Will The January MLP Effect Beat Negative Sentiment?

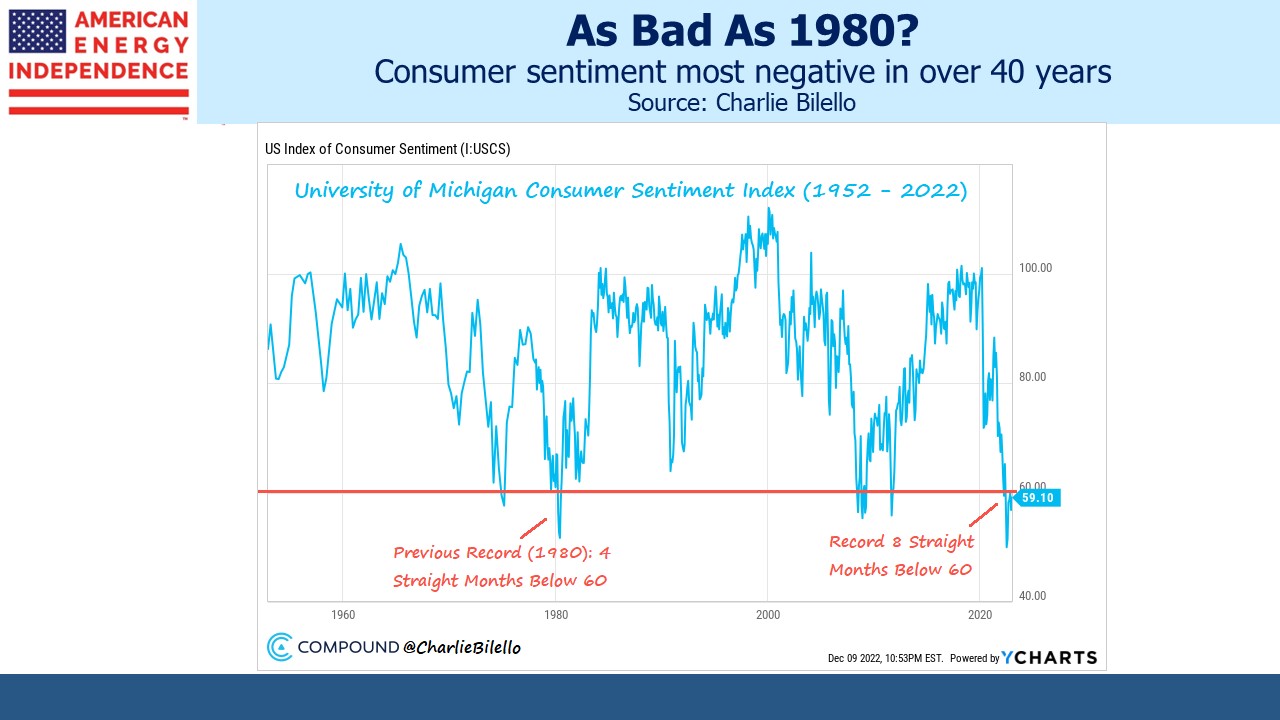

Consumer sentiment is as bad as 1980 when inflation was 13%. The Fed funds rate swung from 17% to 9% before peaking at 19% in early 1981. Eight US marines died in Iran in a failed attempt to rescue our hostages. John Lennon was shot. No wonder Ronald Reagan won election later that year. Consumers today are more negative than they were back then.

