Market Analysis

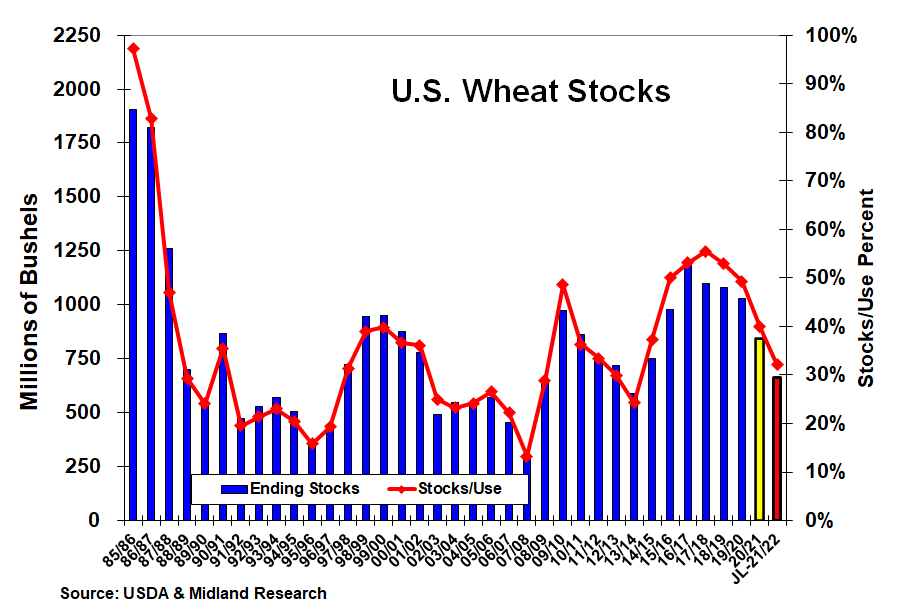

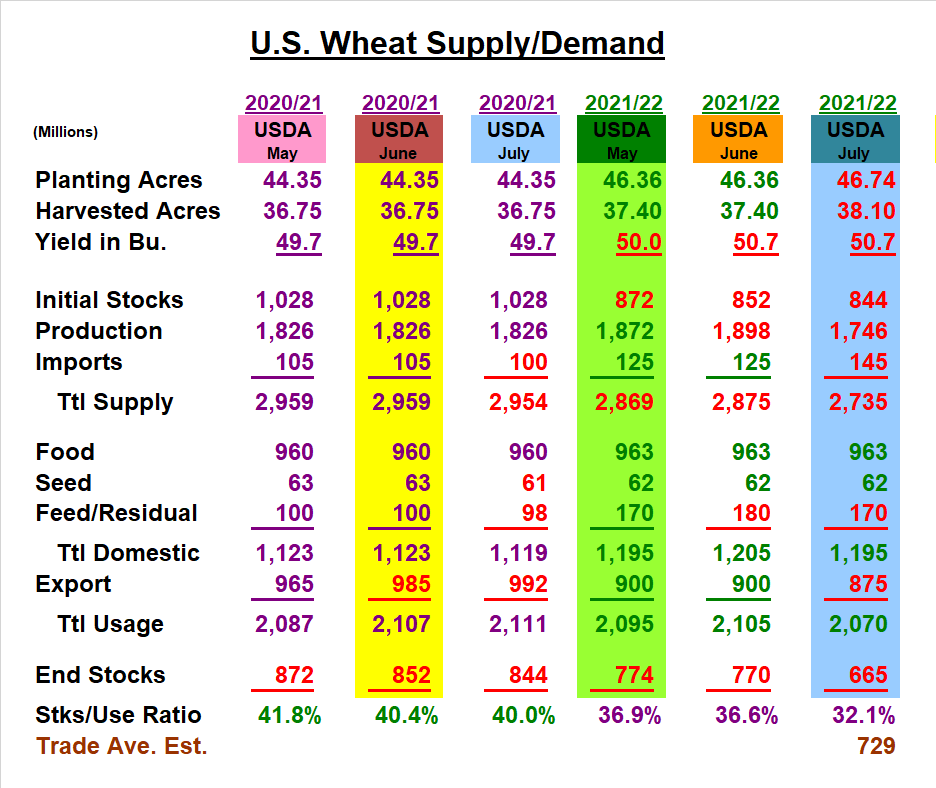

July’s US supply/demand revisions for corn & soybeans generally followed the trade’s expectations after June’s USDA acreage & stocks report. A sharp drop in US spring wheat output because this year’s N Plains drought dramatically changed wheat’s US balance sheet. Even with a larger US winter wheat crop, the USDA reduced the US crop to its lowest level since the 2017/18 season. This change also sliced wheat’s ending stocks & stocks/use ratio to their low- est levels in 7 seasons. These smaller US wheat supplies and reports of weather damaging Canada’s wheat, canola & feed grain crops helped firm prices across the CBOT.

