Here is the opening statement from the Department of Labor:

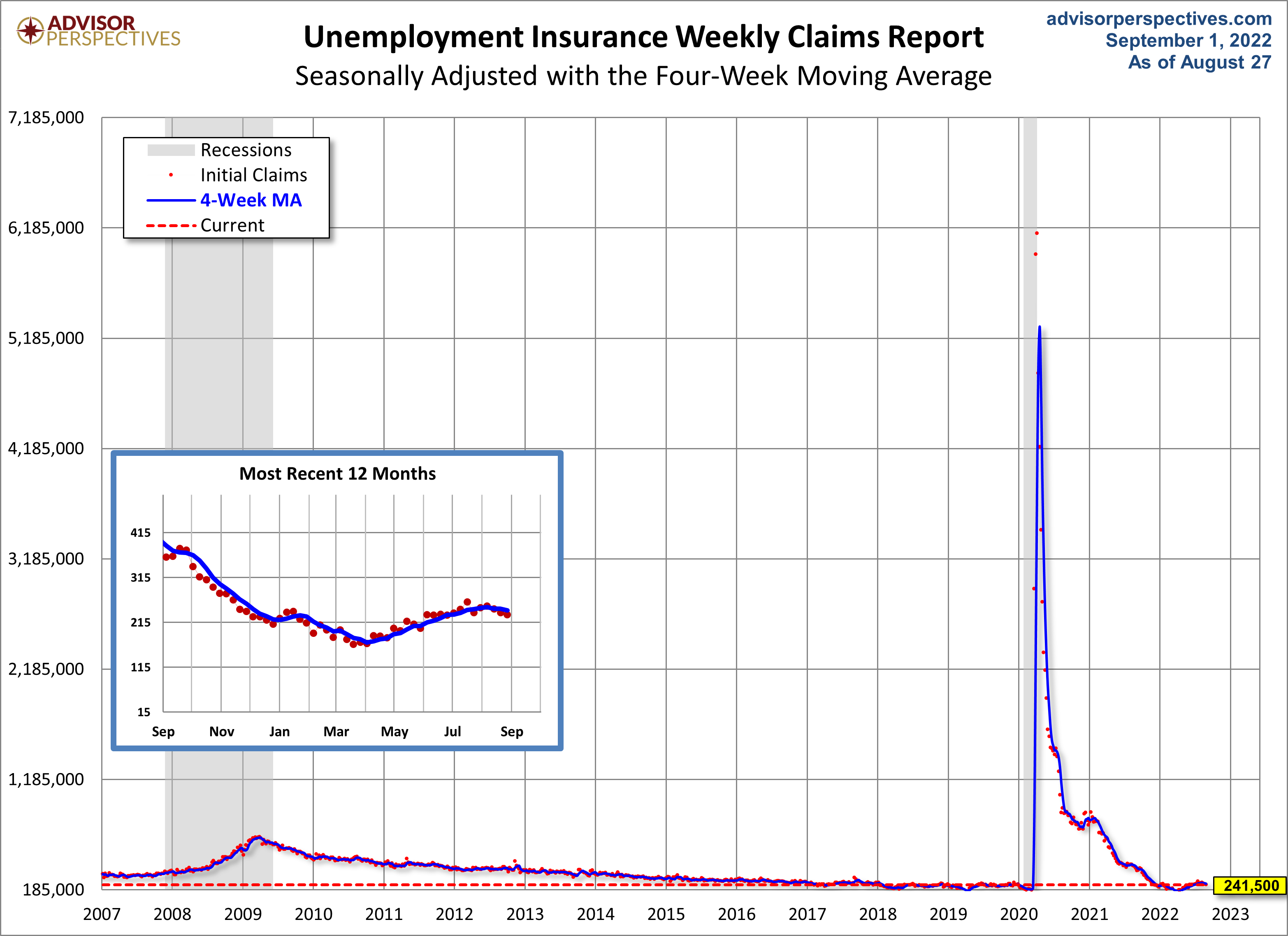

In the week ending August 27, the advance figure for seasonally adjusted initial claims was 232,000, a decrease of 5,000 from the previous week's revised level. The previous week's level was revised down by 6,000 from 243,000 to 237,000. The 4-week moving average was 241,500, a decrease of 4,000 from the previous week's revised average. The previous week's average was revised down by 1,500 from 247,000 to 245,500.

