Friday, June 11, 2021 1:35 PM EDT

The University of Michigan sentiment index offers a Goldilocks scenario for markets in that confidence continues to move higher yet inflation expectations have edged lower. Nonetheless, households are doubting the Fed’s signal on policy with two-thirds expecting higher interest rates in the next year.

The June preliminary reading for the University of Michigan consumer sentiment index shows confidence moved higher, led by the key expectations index reaching a new pandemic period high. 54% of respondents believe incomes will rise over the next 12 months while optimism on employment prospects are also higher.

This is encouraging for the growth outlook given the historically strong correlation between the overall expectations indicator and consumer spending. This index should continue moving higher as the reopening gathers momentum, jobs return and incomes continue to rise, as companies desperately try and recruit to take advantage of the strong consumer demand story.

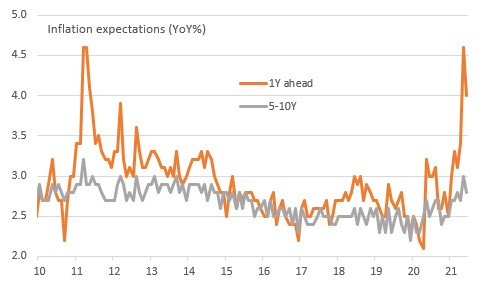

Inflation expectations edge lower after the recent spike

Source: Macrobond, ING

Bond markets have also taken confidence from the data on inflation expectations, which moved lower after a sharp spike last month. Nonetheless, the 1Y ahead expectations remain well above levels seen over the past decade and the 10Y expectations also remain elevated relative to recent history.

The text of the report suggests that “rising inflation remained a top concern of consumers”. Prices for cars and homes were a particular worry with the “good time to buy a home” and “good time to buy a vehicle” indices both dropping to their lowest reading since 1982. Households seem to be doubting the messaging from the Federal Reserve that interest rates are not going to be raised anytime soon - the report suggests more than two-thirds of households expect to see higher borrowing costs over the next 12 months.

Another interesting aspect is the political split. The report suggests the Republicans continue to feel the current situation is just as bad as it was in the depths of the global financial crisis while Democrats think things are as good as they have ever been. The political polarisation shows no sign of healing and if anything appears to be getting more entrenched across a range of issues.

Consumer sentiment by support for political party

Source: Macrobond, ING

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.