This year’s extremely low spring wheat crop ratings prompted the USDA to drop this variety’s July yield by 18 bu to 30.7 bu, the lowest level since 2002. Despite this month’s 55 million bu rise in US W. wheat, 2021/22’s initial spring wheat projection of 345 million and durum’s 37 million bu crop (273 million bu less than 2020) reduced July’s US total wheat production to 1.746 billion bu. This 152 million smaller US crop reduced 2021’s US overall wheat yield to 45.8 bu, down 4.9 bu from last month. Despite a rise in US imports and slight reductions in feed & export demand by the USDA this month, wheat’s the US ending stocks are now projected at 665 million bu. their lowest level since 2013/14. Canada’s wheat crop was also cut by 4.5 mmt, but the USDA’s world output remains higher because of larger EU, Black Sea & Indian wheat crop in 2021/22.

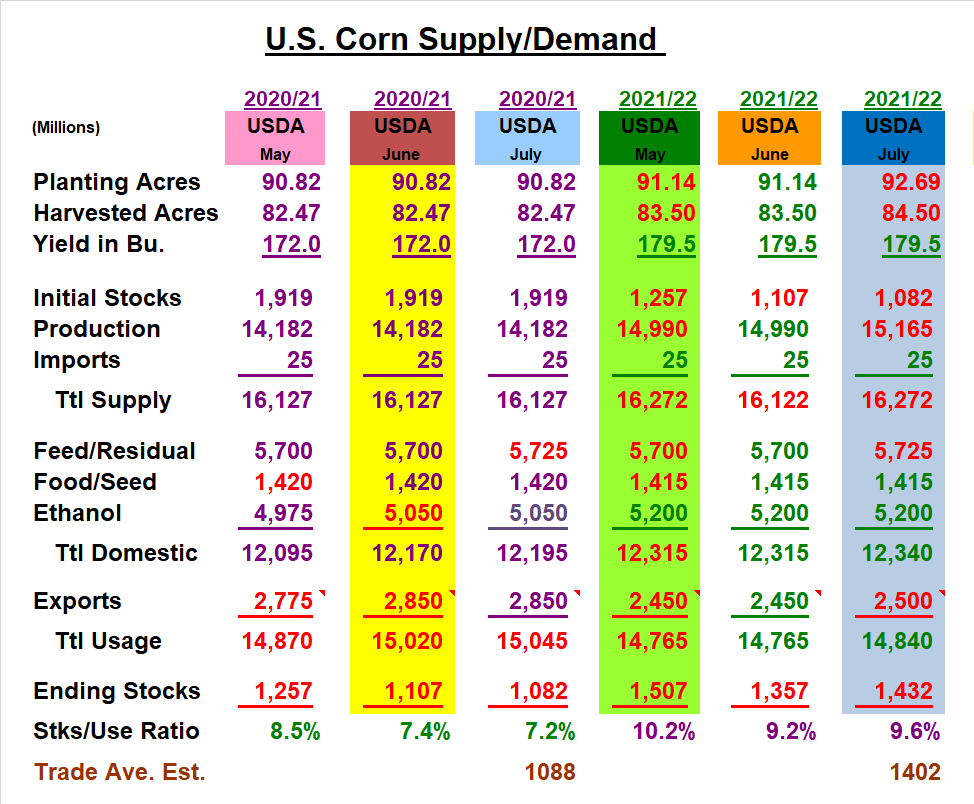

The USDA did up both corn’s old and new crop feed de- mand by 25 million and 2021/22’s exports by 50 million because of their lower Brazilian Safrinha corn crop estimate by 5.5 mmt to 93 mmt this month. However, no change in the US yield from their 179.5 bu new crop trendline level despite 20-25% of US corn crop in drought areas kept corn’s ending stocks 75 million bu higher than last month.

In soybeans, the USDA reduced old-crop imports, crushes, and exports leaving old-crop stocks unchanged. With no US 2021/22 yield change, soybean’s new crop supply/ demand levels & ending stocks were also left unchanged.

What’s Ahead:

Wheat’s US supply/demand data was impacted by the N. Plains drought this month. Growing conditions in the NW Midwest remain important as the US corn pollinates this month & soybeans set pods during August.

Harvested acres and US corn & soybean yields can be impacted by the sizable drought area that remains. Use $14.40-14.60 August prices to sell old-crop beans but hold all new-crop sales 20-25%.

Comments

Log in or sign up to join the conversation.