The advance seasonally adjusted insured unemployment rate was 1.0 percent for the week ending August 20, unchanged from the previous week's unrevised rate. The advance number for seasonally adjusted insured unemployment during the week ending August 20 was 1,438,000, an increase of 26,000 from the previous week's revised level. The previous week's level was revised down by 3,000 from 1,415,000 to 1,412,000. The 4-week moving average was 1,428,500, an increase of 4,500 from the previous week's revised average. The previous week's average was revised down by 750 from 1,424,750 to 1,424,000.

This morning's seasonally adjusted 232K new claims, down 5k from the previous week's revised figure, was better than the Investing.com forecast of 2458K.

Here is a close look at the data over the decade (with a callout for the past year), which gives a clearer sense of the overall trend.

As we can see, there's a good bit of volatility in this indicator, which is why the 4-week moving average (the highlighted number) is a more useful number than the weekly data. Here is the complete data series.

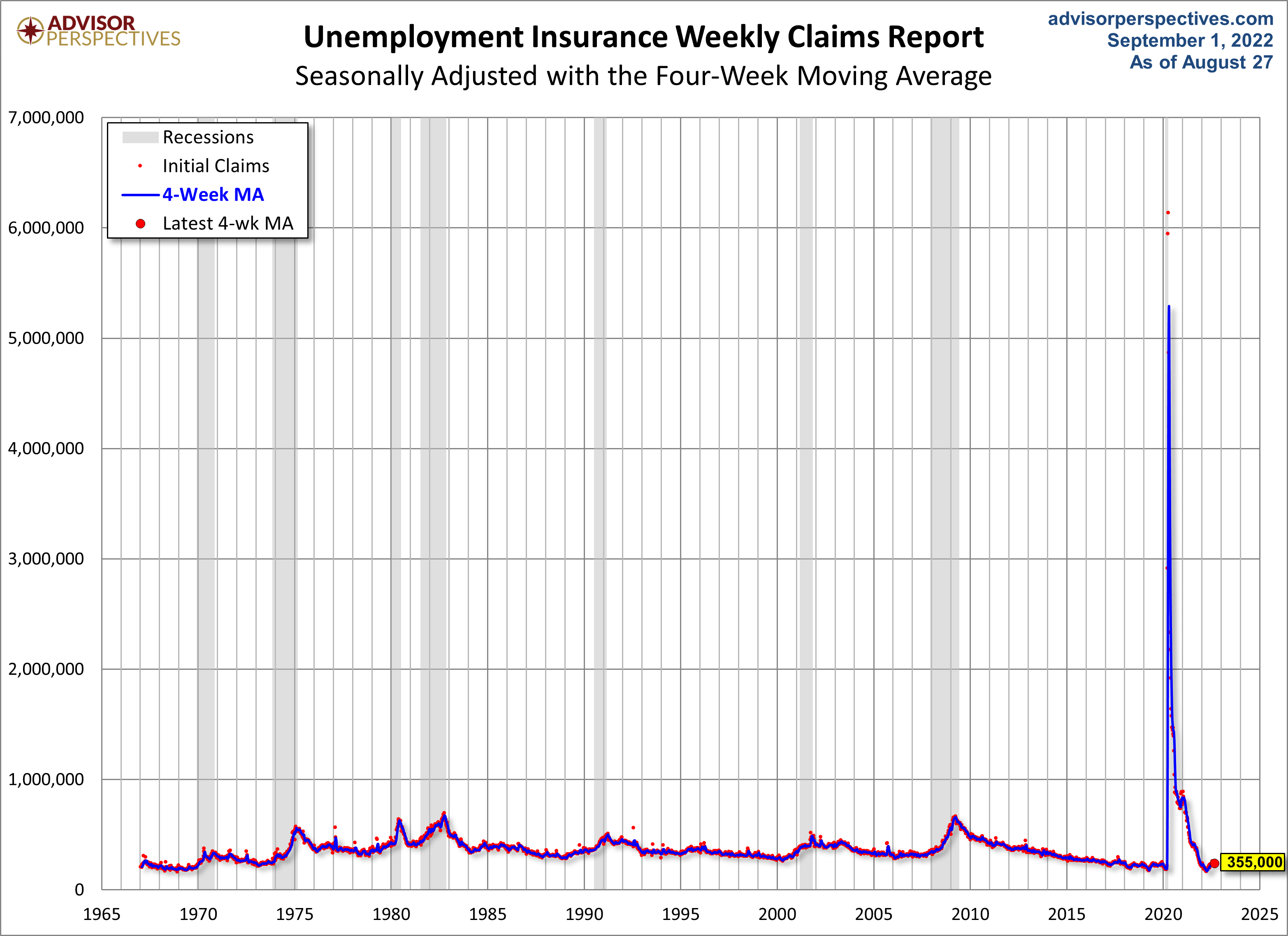

Here's a copy of the above chart, but zoomed in, so the COVID spike isn't as prominent.

