Where Did You Put Your Cash After The Fed’s Rate Hike?

Winter’s coming.

OK, not really. Winter’s already here.

But, for the investing world, things are starting to get a lot more chilly and scary. The storm clouds are rolling in.

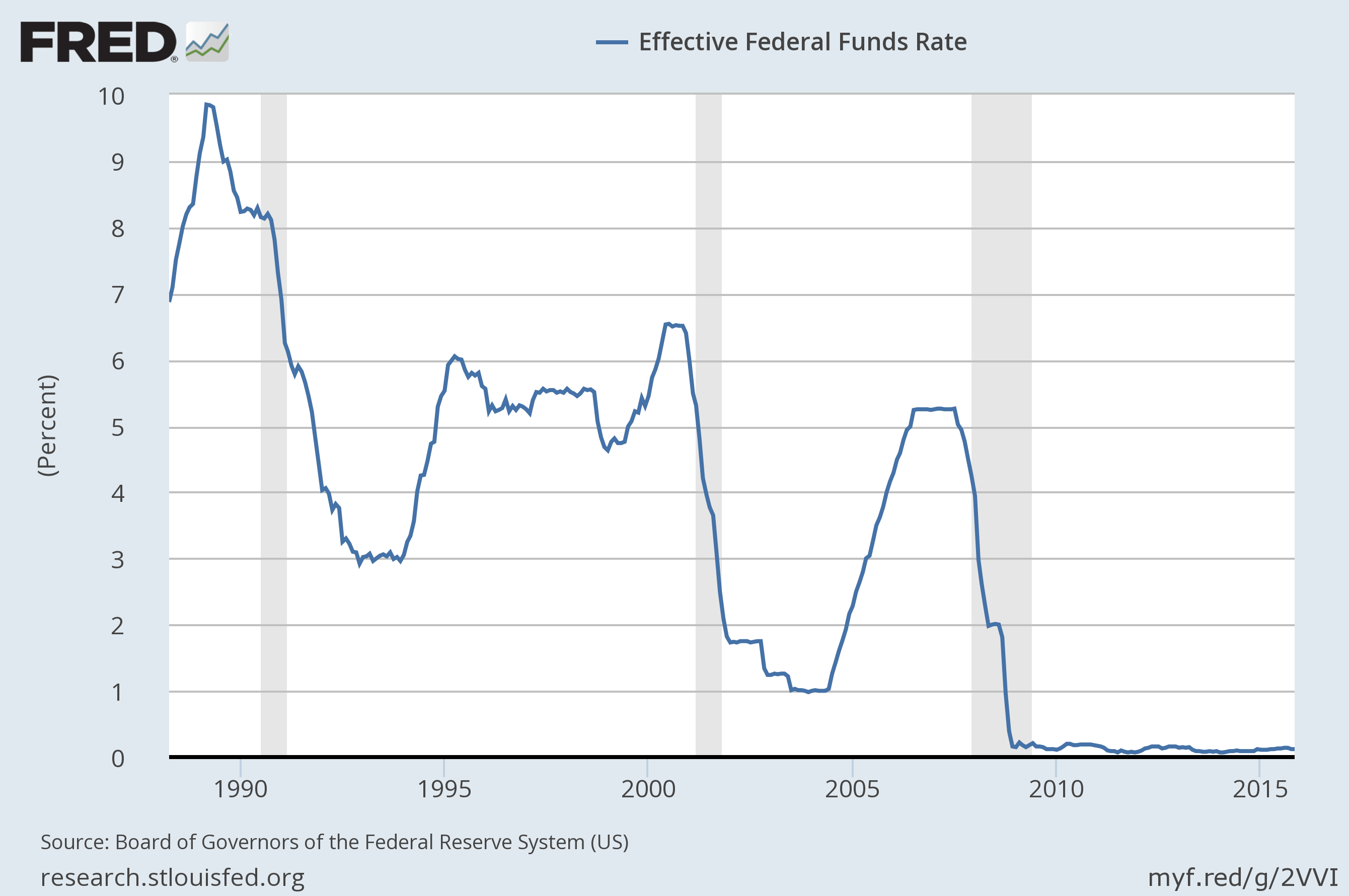

After seven years of holding short-term interest rates at roughly 0%, with no hikes for nearly a decade, the U.S. Federal Reserve Bank has officially begun to tighten up its lending policy again, slowly raising the interest rate it charges banks and other financial institutions to borrow from it.