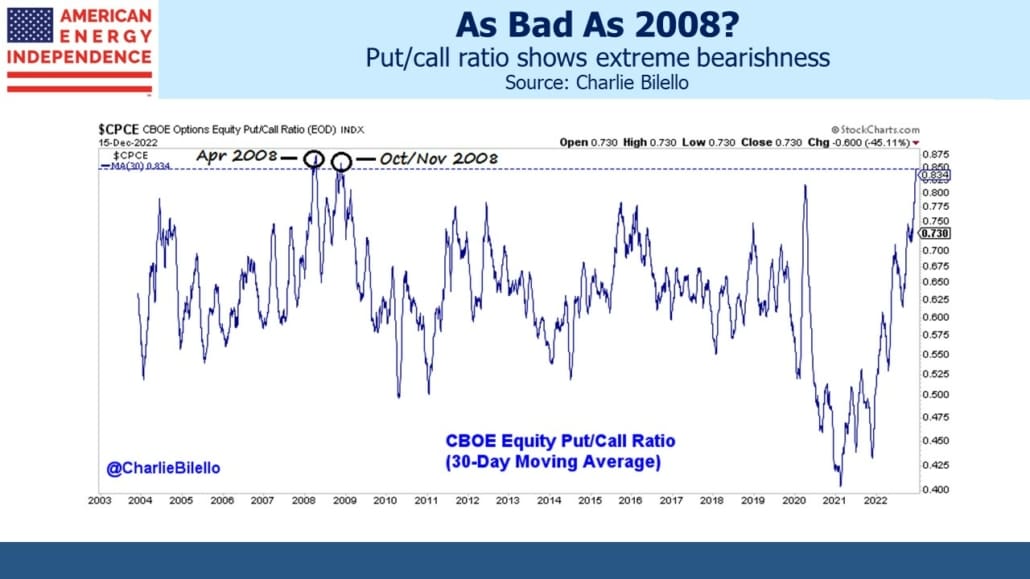

The put/call ratio is close to the extremes of the Great Financial Crisis in 2008 when Bear Stearns was bailed out by JPMorgan and Lehman failed. There’s plenty of negatives, but are prospects really that terrible?

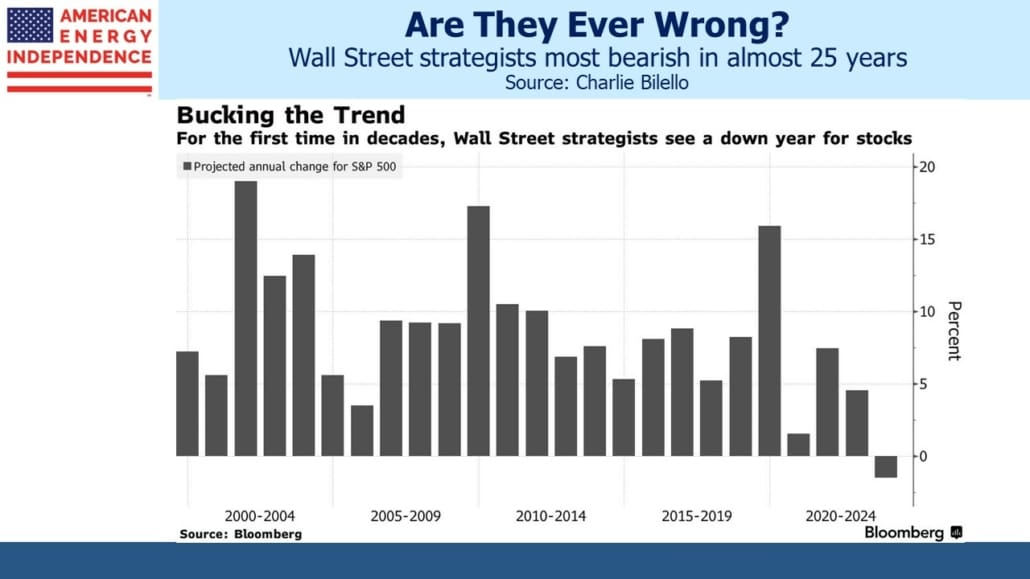

If you’re not yet convinced of pervasive bearishness, how about that for the first time in 25 years US equity strategists are forecasting a down year.

Conventional portfolios did poorly. Diversification and a dollop of fixed income have caused misery. Energy and cash was the improbable winning combination. Meme stocks, tech and bitcoin (useless except when it’s going up) have slumped along with animal spirits.

But everyone who wants a job has one, albeit pay is lagging inflation. We’re not at war, although between Ukraine and Taiwan there’s plenty to worry about. And it looks like we handled covid rather better than China even though they had a head start on us since it originated there.

If today’s outlook compares unfavorably with 2008 or 1980, you have to conclude that people expect more out of life. Warren Buffet famously said that the secret to a happy marriage is to marry someone with low expectations. At moments of marital discord, I’ve pushed my luck by sharing this wisdom with my wife, who retorts that her expectations couldn’t be any lower.

Perhaps happiness in life requires lower expectations than evidenced by survey respondents to the University of Michigan.