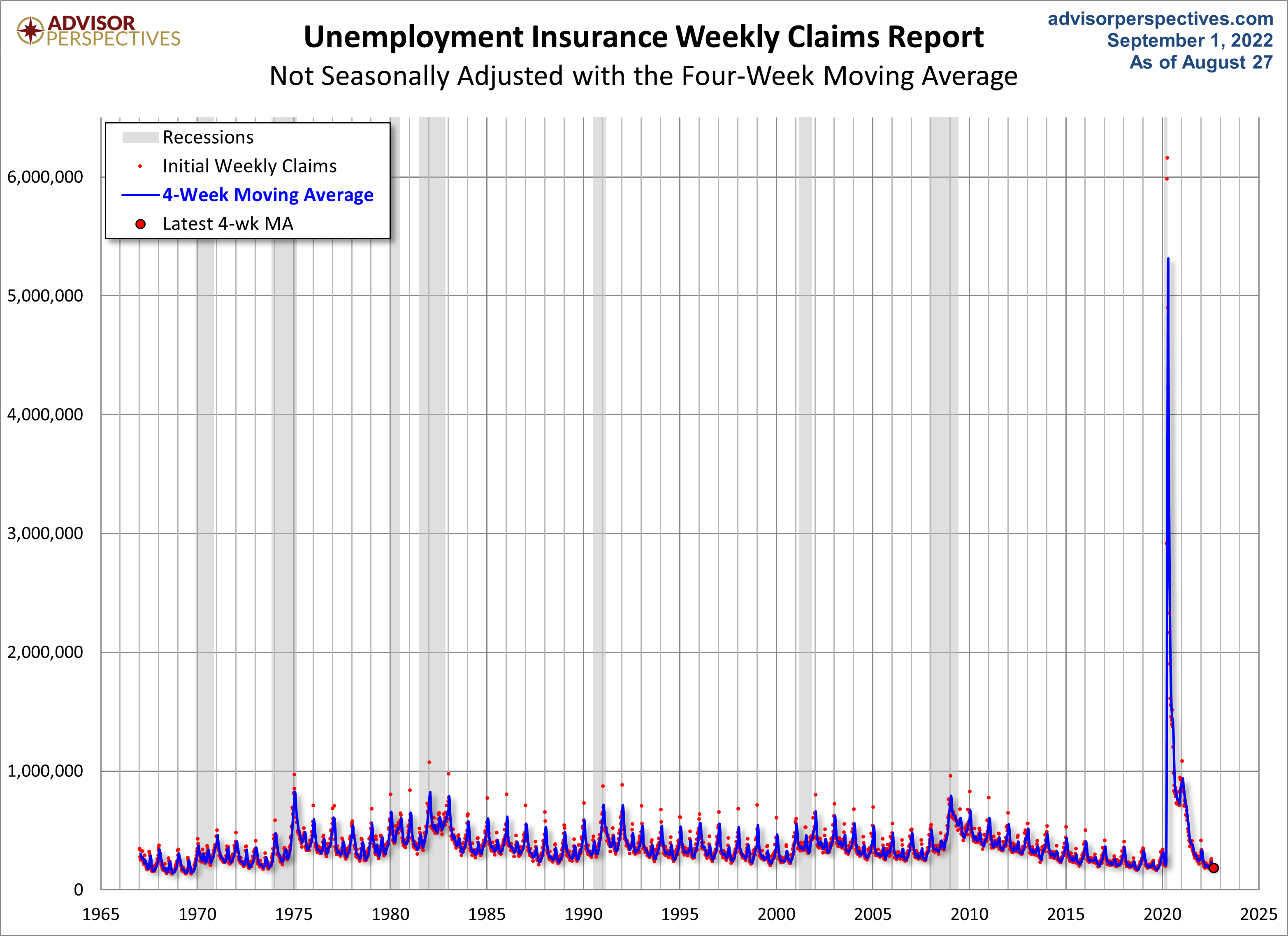

The headline Unemployment Insurance data is seasonally adjusted. What does the non-seasonally adjusted data look like? See the chart below, which clearly shows the extreme volatility of the non-adjusted data (the red dots). The 4-week MA gives an indication of the recurring pattern of seasonal change (note, for example, those regular January spikes).