On the surface, this is great news.

It means that the economy is finally showing signs of strength again, a full six years since the lows of the 2008 financial crisis. And it means that the unprecedented steps that the Fed took to keep us from the brink of financial ruin can finally be rolled back.

We’re on solid ground again. The economy is able to sustain itself. The Fed can get back to normal.

We should all be happy (and we are).

For the markets, though, this news comes with some dark clouds. There are reasons to be worried.

After years of life in a near-zero interest rate environment, no one is really sure what’s going to happen now that rates are rising again. Will the bull market stumble? Will lending dry up? Will the economy slip back into another recession?

(Yes, no and probably, but not for a while.)

And what about all of those investors and money managers out there who only know life with zero interest rates? What will they do with more normal policies from the Fed? Will they freak out?

There’s a lot we don’t know.

But this is happening, no matter what we think or want.

First, let me explain this whole thing simply.

The Fed lends money to banks, and banks lend money to each other based on the benchmark rates that the Fed establishes. When the Fed rate is low, savings rates are low. That’s because banks aren’t paying much in interest on those savings. There are better things to do with your money.

When savings rates are low, people put more money in higher risk stocks instead of savings. Make sense, otherwise their returns will suck. (Sorry banks, but a savings account that pays you less than 1% APR sucks. It’s a waste of time, and everybody knows it. Inflation is 2%. Do the math.)

But when savings rates are high (7%+), people put money in their savings account because it’s safer (it really is).

That’s why people say, “when interest rates go up, stocks go down.”

Oh my god!

So where are we now? The Fed Rate has been near 0% for six years (actually, the target is 0%-0.25%). This is (and has been) ALMOST FREE MONEY for banks … for years. And this has been driving stock market growth ever since 2008.

The Fed’s first step in normalization was to increase the target rate from 0% to 0.25%-0.50%. Not a big move.

They SHOULD raise the rate to 0.5% or even 2%. In that case, nobody will say, “Oh, now I should move out of the stock market and get 2% savings rates.” That isn’t really worth it either.

But we don’t know how this is going to go, or what they’re going to do.

And, by the way, the Fed only raises rates when every indicator suggests that companies are growing at a fast rate. So they have a good reason to do this.

The promise of easy money

If you’ve ever watched TV in the Washington, D.C. metro area you probably know who Matthew Lesko is.

He’s the guy who dresses up in a purple suit with yellow question marks all over it (I’m still not sure why) with a bow tie and films infomercials in front of the U.S. Capitol building about how you can get free money from the Federal government to start a small business, pay your taxes, and a long list of other things.

Whatever you needed money for, the government has a program to help you out. You didn’t really have to do anything to get it, just ask.

He would stand there on the Mall, frantically waving his arms around and yelling about FREE MONEY!, listing off all of the different government programs he had found that regular people could take advantage of.

(I last saw one of his ads around 2005, but he may well still be going with them. I’m not sure. He did used to drive around in a car covered with question marks, though.)

All of this was to sell the books he wrote to help people find and apply for these grants. Now he sells access to an online database of government grant programs.

Anyway, his whole message was about free money. From the government.

What a deal!

And that’s what the Fed has been offering to the market ever since the last recession.