The Alerian MLP ETF (AMLP) may be a flawed investment product, but it still has its uses. It serves as a reminder of what an ETF should not be, which is a payer of corporate taxes. As regular readers know, AMLP doesn’t qualify to be exempt from taxes like virtually all ETFs and mutual funds, because it invests almost all its assets in MLPs. Our Byzantine tax code recently led to a 3.9% NAV hit for AMLP investors as its advisor Alps reassessed what they owed (see AMLP Trips Up On Tax Complexity).

AMLP is inadequate as a long-term investment because its taxable structure ensures it will substantially lag its index. But it can still be worthwhile as a short. One example is when market appreciation turns unrealized losses into gains. Upon crossing that threshold the tax drag kicks in, such that it goes up at 79% of its index (ie 1 – the 21% corporate tax rate) but still falls with the market. Such asymmetry can make it a useful hedge on a long portfolio of MLPs or even a good short position (see Uncle Sam Helps You Short AMLP).

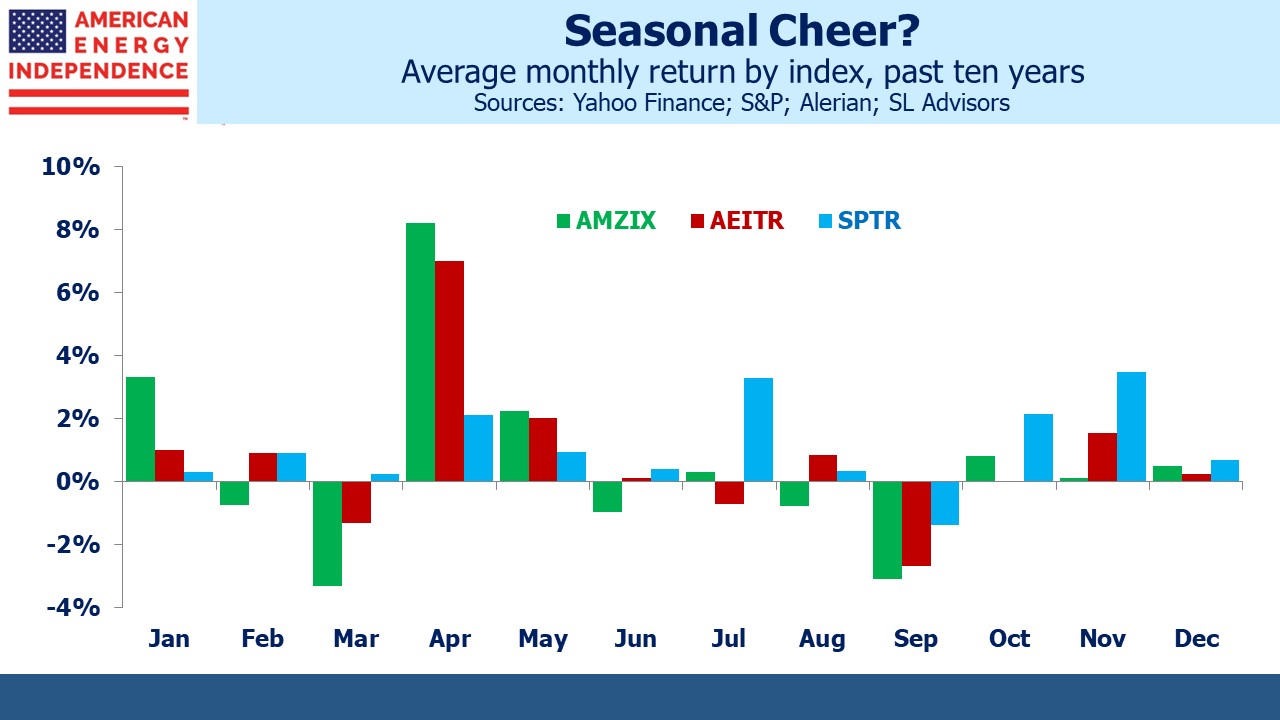

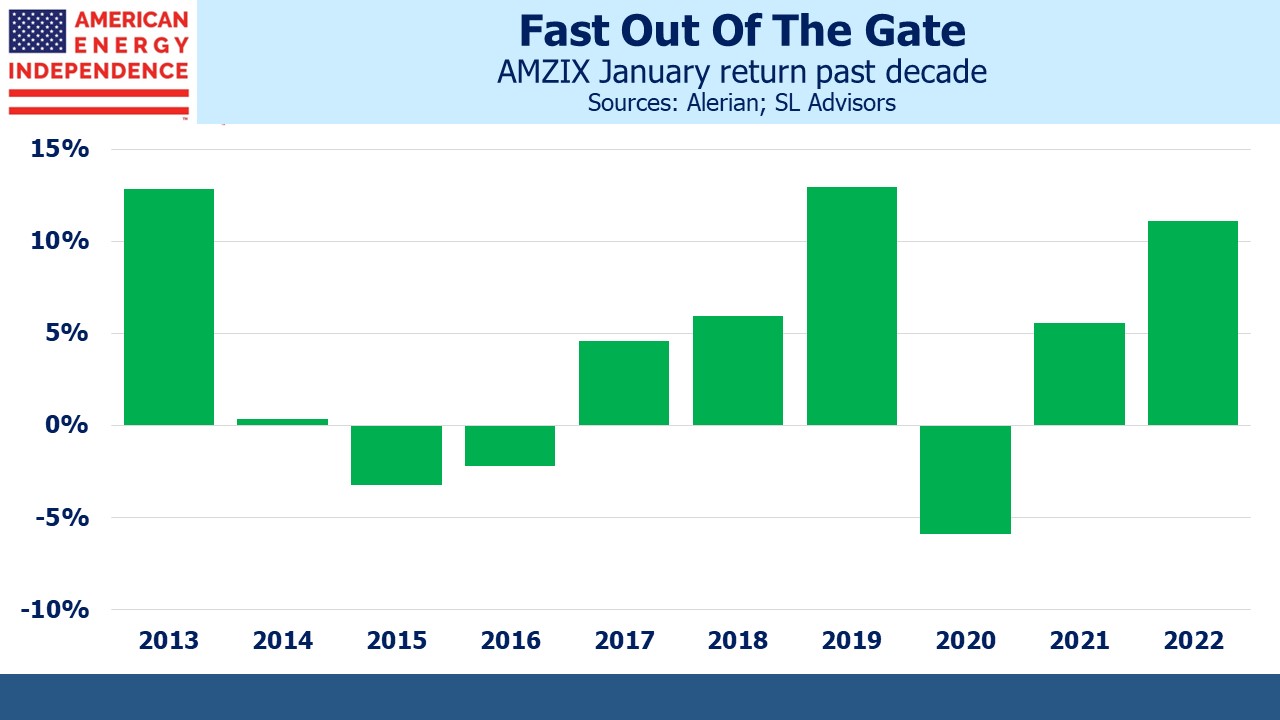

Another trade opportunity exploits the January effect. This used to be a feature of the S&P500 but has disappeared in recent years. It’s not that pronounced for the American Energy Independence Index (AEITR), but still shows up in the Alerian MLP Infrastructure Index (AMZIX), which AMLP seeks to track minus the tax drag and expenses.

