Image Source: Pexels

The US economy added 236,000 jobs in March with the unemployment rate dropping to 3.5%. With next week's core inflation number likely to come in at 0.4% month-on-month the odds must favor a final 25bp Fed rate hike in May. However, economic challenges are mounting with higher borrowing costs and reduced credit flow heightening the chances of a hard landing.

More jobs, less unemployment, and high inflation point to a 25bp hike in May

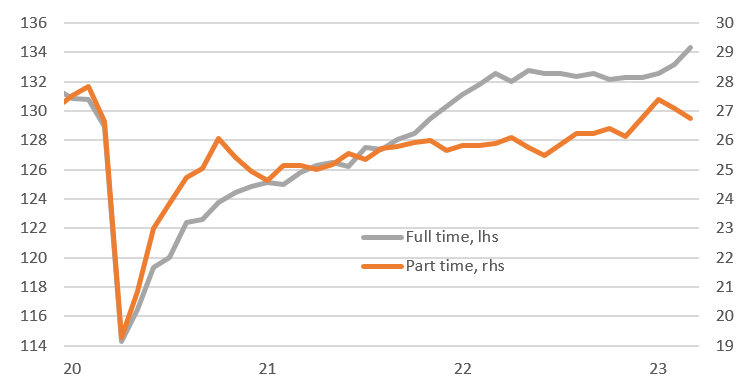

US non-farm payrolls rose 236k in March, above the 230k consensus. There were 17k of downward revisions to the past two months of data while the increase in private sector payrolls was weaker than hoped, rising 189k versus expectations of a 218k increase. The details offer a mixed picture though. On the positive side, the bulk of the jobs added were in full-time positions.

Full-time versus part-time employment (millions)

Image Source: Macrobond, ING

Up until last month all of the jobs added (on balance) over the previous 11 months were part-time with full-time employment having flatlined. Nonetheless, the job-creating sectors remain government (+47k), and leisure/hospitality (+72k) while private education/health continues its strong performance with a gain of 65k. On the negative side, construction, manufacturing, financial, retail trade, and temporary help all lost jobs.

Wages rose 0.3% MoM as expected, while the unemployment rate edged lower to 3.5%. As such the tight jobs market and decent job creation nudge up the probability of a 25bp rate hike on 3 May. Next Wednesday's CPI report is expected to show core CPI rising 0.4% MoM, more than double the 0.17% MoM rate needed overtime to take the US back to 2% YoY inflation. If that happens it is difficult to see the Fed pausing in May barring the re-emergence of financial system stress.

Banking stresses intensify the headwinds

Nonetheless, employment data is a lagging indicator – the last data point to turn in a cycle – and the outlook is becoming increasingly challenging. The economy has experienced the most aggressive period of monetary policy tightening for 40 years while recent banking stresses are likely to disrupt the flow of credit to the economy. Add in the fact that business confidence (be it the Conference Board measure of CEO confidence or the National Federation of Independent Business' small business optimism index) is at recessionary levels and the housing market is in deep trouble and this is a toxic combination for job creation.

Tighter lending conditions signal a big rise in unemployment in the second half of 2023

Image Source: Macrobond, ING

Indeed, even before the events at Silicon Valley Bank, the January Federal Reserve Senior Loan Officer survey had shown banks were becoming more cautious with credit flow likely to be restricted. This will inevitably get worse, putting struggling companies and households under intensifying pressures. The chart above suggests we should be braced for unemployment to rise from the late second quarter/early third onwards.

Rising lay-offs and jobless claims are other warning sign

This prognosis is also supported by the latest job lay-off and the revisions to initial claims data. There is always a delay between the announcement of layoffs and the actual job losses happening that result in an unemployment benefits claim. In addition, several states require all severance payments to have been finalized before a benefit claim can be lodged, which further extends the time frame. On top of that, not everyone will immediately lodge a claim. The chart below suggests a big rise in initial jobless claims is coming imminently and this will translate into a rising unemployment rate, as already indicated by the Fed’s Senior Loan Officer survey.

Surging lay-offs point to more pain to come (YoY% change)

Image Source: Macrobond, ING

Fed will reverse course as hard landing depresses inflation faster

We are obviously worried about the outlook for the US jobs numbers, but the commentary from Fed officials indicates that they feel they have more work to do to ensure inflation pressures are eradicated. Market pricing currently has it at a 55:45 call for the Fed to hike rates 25bp on 3 May.

We think the Fed will indeed hike 25bp, but see the Fed rapidly reversing course later this year. The combination of higher borrowing costs, disrupted credit flow, weak business confidence, and a crumbling housing market increase the chances of a hard landing for the economy, which will mean inflation pressures moderate more quickly. We see the potential for 50bp rate cuts at both the November and December FOMC meetings in such an environment.

More By This Author:

Belgium: Core Inflation Rises, But The Peak Is NearFollowing The Collapse Of Silicon Valley Bank, Where Do The Risks Lie For Small Banks?

Fx Daily: Is Gold Telling Us Something About The Dollar?

Comments

Log in or sign up to join the conversation.