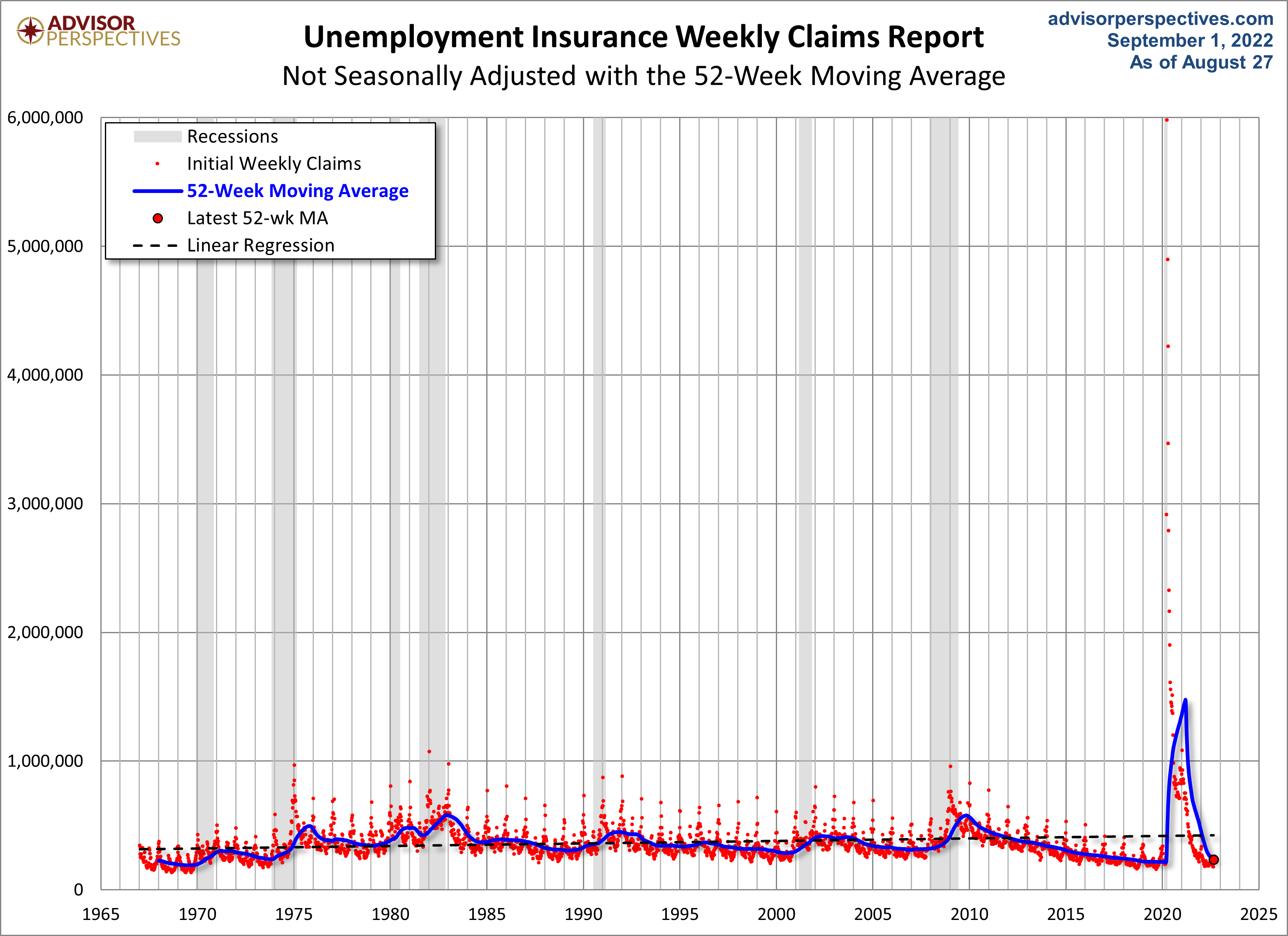

Because of the extreme volatility of the non-adjusted weekly data, we can add a 52-week moving average to give a better sense of the secular trends. The chart below also has a linear regression through the data.

