It would be easy for those who have decided to buy gold and silver bullion to lose heart over the precious metals, had they seen how prices reacted to Chairman Powell’s comments, last week.

However, to do this would be very short-sighted. Whilst Powell may well have signaled that the Fed will stay on this path of tightening this does not mean that they have resolved the issue. Rather, it likely means that the Fed is reacting a little too hard, a little too late and this will almost certainly pave the way for gold and silver investors.

Central Banks come under scrutiny

The Federal Reserve of Kansas City hosted its annual policy symposium for central bankers on Thursday and Friday of last week.

This was the 45th year of the annual event that is held in Jackson Hole Wyoming. During turbulent markets, a central banker’s every word is scrutinized to extract information from presentations on future policy moves.

The highlight of this year’s conference titled Reassessing Constraints on the Economy and Policy was Fed Chair Jerome Powell’s Friday morning presentation.

Powell’s short presentation focused on the Fed’s continued campaign to bring inflation down close to its 2% target.

Gold and silver prices both declined sharply as interest rate expectations rose (along with the US dollar and real rates). US equity markets also declined with the S&P 500 Index plunging 3.4% on Friday.

Key statements from Powell’s presentation included:

Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy …

We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent …

Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions …

Powell’s statement regarding what the September 20-21 meeting might bring in the way of additional hikes reiterated what he said at the July Fed Meeting

that another unusually large increase could be appropriate at our next meeting. We are now about halfway through the intermeeting period.

Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook …

While the lower inflation readings for July are welcome, a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down …

In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, [this is] not a place to stop or pause …

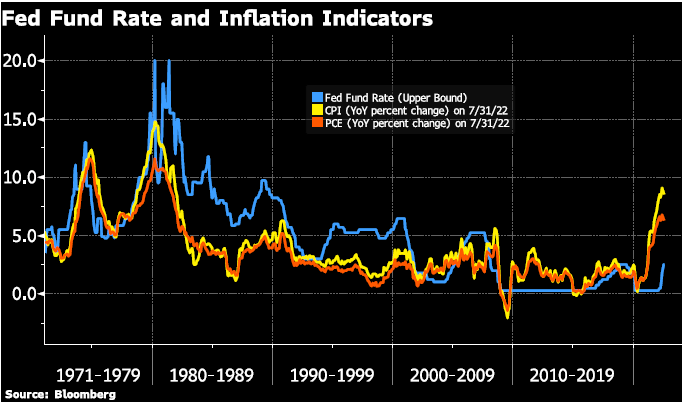

The lower inflation reading Powell referred to was that both the Consumer Price Inflation Index (CPI) and the Personal Consumption Expenditure Index (PCE) came in slightly lower in July than June, the CPI at 8.5% compared to 9.1% in June and the PCE at 6.3% compared to 6.8% in June.

It is too early to know if the lower numbers are merely a pause in inflation or a turning point into inflation declines.

Either way, the Fed remains well behind the inflation curve with the fed funds rate only in the 2.25% to 2.50% range.

However, the Fed and other central banks also must consider slowing economic growth, wobbly housing markets, lower equity markets, and rising debt servicing costs for both households and governments.

Especially in Europe, the rising costs of natural gas and low storage supply are already stretching household budgets to breaking point even before winter sets in.

Fed Fund Rate and Inflation Indicators

Fed Fund Rate and Inflation Indicators

Central Banks have Lost their Sense of Reality

Central banks have printed so much money and kept interest rates low for so long that the unwinding of the damage is going to take time. As Powell stated there will be pain as households and governments sober up from the long party of low rates.

The main problem now is that central banks have lost their sense of reality. Also, central banks are likely to now push rates too high, resulting in a deeper recession than otherwise.

According to the CME Group’s FedWatch Tool, the probability of another 75-basis point hike by the Fed at the September meeting has increased back up to almost 70 percent.

The probability that the fed funds rate will end the year in the 3.75% to 4.00% range is up to 60% (this is 1.5% higher than the current rate). Markets are currently placing the highest probability on the fed funds rate remaining in this range or being lower by July 2023.

However, these probabilities do change quickly as new data points are released. Before the September meeting, there is an employment report scheduled for Friday. Also, CPI data for August to name a couple of the data releases still to come.

The bottom line is gold and silver investors still require patience. However, the day of reckoning will come, and prices will break out of their sideways channel.

Circling back to the Jackson Hole Symposium we leave the reader with the last quote from economist Edward Kane from the 1983 symposium. This quote seems very relevant to the current monetary policy environment:

“ Depending on which economic indices one emphasizes and how one takes into account other potentially relevant developments, the (October 1979) change in FOMC policy framework can be portrayed as spectacularly successful, relatively unimportant or absolutely disastrous in its effects.”

Kane went on to say that in his view it was the third option. Remember this was just after back-to-back recessions, the second of which lasted for 16 months. Some of the reasons Kane viewed the policies as “disastrous in its effects”. This Includes generally slower economic growth rates, higher unemployment, bankruptcy, and foreclosure rates.

If you enjoyed this little piece of insight into the kinds of discussions we have in the GoldCore office, then why not subscribe to our YouTube Channel. There you will find a host of interviews and discussions from the great minds, commentators and experts in the financial and precious metals markets. You can see our latest interview with Jim Rickards and Marc Faber, here.

More By This Author:

The Russian Gold StandardHistory Of Money And Evolution Suggests A Crash Is Coming

Why We Couldn’t Be Happier That Gold Is Boring

Comments

Log in or sign up to join the conversation.