Image Source: Unsplash

The jobs market is tight, inflation is above target, consumer spending is holding up and recent Fed commentary suggests they are in no hurry to loosen policy. As such we continue to favor May as the starting point for interest rate cuts rather than March as the market currently favors.

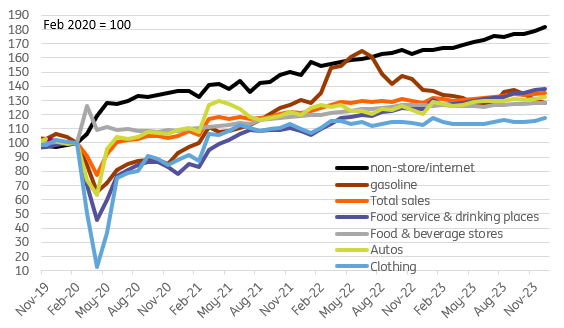

Retail sales hold up well in December

US retail sales rose 0.6% month-on-month in December, above the 0.4% consensus. Motor vehicles jumped 1.1% MoM with clothing up 1.5% and department stores reporting a 3% MoM gain. There was some offsetting weakness in furniture, electronics, gasoline, and health/personal care. Meanwhile, the control group, which excludes volatile components such as gasoline, building materials, and autos and better correlates with broader consumer spending trends rose 0.8% MoM versus the 0.2% MoM consensus. This highlights that the US economy ended the year in decent shape with next week’s fourth quarter 2023 GDP report, we believe, likely reporting growth in the 2-2.5% range. With the jobs market remaining tight and inflation still above target we continue to take the view that May is the more likely starting point for Fed easing versus the market’s pricing of March.

US retail sales levels (Jan 2020 = 100)

Image Source: Macrobond, ING

But challenges for the consumer remain intense

That said, we remain cautious about the prospects for consumer spending over the medium term. There are four ways to finance spending; from income, from savings (either save less each month or run down savings), borrow (such as on a credit card), or sell assets. Real household disposable income will hopefully be lifted by wage growth increasingly outpacing inflation as the latter continues to slow, but slowing jobs growth limits the upside. Pandemic-era savings appear to be in the process of being exhausted for an increasing number of households and are unlikely to be as supportive this year as they were in 2023. Meanwhile, consumer borrowing costs continue to rise with credit card, personal loan, and car loan borrowing rates all at 20+year highs. We therefore suspect that consumer spending will increasingly struggle over the next couple of quarters and the Fed will indeed respond with interest rate cuts, just not as early as the market expects.

Industrial activity stays sluggish

US industrial production was also a bit firmer than expected for December. It rose 0.1% versus the 0.1% drop expected, but this is mitigated by a downward revision to November's growth rate of 0.2 percentage points (to 0%). Manufacturing rose 0.1% MoM after a 0.2% increase in November. That said, the only reason we have growth is due to the continuing rebound in auto output following the strike action seen in October that prompted a 10% drop in vehicle production. Manufacturing ex autos has fallen for three consecutive months and the ISM manufacturing survey suggests little prospect of a turnaround anytime soon seeing as it has now been in contraction for 14 consecutive months. Rounding out the report, warmer weather mean utilities output fell 1% MoM but the warm weather also allowed drilling and mining activity to continue unimpeded, leading to a 0.9% MoM increase there.

More By This Author:

FX Daily: Enthusiasm Has Been CurbedUK Inflation Unexpectedly Picks Up Amid Stubborn Services Price Rises

The Commodities Feed: USD Surge Holds Complex Back

Comments

Log in or sign up to join the conversation.