U.S. Global's Ralph Aldis On The Life-Changing Magic Of An Asset Allocation Plan

TM editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

You have to have a plan and stick to it. This wisdom from U.S. Global Investors Fund Manager and TalkMarkets contributor Ralph Aldis is true for investors and mining companies. And it may be even more true when the market seems to be careening from one disaster to the next. In this interview with The Gold Report, Aldis shares seven companies he is sticking with come low gold prices or a high Purchasing Managers Index.

The Gold Report: This year started with a bang as China's machinations rocked markets all over the world and set off a gold rally. Is that sustainable? What did we learn?

Ralph Aldis: China was the main driver of the volatility that started out the year. The economy is not collapsing. Growth will just be a little bit slower than expected.

I also think people are losing faith that the Federal Reserve will be able to maneuver the markets this year. What's really been disturbing to me is how much central banks all around the world are intervening in stock markets. To me, that's a recipe for disaster.

Gold was the beneficiary of these dark notes. Investors need to understand that, regardless of what the pundits are saying. All investors need an asset plan designed around individual timelines. Then they have to stick to it and rebalance.

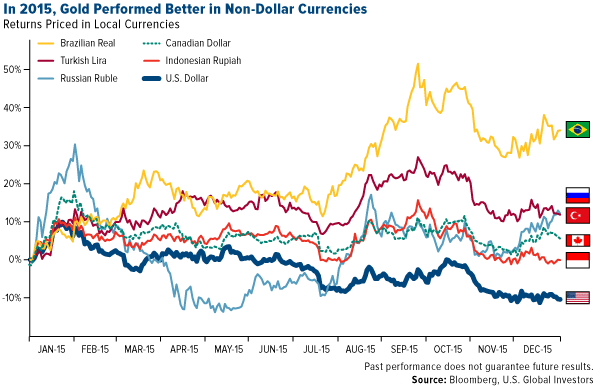

TGR: Frank Holmes pointed out in his Frank Talk that gold actually performed well in 2015 in some currencies. Where are you looking for gold to do best this year? What does that mean for North American investors?

RA: The Canadian dollar was a standout last year. We are looking at $1,600/ounce gold prices in Canada right now. The same is true for Australia. In other countries—Russia and Brazil for instance—it has been even more pronounced because of the ruble and the real, but there just aren't that many names to invest in there right now.

I think the Canadian dollar is still going to weaken a little bit more this year. We saw the Bank of Canada hold off on cutting rates at its last meeting. I still think the bank is going to end up having to cut rates at some point in the not too distant future. The Canadian dollar will get weaker and that will be very positive for the metals prices. On the Aussie side, I see the same trends happening. Gold companies operating in those regions have an advantage over some of the other miners out there.

TGR: And do you believe the U.S. dollar will continue to be strong?

RA: Yes, but I don't think we're going to see a runaway U.S. dollar. Cornerstone Research has shown that historically the dollar rallies up into the first rate hike and then generally tends to fade after that. With the emerging markets' currencies down so much, that's probably going to trigger some growth in those regions, too.

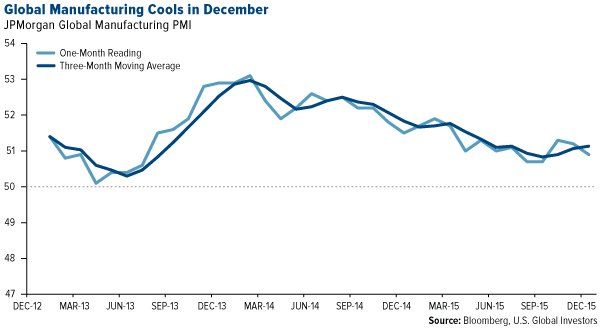

TGR: One of the things that you and Frank follow is the Purchasing Managers Index to measure economic health. What is the cross-above trend telling you about global growth?

RA: The most recent global manufacturing chart showed cooling in December, which resulted in the one-month reading falling below the three-month moving average. The average had been rising slightly since September, but the last two data points from November and December were kind of trending down. The recent market turmoil indicates we are probably still looking at some weakness this year.

TGR: The other thing that you've written about is the strategy of royalty companies to buy when the streams are on sale. What companies have been the most active? What does that tell you about where we are in the cycle?