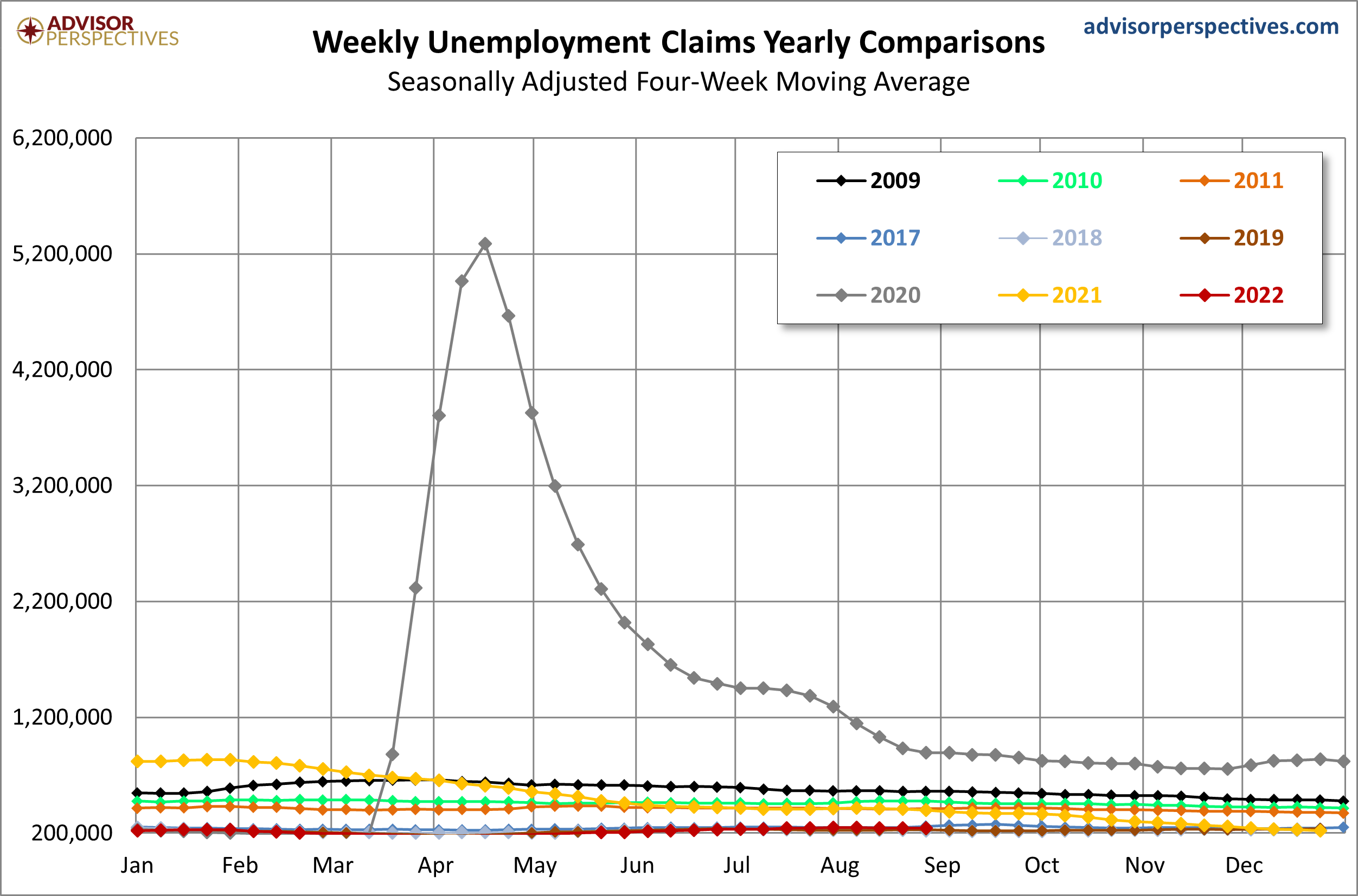

Here's a look at a sample of year's claims going back to 2009.

