent to the economy of Germany, accounts for one-fifth of national debt. It’s a significant concern for public employees who were banking on a fully funded retirement to get them through their golden years. The true number could be much higher. Whatever it is, filling it will be painful for somebody. Pensioners will receive lower-than-expected benefits, taxpayers will get higher-than-expected tax bills, or citizens will see government services cut. Or maybe all the above.

Then again, if you make more realistic assumptions on future returns the unfunded liability becomes $6 trillion according to the American Legislative Exchange Council. Total state and local annual revenues are only $3.1 trillion. Total property taxes are roughly $590 billion.

Here’s more grim news from The Heritage Foundation.

Overall, the American Legislative Exchange Council estimates that pension plans have only about a third of the funds on hand—33.7 percent—that they need to pay promised benefits. Some states have significantly lower funding levels, which means they are at risk of running out of funds in the near future.

Once a state or local pension plan runs out of money, taxpayers have to fund the pension benefits of retirees as well as the contributions of current employees.

Connecticut, Kentucky, and Illinois have the lowest funding ratios, at 20 percent, 21 percent, and 23 percent respectively.

Already, Illinois spends as much on pensions as it does on welfare and public protection (that is, police and firefighters) combined, and nearly half of its education appropriations go toward teacher pensions. If the state’s pension plans reach insolvency, pensions could become its single biggest cost.

These unfunded liability estimates are high because plan assumptions are too optimistic. Almost all public pension funds assume investment returns somewhere around 7% (and some as high as 8%+). A more conservative and realistic approach would force the state and local governments to fund those pension plans at a much higher level by either raising taxes or reducing services. What local politician will volunteer to do that? Better to find a consultant to tell you what you want to hear. There are plenty of them that will, for a reasonable fee, billed to the taxpayers.

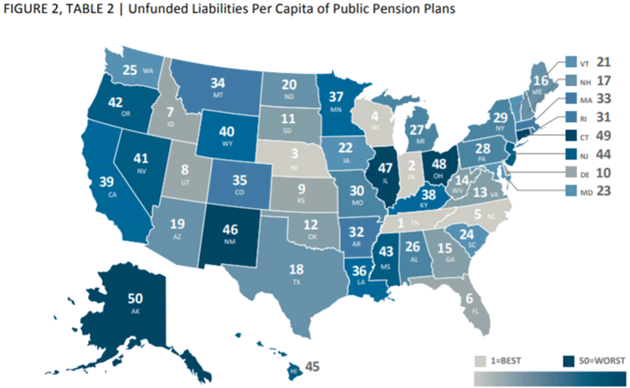

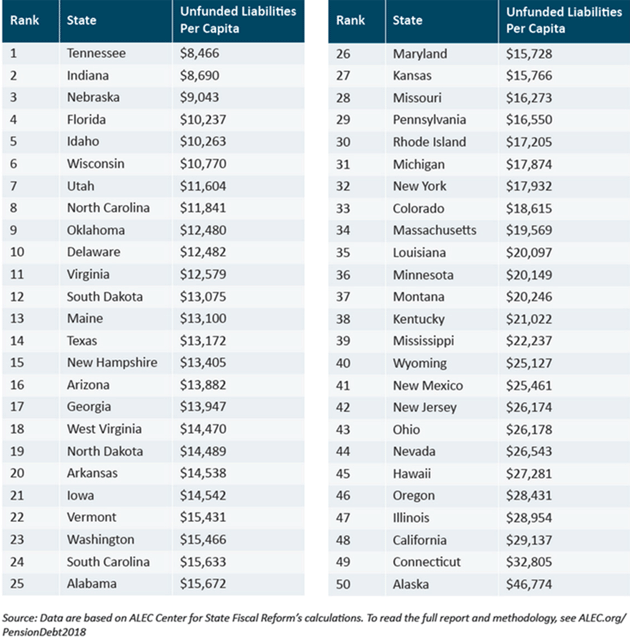

The following graphic shows how your state is ranked on a per capita funding basis. You can see the absolute numbers in the following table.

Source:

A further complication is that the taxpayers who might have to cover these amounts are mobile. They can move to other states with lower tax burdens, leaving behind those who, for whatever reason, can’t leave their states.

And to make it even more interesting, the beneficiaries often no longer live in the states that pay them. Retired public employees from the Northeast might live in Florida now, for instance. They can’t even vote for the people who govern their incomes.

The broader point: As with the federal debt, some portion of this unfunded pension debt is going to get liquidated in some manner. Any way we do it will hurt either the pensioners or taxpayers.

Pension Fund Underfunding Is a Local Problem

Thirty years ago Frisco, Texas, had fewer than 20,000 residents. Today its population is well over 180,000. Corporations from all over America are moving there. Tax revenues are booming. Frisco is the happy exception that simply grew faster than its pension liabilities.

Not so Dallas, whose Police and Fire Pension System was advertised as solvent just a few years ago. Now it is so deep in the hole that the mayor says plugging the gap would take almost a doubling of city taxes. (I bought my Dallas apartment after that news was announced but such an increase would have still made my taxes cost more than my mortgage. Can you say taxpayer revolt? It wasn’t the main reason, but it did factor in to my move.) Texas Monthly recently noted:

For those of us in Texas, with our gloriously high credit ratings and fervent allegiance to low taxes, restrained spending and conservative oversight of a robust Rainy Day Fund, the news that certain big cities around the country were in a heap of trouble might have elicited nothing more than a collective, if somewhat condescending, shrug. Except for one thing: Texas’s four biggest cities were all high on the list [of the worst 15 cities]. Dallas, which came in second, is on the hook for $7.6 billion, about five times the amount of its total operating revenues. Houston was fourth, with a $10 billion shortfall—equal to four times its operating revenues. Austin, at number nine, has $2.7 billion in liabilities, and San Antonio, ranked number twelve, is $2.3 billion short. That seems like very bad news for just about any Texan. Particularly since the vast majority of Texans now live in urban areas. How can a state known for fiscal responsibility have so many cities with empty pockets?