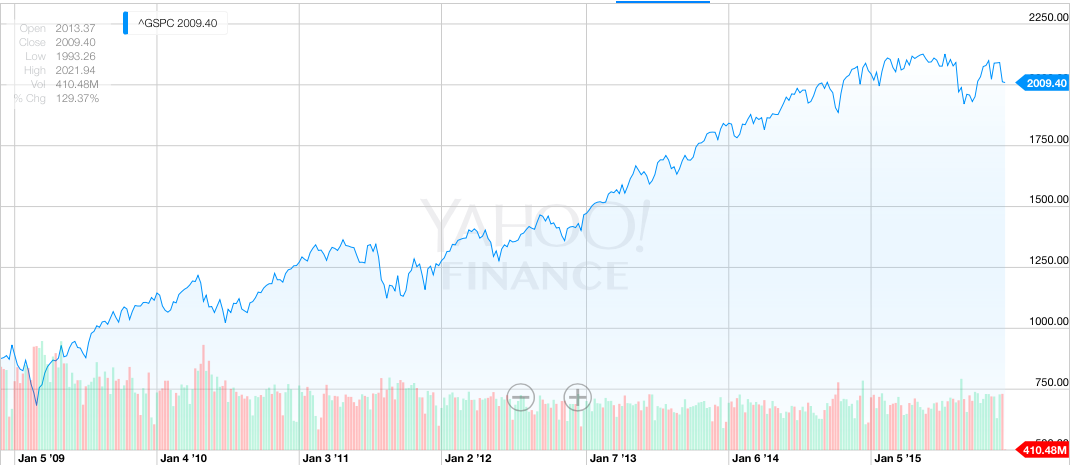

The stock market has been on a tear for the better part of seven years—up more than 170% since the March 2009 bottom—fueled by a lot of deep-pocketed investors as well as that promise I talked about earlier of free money from the government.

(Click on image to enlarge)

When interest rates are low, companies can borrow on the cheap to build their businesses or invest in other things. Their debt costs—“cost of capital”—go way down and they’re able to focus on growing their revenues.

It’s a great deal for them, and for investors.

But when this easy money goes away, thing should naturally slow down, if not fall into the red entirely. Cheap money is an addiction. Take away the goods, and things freak out a little bit.

Or maybe not

But history tells a different story.

Let’s look at recent times the Fed raised rates. Through most of the 90s the markets went straight up. In 1999, the Nasdaq 100 went up almost 100% over the next year (and value stocks continued to go higher ever after the crash).

From 2002-2007 the Fed raised rates every chance it could get. The market went constantly up.

And none of that was from such a low base of nearly 0%.

The longest Fed rate-hiking cycle since 1950 was between 1963 and 1969, when the Fed tightened and maintained rates for 69 straight months. The economy fell into a recession in December 1969, 77 months after the Fed started tightening. Stocks dipped only slightly as a result, before recovering by 1971.

But 1980 might be an even better example.

The Fed tightened for just four months that summer, but a recession still hit in mid-1981, just 11 months later.

That’s the quickest fall to date. The stock market didn’t even notice, rising steadily into 1981.

On average, the Fed has tightened its lending policies for 22 months at a time. And the average time from the start of tightening to the next recession is 41 months.

What does all this mean for stocks?

One thing the Fed always says is that investors shouldn’t focus on when it starts raising interest rates but, rather, how aggressively it does it.

Steep hikes tend to lead to more undesirable outcomes (e.g. bear markets, recessions, fear and mayhem in the streets, etc…), while slow, steady increases are more easily absorbed by the market.

We’re on the slow and steady path so far, but who knows what they future will hold.

What does that really mean for investors? What should we expect to see from the various parts of the economy as this unfolds?

1. The stock market may slow down, but it will still go up.

I once wrote software that basically analyzed what’s happened to the stock market after every rate hike since World War II. The result was that when a rate hike cycle starts, the market doesn’t go up as much as normal, but it DOES still goes up.

The research says that stock prices jump a lot—as much as 14%—heading into a rate hike, flatten out for about 6-8 months after the hike, and then return to normal after a year and a half or so.

So…that’s really a non-issue.

The thing to know is that, as the Fed continues to normalize its interest rate policy, stocks will begin to trade more on their fundamentals and less on the availability of cheap, easy money from the Fed.

This will expose the real winners and losers.

Even in the last cycle, which started in 2004, the market didn’t even peak until November 2007, so that was three years of straight-up return after rates were hiked. Now, there’s more volatility, but who gives a shit? We’re long-term thinkers, so as long as stocks keep going up, that’s a good thing.

We’ll know which businesses are solid and on the right track, and which are just floating on the bubble of easy money to make themselves look like good investments.

The stocks that do well through this tightening process will be set to take off in the next couple of years.

2. We’re going up from 0% interest rates, which is unprecedented.

That’s never happened before, so it’s not like a quarter of a percent or a half of a percent really makes that big of a difference.

The reason rate hikes affect the stock market is because people start saving money instead of buying stocks. It becomes safer to save money than buying stocks. But in terms of that, a half a percent doesn’t really compete with stock market returns, so it’s sort of a moot point unless we get back to pre-crash interest rates, which the Fed has strongly signaled that they’re not going to do.

The economic reasons why rate hikes affect the stock market do not apply on this rate hike cycle.

Near-zero interest rates are unprecedented, so the rise out of those rates will be unprecedented too.