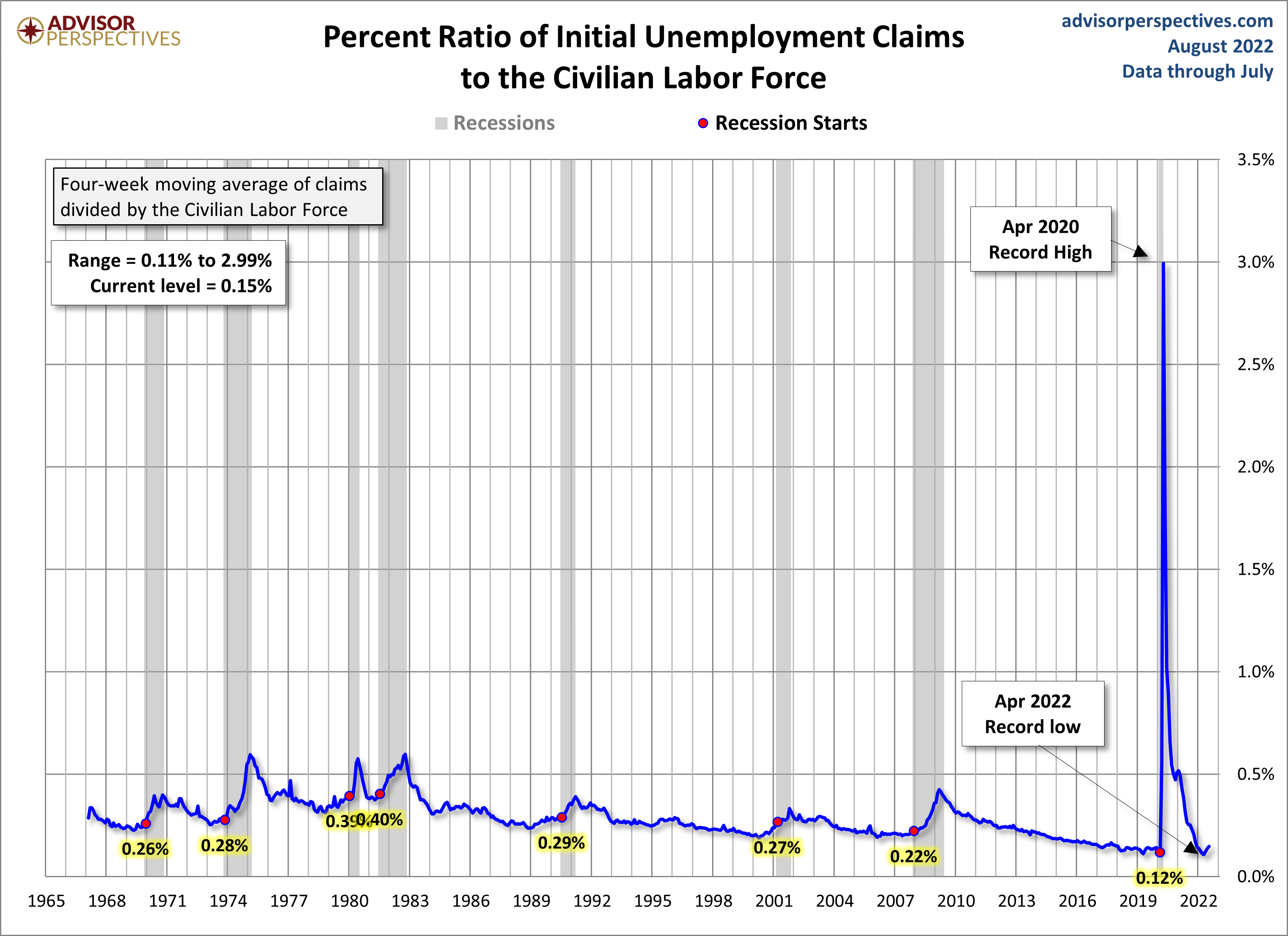

For an analysis of unemployment claims as a percent of the labor force, see this regularly updated piece The Civilian Labor Force, Unemployment Claims and the Business Cycle. Here is a snapshot from that analysis.

More By This Author:

June S&P/Case-Shiller Home Price Index: Up 18% YoY

Chicago PMI Mostly Unchanged In August

Moving Averages Month-End Preview: Down 3.5% In August

Comments

Log in or sign up to join the conversation.