RA: That's an interesting dilemma right now. The royalty companies have traditionally been one of the best places to be long term, and I think that still probably holds because they have a very diversified risk portfolio. The big challenge now is they don't have the capital available to do more. They could borrow. Franco-Nevada Corp. (FNV:TSX; FNV:NYSE) has done that, but historically one of Franco's strengths is that it doesn't like to have any debt on the balance sheet.

Another one that's been pretty active is Osisko Gold Royalties Ltd. (OR:TSX) (OKSKF). It is taking a completely different approach by working in the junior gold space to line up future royalties. That could be a very successful strategy long term.

Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX) is facing a situation similar to Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) when it wrote off $200 million ($200M) on Goldex, and the market took $2 billion out of the market cap. A year later, Agnico was a great entry point and subsequently turned into one of the best performers. Royal Gold's share price has been hit because of fears over Thompson Creek, the Phoenix royalty and so on, but that may be oversold.

Silver Wheaton Corp. (SLW:TSX; SLW:NYSE) has some tax issues hanging out there that make it difficult to go out and tell the story. But the controversy could result in a very good entry point for some people.

TGR: With all of this going on, how are you adjusting the U.S. Global portfolios to prepare for what could happen in 2016?

RA: We haven't changed too much. Most of our big positions are still oriented along the same weightings. If we do get a gold rally, some of the highly leveraged names may be the bigger beneficiaries. I always have to be cognizant of that. Last year, I avoided some of the highly leveraged names, but that may change this year. I do feel that we're getting closer to a turning point.

There are a lot of reasons for that. The Fed is trying to raise rates. In a news article recently, Goldman Sachs advised selling the 10-year treasury bonds, and Morgan Stanley was saying buy the 10-year because its analysts are expecting 10-year yields to drop another 50 or 60 basis points. All of this stress could lead to a big pull away where the market just loses confidence. Historically, when the Fed and all these governments make a mistake, people decide it is a good time to own some gold.

TGR: Let's talk about some of the specific gold mining companies in your portfolio that are doing well or have significant catalysts coming up.

RA: Gran Colombia Gold Corp. (GCM:TSX) (TPRFF)is one that we've been involved with for a number of years. The challenge of operating in Colombia isn't as much the narcotics drug lords as it is the socialist slant of the government. We have seen a restructuring of the board members, and we would like to see the management team strengthened. Rodney Lamond, Mark Ashcroft and Mark Wellings are three new board members. Wellings was one of the people who ran GMP Securities for a very long time for Griffiths McBurney & Partners. He's highly respected on the Street. All three people have a great track record. Gran Colombia has also formed a technical committee of the board. Having a plan and executing on that plan will be important for Gran Colombia going forward. With these new board members, I think we could have great opportunity on this one.

The common share price is very cheap. The real play right now is to buy the depressed debt securities because those will see the rerating first. The silver notes have a 1% coupon, but the gold notes will have a 6% coupon. The yields of 25% to 30% are very attractive in this market. So once the market gets some clarity on how Gran Colombia is going to be led, that could be a game changer for the company.

TGR: In addition to the changes on the board, Gran Colombia also just completed a debt restructuring. How important is that for reducing costs?

RA: That's a big deal because bringing down the interest payments will free up a lot of cash flow to do more things. It will give the company a lot of flexibility on the operating side.

Plus the Colombian peso has fallen quite a bit. That is another example of where a company benefits from paying its labor with the Colombian peso, but profiting from a higher gold price.

TGR: Let's talk about another one that could do well in 2016.

RA: A company we have talked about since we've been doing the interviews is Klondex Mines Ltd. (KDX:TSX; KLDX:NYSE.MKT). Success really depends on the people running these companies. It was a game changer when Paul Huet, CEO of Klondex, came on the scene three years ago.

Klondex recently completed an acquisition and the market got jittery. It bought the Rice Lake mine out of bankruptcy for around $30M from a controversial name, San Gold Corp. (SGR:TSX.V). There is still some $20+M of mobile mining fleet at the mine site and the mill was on care and maintenance. I think the real problem with San Gold was that it was trying to grow this asset beyond the natural mining rate. The trouble is if a company upsizes the mill and the underground operation can't keep up, it is forced to mine lower grades to get the tonnage and that is a losing proposition. Klondex is looking at turning it into perhaps a 50,000 ounce (50 Koz) producer, maybe 70 Koz. That is much more economic.