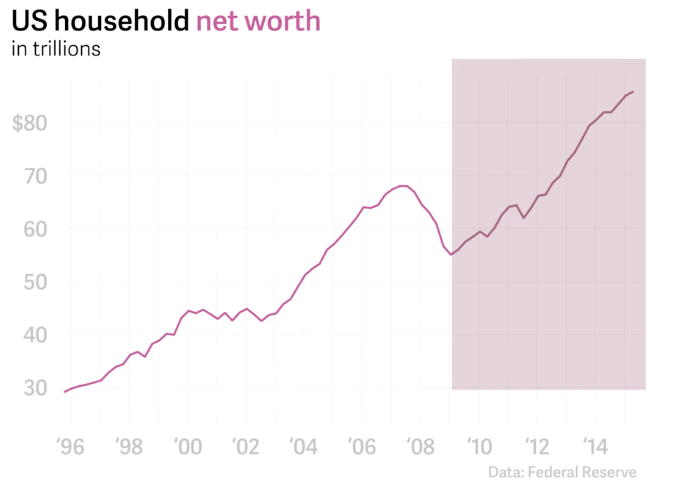

3. It means our economy is in good shape.

The only reason you’d ever even want to do a rate hike is because the economy is booming.

We’ve cut unemployment in half in the past few years.

via: qz.com

Earnings are at an all time high.

via qz.com

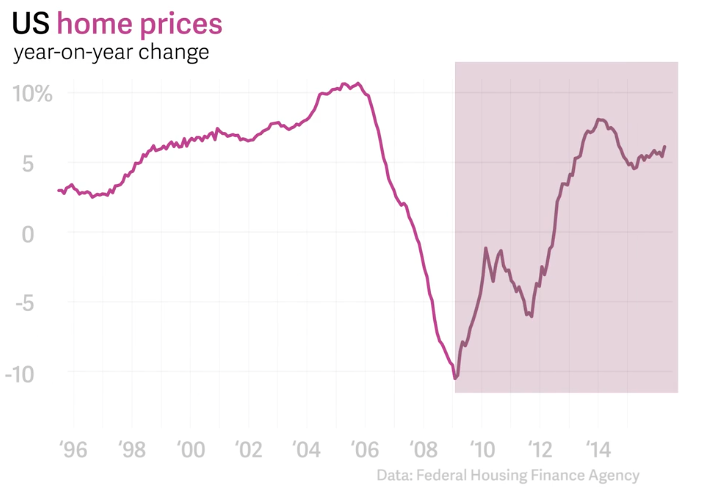

Home prices have finally rebounded.

via qz.com

When the economy is doing well, it’s a good thing, not a bad thing. So that’s the real fundamental story of why the stock market tends to go up after rate hikes.

And I wouldn’t even call this a real rate hike; we’re just getting back to some kind of normalcy.

4. It’ll mean a stronger dollar.

As long as people believe that the dollar is strong, then foreign money will flow into the United States.

Usually, foreign money coming into the United States is coming from people lending the money to the United States because rates are up. But in this case, more of the money that will come to the United States is going to end up somewhere. Some of it will end up in bonds, at low interest rates still, and some of it will end up in the stock market.

This will be good for stocks because it will mean more available capital to invest and, over time, higher prices.

5. Saving rates will go up.

This doesn’t necessarily mean anything for the stock market, but it does mean that more cash will be available for the stock market in the short term. When people put money in a savings account, they don’t necessarily put it in stocks.

Remember those sub-1% savings account rates? Consider them a thing of the past (eventually).

I remember a time years ago—and this is so hazy in my memory that I’m not even sure if it’s true anymore or not—when I was getting 5% in interest on a high-yield savings account.

That’s amazing!

(It’s so amazing that I just looked it up to confirm that it really happened, and it did!)

In an FDIC insured account! Guaranteed yield.

Wow, that was really something.

But that was a long time ago, and most savers—even of the high-yield variety—are lucky these days to break 1%. Banks can get the money they need very cheaply from the Fed, so why would they bother paying out an attractive savings rate to generate more deposits?

No more. Rates on savings accounts will—repeat: will—rise along with the Fed’s rates. Maybe not as high as that 5% (still, amazing), but a lot better than 1%, and that will be great for a lot of everyday people who hold money in savings accounts.