Will Frisco residents want to pay for the Dallas pension funding problems? Is The Woodlands going to want to pay for Houston’s problems? Is Indiana ready to pay for Illinois? Of course not. How much of a crisis will we need in order to recognize we are all in this together? Probably a lot bigger than you imagine.

Make the Children Pay

While arguments progress at the national level, state and local leaders must simultaneously pay their pension benefits, provide public services, and keep taxes to a level that doesn’t sweep them out of office or drive top taxpayers away. Not to mention keep the markets happy enough to sell future bond offerings, until such time as the Fed steps in as buyer-of-last resort. A tall order.

Given those choices, the usual answer seems to be “cut services and hope no one notices.” It is happening nationwide but California is in the vanguard, thanks to its massive pension debt. This is from a recent Brookings Institution note.

Pension and health-benefit costs are bending education finances in California to their will. The sheer magnitude of the rising costs is staggering. Large numbers of school board officials who participated in our survey indicate that the rising costs are meaningfully affecting educational services. For example, many report making cost-saving changes to district budgets that include deferred maintenance, larger class sizes, and fewer enrichment opportunities for students in response to rising pension and health benefit costs.

So in effect, today’s students are paying to keep benefits flowing to retired teachers and administrators.

Meanwhile, the Berkeley city council is taking criticism for prioritizing pension payments ahead of public works projects. Voters approved bond issues supposedly dedicated to infrastructure but the city is apparently not doing the work.

Nor is it just California. In a recent study, Bank of America analysts found an inverse relationship between infrastructure investment and pension fund contributions. Each additional $1 billion in plan contributions subtracts about $2.5 billion from state and local government investment.

We have multiple parties fighting over pieces of the same pie, all hoping that Uncle Sam will step in and save them. Uncle Sam may well do it, too, but it won’t remove the pain. It will just redistribute the burden, perhaps more widely, but the aggregate amount won’t change.

In my view, this leads to some kind of Japan-like deflationary recession. If we’re lucky, it will be mild and long. It won’t be fun but the alternatives would be worse.

The Strategic Investment Conference and Possible Recessions

Newt Gingrich asked me last week about the timing of the next recession. I knew he was thinking about the election in 2020, but the data I trust the most (Steve Blumenthal tracks it here) only goes out about nine months. While global recession is a possibility in the next nine months, the US seems to be okay. But Scott Minerd at Guggenheim has raised his odds of a recession in 2020.

Timing will certainly be a topic of discussion at next week’s Strategic Investment Conference, along with many other topics. There will be several panels dealing with the ever-increasing US and global government debt. Longtime readers know I am not happy with where we are or how we got here, but the path we choose from here will make a big difference. I think we will see Japanification and massive quantitative easing throughout the developed world. As I’ve written the past few weeks, that will bring financial repression and reduced growth. Of course, there are those who want to go ahead and take the pain. It would be severe but not of Biblical proportions. But I just don’t see politicians and voters choosing such pain.

The newly fashionable Modern Monetary Theory (MMT) isn’t the answer, though even Ray Dalio is now toying with it. (I’ll be responding to him in a future letter.) Down that path is Weimar-like inflation and then hyperinflation. I don’t think that is likely, but I find it alarming that more and more people are giving MMT proponents political and philosophical cover.

Speaking of choices, Donald Trump has a very difficult and risky one. He is the first president since Nixon opened China to seriously push back on their theft of intellectual property, the openness of their markets, and their mercantilism. I am not a fan of tariffs, but something does need to be done. If the higher tariff he just launched don’t disappear quickly, we will see a much higher recession probability. I see high probability they will try to shortstop it but wargaming the multiple scenarios is simply impossible. This is high-stakes poker with the global economy as the pot. Well, that and the future of both countries. High stakes indeed. It helps that the new tariffs won’t go on goods currently in transit. That amounts to a few weeks “time out” during which they might reach agreement before anything actually gets taxed.

If you want to better understand what we are dealing with in China, let me suggest three books. The first two are Michael Pillsbury’s The Hundred Year Marathon and George Magnus’s Red Flags: Why Xi’s China Is in Jeopardy. Different perspectives. At the conference we will focus a lot on China with both bullish and bearish speakers.

Then for a fun read, which I finished a few days ago on the plane, get David Ignatius’s blockbuster spy thriller/science fiction novel, The Quantum Spy. It will give you insights into China’s theft of intellectual property, cyber warfare and who is controlling it, as well as introduce you to the potential of quantum computers. This book is well researched, has great characters and plot, and deserves the accolades it gets. I can go on but seeing how few science fiction books I’ve recommended over the years, compared to how many I’ve read, pay attention to this one.

And with that I will hit the send button. If you won’t be at the SIC, you really should get your Virtual Pass which is the next best thing. You can watch it live, watch or listen to it later, or read the transcripts.

Have a great week! I will admit SIC week is the highlight of my year. I am really pumped about this one. So many friends, so much learning, and a lot of fun, too. How much better can it get?

Your trying to keep up with a few dozen balls in the air analyst,

Comments

Log in or sign up to join the conversation.