TGR: We did see a little bit of a selloff when the acquisition came. Is there going to be some kind of a catalyst in 2016 that will prove to investors that this was a good decision?

RA: Klondex is going to re-evaluate the mine plan. In nine months or so we should have a better understanding of how it will operate. We may have other catalysts before that related to Fire Creek and Midas exploration results. That is why I'm pretty confident this thing is going to be a very good performer for us this year.

TGR: How about an update on another one we've talked about before?

RA: Integra Gold Corp. (ICG:TSX.V; ICGQF:OTCQX) is becoming more timely with each Eldorado Gold Corp. (ELD:TSX; EGO:NYSE) press release. Eldorado took a small stake in Integra. With the write-downs the major is taking, I think it makes more of a case that at some point Eldorado will take this company over provided Integra finds the right stuff. I think that this year could be very important for Integra.

Integra also has its Gold Rush Challenge that it's going to highlight at the 2016 PDAC Convention. Rob McEwen did that with Goldcorp Inc. (G:TSX; GG:NYSE) and it had great success. You put up some cash for experts outside the company to look at the data and you don't know what you're going to get, but you may get an answer that's much better than what just one firm would recommend. I'm excited about this one.

TGR: Is the upside the harvesting of crowdsourcing insight or the publicity that comes from doing something out of the ordinary or is it a combination of the two?

RA: I think a combination. It does bring more eyes to the stock. I'm hopeful that a great target comes out of the exercise, but Eldorado making a move to consolidate its ownership is really what I'm looking for.

TGR: Let's talk about another one.

RA: Newmarket Gold Inc. (NMI:TSX; NMKTF:OTCQX) is a company that has a couple of assets in Australia where people have never really paid much attention. AuRico Gold had these and I guess Northgate Minerals before that. When Alamos Gold Inc. (AGI:TSX) (AGI) took over AuRico, it didn't really have any interest in those assets. But recent drill results are hitting some high grades that could result in a longer mine life at Fosterville.

The other thing is that the management team is pretty smart and they understand the value drivers for getting a company's share price higher. So I'm positive on this one. It's one of the few gold stocks that has actually been able to go up in the last year.

TGR: Is that mainly because of the Australian dollar or is it because of the new mine plan and the management?

RA: The Australian dollar has been a big tailwind, so that's part of it. But the new mine plan and the additional drill holes are very promising for a long mine life. Some of these mines can go on for 100 years with underground operations. So I'm pleased with this one.

TGR: How about one that's a near producer?

RA: Pretium Resources Inc. (PVG:TSX; PVG:NYSE) is getting there; 2017 is the expected date for Brucejack to be in production. It continues to put out very good drill holes. After the drama with the initial bulk sample in late 2013, it delivered 4 Koz as estimated. The company just released the fifth set of fan drill definitions and it is continuing to hit. I think it had one hole that was 20,000 grams per ton (20,000 g/t). One of the brokers jokingly suggested measuring in number of Rolexes per ton. I think Pretium is doing the right work to understand the geometry of the ore body. That's so important. Pretium is getting the right three-dimensional picture of the ore and its distribution.

The great thing is it could literally mine here and repay all its capital in a modestly short period of time. Even after it depletes the high grade, it will still be a huge gold camp. Who knows where gold prices will be in 10 years? Maybe all that other 1 g/t gold will actually be worth something.

TGR: Does the company need to raise more money?

RA: Working capital as of Sept. 30, 2015, was $432M. We should get an updated funding capital expenditure estimate for the project this quarter because there are other cost savings that will probably come in. Certainly, the exchange rate is very favorable. Sourcing the equipment with the market in a distressed state could lower prices as well. Pretium still has a little bit more funding to do, but I don't really look at that as a major headwind. I was very pleased with the deal that it did for this last set of funding where it negotiated with private equity. It also put a cap on the royalty. So the company has been very astute about trying to preserve the value for the shareholders, and the management team owns a lot of stock themselves. I'm pretty happy with what Pretium is doing.

TGR: Let's get an update on another long-time holding.