But again we’re confusing this rate hike with other rate hikes. This doesn’t even really count as a rate hike.

If you compare it with the 7% interest rates we had pre-crash, we’re only going to go up to like a half a percent, and I think we’re going to max out at 3%. At least that’s what Janet Yellen has signaled. It’s still much lower than historical rates; 3% would normally be after 20 rate decreases, not after a bunch of rate hikes.

So even at the peak of what we think it’s going to be after this rate hike cycle, we’re going to be in not normal rates. We’re going to still be at historically low rates.

Again, volatility will increase, but the stock market should rise as well.

6. Companies that outsource will become more profitable.

There’s been this huge trend in the United States with outsourcing, so companies that outsource to cheaper economies, let’s say Third World economies, will make more profits as a result of the rate hike.

That’s been flattening out lately because the dollar has been so weak since the rate decreases, but if the dollar suddenly gets a lot stronger then it will make companies that outsource much more profitable, which is ultimately good for the stock market.

The flip side of that is that companies that sell abroad, which has skewed greatly in the favor of multinationals, those companies won’t do as well with a stronger dollar because foreigners will buy cheaper foreign-made products instead of U.S.-made products. Again, it’s not just because of hiked rates.

A strong dollar isn’t a bad thing, so if you can find companies that outsource more, those stocks will likely do well as rates rise. The companies that outsource but sell domestically are the winners here.

7. Banks will do better

After a rate hike, at least initially, banks do well.

People look at financial institutions and they’re like, “OK, rates are going up, so they’re going to do better. They’re on the front lines of this.”

And banks are going to be more willing to part with their money with a higher federal rate. Because they’re paying out so much more, there’s less incentive for them to hold on.

For instance, right now there’s zero incentive for them to lend because they pay zero percent in savings accounts, and the Fed almost pays them to do this. So there’s really no incentive for banks to lend money.

But now there’s more incentive for banks to lend, so they’ll start making more money.

This will help not only their stocks, but also the companies that they eventually lend to.

But what about bonds?

Everyone is worried about bonds. Rate hikes ruin bond yields, they say.

True, bonds and interest rates have an inverse relationship. As rates rise, the prices on bonds actually go down, because older bonds that come with lower coupon rates (which are based on interest rates at the time they’re issued) don’t just lose value, they become completely undesirable.

Think about it. If you’re a bond investor, what would you rather do: buy a bond paying 10% today, or a bond that was issued yesterday and pays 5%?

It’s a no-brainer.

Higher rates really do drag down bond prices, and it happens fast. Much quicker than it does with stocks.

But it’s not the end of the world. For the most part, the higher rates will cause the different in yields between longer- and shorter-dated bonds to shrink, flattening the curve between the two and effectively flattening the market.

So it’s another non-issue, especially for long-term investors like us.

Possible concern

The one thing I worry, which is good for the consumer but not good for the stock market, is that I already think there’s deflation in the economy.

Whereas the reason you do a rate hike is to battle inflation. A rate hike encourages deflation. So I think there is a danger that down the road with these rate hikes we could start seeing more deflation.

I don’t know if that’s true, though. I think deflation’s happening naturally because of increases in productivity due to computers and the Internet and cheaper energy and all these other things.

But rate hikes could trigger more deflation. It happens. It’s a risk.

Really the Fed doesn’t need to do anything, we’re looking good. But they’ve signaled so much recently that they’re going to do a rate hike that it had to happen.

This isn’t 2009

In March 2009, the market hit an all-time low.

Fortunately, I ended it and saved the world.

I lived at 40 Broad Street, directly across from the New York Stock Exchange.

On March 9 I went out and bought hundreds of Hershey’s chocolate bars. Chocolate makes people feel like they are in love. And willing to take risks.

All of the traders walking into the exchange were depressed. They were all looking at the ground.

I started to approach them with my chocolates. At first the guards stood up and gripped their guns. Dogs were barking.

But then I started handing out the chocolates. Traders would look up, smile, and take the chocolate. Nobody refused me.

And yes, that day was the bottom of the market. I documented on Twitter before I started handing out and when I was done.

BUT, I can’t take all the credit.

People blame the 2009 crash on the housing crash. This is not true.

Housing prices peaked in 2006. The housing crash was only one small piece of the puzzle in the 2009 crash.

I won’t get into all the details of how banks account for mortgage debt.

