The Stock Market Is Just Noticing What The Bond Market Has Known For Months

…that growth is slowing, the credit cycle could have already peaked and risk appetites are waning.

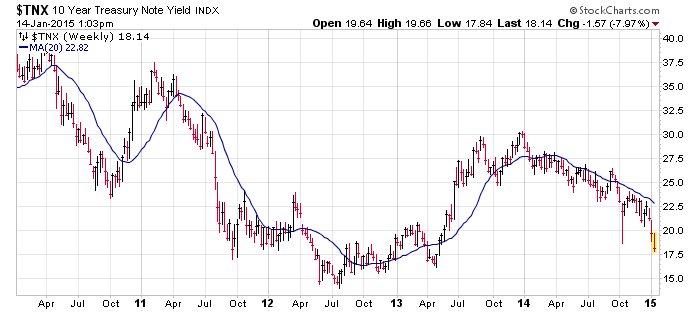

Over the summer I attended a conference which featured Steen Jakobsen as one of the speakers. The one thing he said that really stuck with me is that long-term bond yields lead the economy by about 9 months. If that is true, economists are going to be dramatically lowering their expectations for growth over the coming 9 months as the 10-year treasury has seen its yield plummet over the past year (not to mention foreign yields which are now negative at maturities of up to 5 years):

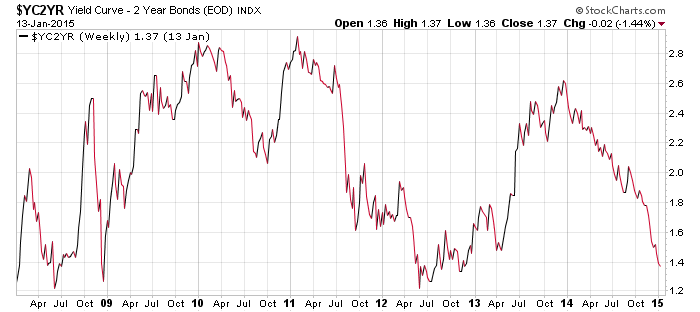

What’s more, the yield curve (the difference between the 10-year and the 2-year treasury yield) has flattened almost back to the level it saw at the very bottom of the financial crisis:

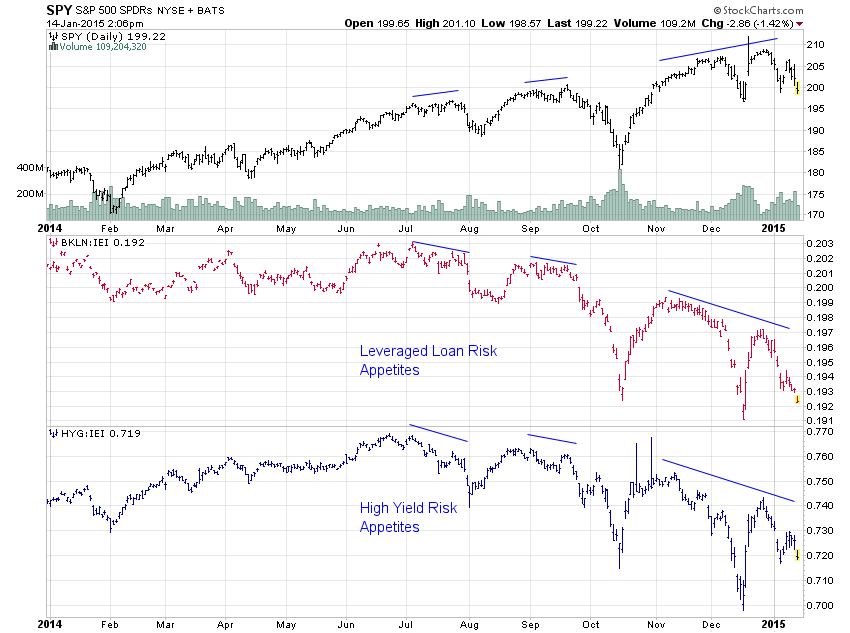

For most of 2014, stocks completely ignored this warning from the treasury market of slowing growth. One asset class that hasn’t ignored it is the corporate bond market, specifically the riskiest sector of the corporate bond market. High-yield bonds have been sending a clear signal for months now that, after a long hiatus, risk is making a comeback and the long-benign credit markets may be shifting to something not so benign. In his conference call yesterday, Jeff Gundlach called this divergence between stocks and high-yield, ‘the most worrying signal coming out of the markets right now.’

Most equity bulls have written off the weakness in junk bonds as a reaction to the oil crash which they believe will be contained. Junk has anywhere from 14-18% exposure to energy. However, leveraged loans have only a 4% exposure to energy and they have been just as weak, if not weaker, than junk bonds. This tells me that this growing risk aversion goes beyond just the energy sector and has implications for all risk assets, including stocks.

I guess nobody told the stock market as much until very recently. For the past few years risk appetites in the bond market (willingness to venture out on the risk curve from treasuries to riskier fixed income instruments) have been very highly correlated with stock prices – I’m talking 98% correlated… until last summer, that is. Since then, virtually all other risk assets have declined while US stocks continued to make new highs.

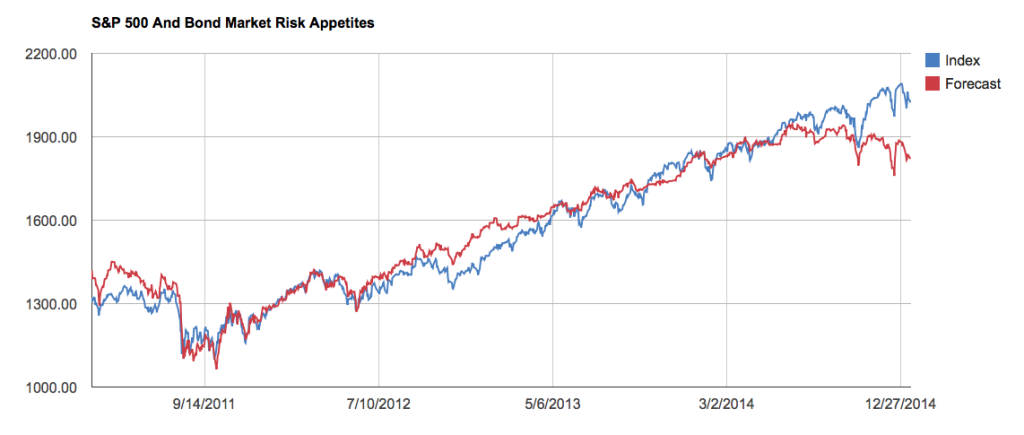

So to my mind the stock market weakness over the past couple of weeks is merely a function of equities playing catch up with all other risk assets. Stocks are just starting to pay attention to these messages of slowing growth, increasing risk and waning appetites.

In the short term, my model suggests the S&P 500 should be trading closer to 1800 than 2000, based solely on bond market risk appetites which, as I said, have been very highly correlated in the past. Having said that, bond market risk appetites are a moving target. They could recover and that would change this forecast. But should we be witnessing a cyclical end to the incredible hunger for risk assets we’ve seen over the past few years (inspired by ZIRP and QE) then I imagine this is only the beginning of the process. Yield spreads certainly have plenty of room to move wider still. We’ll just have to keep our eyes peeled, I guess. And keep them trained on the bond market which will likely tell the tale.

Disclosure: Information in “The Felder Report” (TFR), including all the information on the Felder Report website, comes from independent ...

more

Nice read. Thanks for sharing - I'm bullish on bonds.

Well written article here. I agree with your views except for one wild card -- Europe, which if they engage the "eurobond" will change this forecast dramatically, but again, well done, good to see people who actually understand what is really going on!