RA: I talked to Rye Patch Gold Corp. (RPM:TSX.V; RPMGF:OTCQX) CEO Bill Howald recently and he has been very busy. Funding hasn't been an issue because of the royalty on Coeur Mining Inc.'s (CDM:TSX; CDE:NYSE) Rochester Mine. He just picked up some additional land positions near the old Florida Canyon mine, which is owned by a large Asian operator. It is up for sale. I don't expect Howald to necessarily buy that, but he has a lot of land positions around that. So if a company does decide it wants to make a run at it, Howald certainly has a lot of land in that area.

Rye Patch also recently renegotiated its terms with the Barrick Gold Corp. (ABX:TSX; ABX:NYSE) group on the Patty project to give it more time. It is fairly complex geology and the company doesn't want to drill and make a mistake, so it is taking a little bit of extra time. Howald has a lot of irons in the fire. I've been very happy holding on to this company because it's been run very solidly and it doesn't have a funding issue.

TGR: How about one more?

RA: Tahoe Resources Inc. (TAHO:NYSE; THO:TSX) just released its 2016 production and cost guidance. I didn't see major issues there. I think at Shahuindo it was planning a 10,000 ton per day (10 Ktpd) plant versus a 30 Ktpd version, but in this environment, a company is probably better off risking less capital until it knows the conditions. Tahoe has actually underperformed year-to-date compared to its peers, but this is a company that is not going bankrupt and is run by good people who own a lot of stock. I think the stock is probably a reasonable Buy at this level. The worst thing would be if silver prices continued to drop, but if gold goes up, silver should follow that.

TGR: Are there some catalysts coming up on Tahoe we should watch?

RA: There are some more engineering studies going on. The bigger deal will just be continuing to operate and not have any big hiccups. The guidance may be overly conservative. It's hard to say. But Tahoe's management team has a lot of experience and has maneuvered a lot of markets before, so we're sticking with that one.

TGR: How about some last words of advice for investors looking to make the most of their portfolios in 2016?

RA: Investing is a discipline. I always stress the importance of an asset allocation plan and rebalancing that plan regularly. Gold is always an important part of that asset allocation mix, which so many investors just don't consider. Even brokers don't always know what's going to happen, so a good balanced asset allocation plan tethered to where you are in life is the key to building wealth.

TGR: Thank you for your time, Ralph.

Ralph Aldis, CFA, rejoined U.S. Global Investors as senior mining analyst in November 2001. He is responsible for analyzing gold and precious metals stocks for the World Precious Minerals Fund (UNWPX) and the Gold and Precious Metals Fund (USERX). Aldis also works with the portfolio management team of the Global Resources Fund (PSPFX) to provide tactical analyses of base metal, paper, chemical, steel and non-ferrous industries. Previously, Aldis worked for Eisner Securities, where he was an investment analyst for its high net worth group and oversaw its mutual fund operations. Before joining Eisner Securities, Aldis worked for 10 years as director of research for U.S. Global Investors, where he applied quantitative skills toward stocks, portfolio tilting, cash optimization and performance attribution analysis. Aldis received a master's degree in energy and mineral resources from the University of Texas at Austin in 1988 and a Bachelor of Science in Geology, cum laude, in 1981, from Stephen F. Austin University. Aldis is a member of the CFA Society of San Antonio.

Ralph Aldis, CFA, rejoined U.S. Global Investors as senior mining analyst in November 2001. He is responsible for analyzing gold and precious metals stocks for the World Precious Minerals Fund (UNWPX) and the Gold and Precious Metals Fund (USERX). Aldis also works with the portfolio management team of the Global Resources Fund (PSPFX) to provide tactical analyses of base metal, paper, chemical, steel and non-ferrous industries. Previously, Aldis worked for Eisner Securities, where he was an investment analyst for its high net worth group and oversaw its mutual fund operations. Before joining Eisner Securities, Aldis worked for 10 years as director of research for U.S. Global Investors, where he applied quantitative skills toward stocks, portfolio tilting, cash optimization and performance attribution analysis. Aldis received a master's degree in energy and mineral resources from the University of Texas at Austin in 1988 and a Bachelor of Science in Geology, cum laude, in 1981, from Stephen F. Austin University. Aldis is a member of the CFA Society of San Antonio.

Disclosure:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of

The Gold Report, The Energy ...

more