But basically, the FASB (financial accounting services board) changed the rules mid-flight on how banks should account for their debt. It was a horrendously strict rule change that forced banks out of business.

When did they make this rule change? Late 2007, at the peak of the market. Then the real crash happened: the banking crisis.

Everyone begged them to change the rules back. When did they change it back? March 2009. Coincidence? The market went straight up.

Stocks are over

But who cares. Stocks aren’t how you make money these days anyway.

Really.

In 2001 and 2002 I lost all my money through bad investing. The same thing happened to me on a couple of occasions after that.

I learned a lot from that experience. The first is that the three most important three words in investing are: “I don’t know.” If someone doesn’t say that to you then they are lying.

The second: ALL OF WALL STREET IS A SCAM. There are zero exceptions.

The CXO Advisory Group polled the predictions of 500 investment strategists and pundits, and “the experts” had a 47% success rate. Good luck if you listen to any of them.

That’s the bad news. But where does that leave average, everyday investors looking to profit in the markets?

You have to be smart.

You have to be creative.

You have to think outside of the stocks-and-bonds-and-mutual funds box and look for the real opportunities in the market. Those sectors that are still well priced and offer potential for big gains. And then you have to hold those investments, for a long, long time.

The Fed raising rates isn’t going to change any of this.

For instance, if you still want a return, you’re still not going to get 2%. You still don’t want your 2% in savings accounts. You need to find an investment that will do better than that, without snagging you in Wall Street’s net of fees and rigged trades and everything else.

But here’s the truth. I used to write about money stuff a lot because I wanted investors, or I wanted to sell books, or get speaking engagements. Now I want none of that.

I HATE WRITING ABOUT FINANCE NOW. Because it’s almost all bullsh*t and I don’t want to be like the other BS.

But I get worried that in a world of increasing economic uncertainty that more and more people are getting “stuck” and getting lied to and are scared about what is happening.

Most people will think I am giving bad advice. That’s fine. I probably am. I am just trying to avoid the BS and I hope you are also.

Too many people I know are nervous and depressed.

There’s nothing else to know about investing your money. If your bank tries to give you any advice just say, “thanks but I’m OK.” If they want you to put your money in a savings account, even “so you can get the interest,” I would politely decline. There’s a reason they are asking you to do this and I have no idea what it is but it’s probably not good for you.

You won’t get rich investing your money but you can do very well. And if you combine that with investing in yourself, you will get wealthy.

Here’s what’s going to happen, though. Rising interest rates could change things, and they probably will drag some investments down and boost some higher.

The key for us, as long-term value investors, is to keep looking for investment opportunities that are statistically trading for much less than their net asset values. That way, no matter what rates do and no matter how the market reacts, we’ll be on solid ground.

My strategy isn’t based on any one particular interest rate goal (in fact, it will work better than ever with the volatility that comes after any rate hike increases).

This material is provided for informational purposes only, as of the date hereof, and is subject to change without notice.This material may not be suitable for all investors and is not intended to be ...

more

I don't think raising the fed rate will encourage banks to lend more money (point 7). You say there is no incentive to lend if the fed rate is zero. Say I'm a loans manager. A guy walks in and wants a car loan. I get the money he needs at zero cost to me and lend it to him at 10% interest. No incentive, I don't think so! If the fed raises its rate to 2% you say the bank will have more incentive. How so? I get the money from the fed at 2% and loan it out as a car loan at 12% interest. Where is the greater incentive to lend?

You already give a car loan to any warm body. But easy money is not so prevalent in the housing market, Gerald. Raising interest rates would give banks more incentive to do a 30 year loan. But realize that interest rates going up could destabilize banks that bet on LIBOR floating rates while the counterparties are forced to bet on the fixed higher rates.

I don't think it is going to work the same as in the past for bonds, James. JMO. But there is a shortage of treasury bonds, long bonds especially. And those are being held on to They are used as collateral in the derivatives markets and I know CATO and others say that it is a small part of the total bond market, but I don't really believe that. I am looking into that more and more. We will see going forward.

Why don't you believe it?

Hi Carl, good question. I don't believe it because the estimate for bonds as collateral in the derivatives market in 2013 was between 800 billion dollars and 4 trillion dollars of bonds needed. m.treasuryandrisk.com/.../demand-for-swaps-collateral-could-bolster-bonds

This is the best explanation I've seen yet. A must read for all.