The likely reason for a positive start to the year is that MLP holders tend to be K-1 tolerant, US taxable Americans. Because K-1s are a pain in the neck, if you’re contemplating selling an MLP December is better than January because you’ll avoid one last K-1 for the stub year. Similarly, purchases delayed until January avoid a K1 for the last month of the prior year.

Over the past decade, the AMZIX has averaged +3.3% in January, versus 0.5% for all months. Seven out of ten Januarys were positive, and only one was down more than 5% (2020). On average it’s up around half the time. If you’re inclined towards trading, buying AMLP now and planning to exit next month has an attractive risk/reward. And if you’re thinking of investing in the sector, delay is likely to mean paying higher prices. Just don’t make AMLP a long-term holding, because with its tax structure and absence of the biggest pipeline corporations it’s likely to continue underperforming the sector.

The seasonal January AMLP trade might benefit from a macro backdrop that suggests more investors than usual are hedged, defensive, in cash and hunkered down. In addition, the fundamentals for midstream energy infrastructure remain positive as tirelessly reported on this blog (see Energy – The Only Bright Spot In 2022). And if you already own AMLP, late January could be your best chance to swap it for a fund with a more investor-friendly structure.

More By This Author:

Merry Christmas And Happy Holidays!Can Pay Raises Keep Up With Inflation?

Is BREIT Marked To Market?

Disclosure: We are invested in all the components of the American Energy Independence Index via the ETF that ...

more