- The United States Gross Domestic Product is expected to grow at an annualized rate of 3.0% in Q3.

- The US economy continues to outperform its G10 peers.

- Investors anticipate the Federal Reserve will reduce interest rates by 25 bps in November.

The US Bureau of Economic Analysis (BEA) is scheduled to release the preliminary estimate of the US Gross Domestic Product (GDP) for the July-September quarter on Wednesday. Analysts anticipate that the report will indicate an annualized economic growth rate of 3.0%, matching the expansion recorded in the previous quarter.

Unveiling US economic growth: GDP forecast insights

This Wednesday, the US Bureau of Economic Analysis (BEA) is set to release the first estimate of the Gross Domestic Product (GDP) for the third quarter (July-September) at 12:30 GMT. Initial projections point to an annualized economic growth rate of 3.0%, in line with the expansion seen in the previous period and indicating a robust pace for the domestic economy, which continues to outpace its G10 counterparts.

The updated Summary of Economic Projections at the Federal Reserve’s (Fed) September meeting revealed several changes from June. The Fed’s median forecast for real GDP growth remained mostly steady at 2.0% for 2024, 2025 and 2026, and 1.8% for the long term.

The Fed also announced that it had raised the median unemployment rate projections to 4.4% for both 2024 and 2025, 4.3% for 2026 and 4.2% in the long run, up from the previous estimates of 4.0%, 4.2%, 4.1% and 4.2%, respectively.

Regarding inflation, the Fed reported that the median estimate for the core Personal Consumption Expenditures (PCE) price index was revised down to 2.6% for 2024, 2.2% for 2025 and 2.0% for 2026,from earlier projections of 2.8%, 2.3% and 2.0%.

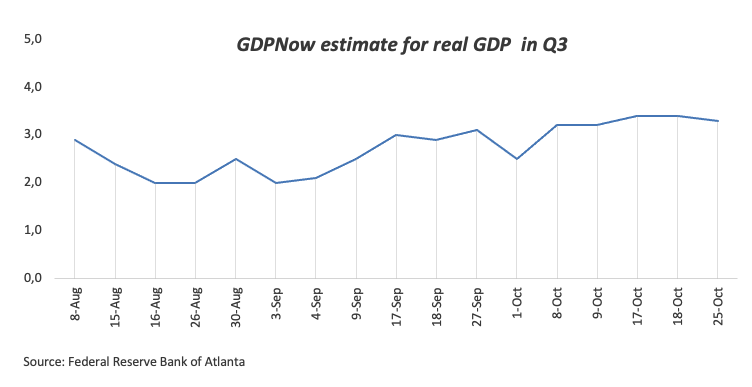

The latest GDPNow forecast from the Federal Reserve Bank of Atlanta, released on Friday, projects that the US economy expanded at an annual rate of 3.3% in the third quarter.

Market observers will be paying close attention to the GDP Price Index, which tracks changes in the prices of goods and services produced domestically, including exports but excluding imports. This index provides a clear view of how inflation is affecting GDP. For the third quarter, the GDP Price Index is expected to increase by 2.7%, up from the 2.5% rise seen in the second quarter.

Along withthe GDP Price Index, the upcoming GDP report will include the quarterly Personal Consumption Expenditures (PCE) Price Index and the core PCE Price Index. These metrics are crucial for assessing inflation, with the core PCE Price Index being the Federal Reserve’s preferred measure.

Ahead of the GDP release, analysts at TD Securities shared their insights: “US Q3 GDP strength is likely to persist with a 3% gain, driven by strong domestic demand and a resilient consumer base.”

When will the GDP print be released, and how can it affect the USD?

The US GDP report will be published at 12:30 GMT on Wednesday. In addition to the headline real GDP figure,changes in private domestic purchases, the GDP Price Index and the Q3 PCE Price Index figures could impact the US Dollar’s (USD) valuation.

Sticky inflation readings in September, combined with the still robust US labour market, have recently fuelled expectations for a smaller Fed rate cut in November.

According to the CME FedWatch Tool, a 25 basis points (bps) rate reduction in November is almost fully priced in.

Looking at the USD, a firm GDP could provide the Fed with additional justification to go for the small option at next month’s meeting. On the other hand, a disappointing GDP print—albeit unlikely—could motivate the Greenback to take a momentary breather, if any at all.

Pablo Piovano, Senior Analyst at FXStreet, gives his view on the technical outlook for the US Dollar Index (DXY): “Amidst the ongoing rally in the US Dollar Index (DXY), the next key target is the October 29 high of 104.63 (October 29). Once this region is cleared, the index could embark on a potential test of the weekly top of 104.79 (July 30).”

“On the downside, strong support remains at the year-to-date low of 100.15 (September 27). Should selling pressure reappear and the DXY breach this level, it may retest the psychological 100.00 milestone, potentially leading to a drop to the 2023 low of 99.57 (July 14)”, added Pablo.

More By This Author:

Japanese Yen Hangs Near Multi-Month Low Against USD Amid BoJ Rate-Hike UncertaintyUS Dollar Steady Ahead Of Key Data, Mixed JOLTS

USD/JPY Is Testing 153.90 High Ahead Of US Labour Data

Comments

Log in or sign up to join the conversation.