The Myth Of “Average Rate Of Return”

We are told that stocks are the way to wealth and that the market has averaged (pick a figure) over the last (pick a time frame) and so it will continue to do the same. It is important for you to understand that “average rates of return” can be easily manipulated and that whatever figure you get from Wall Street does not mean that your money will average that growth rate. (Dow Jones Industrial Average Stock Market Historical Graph)

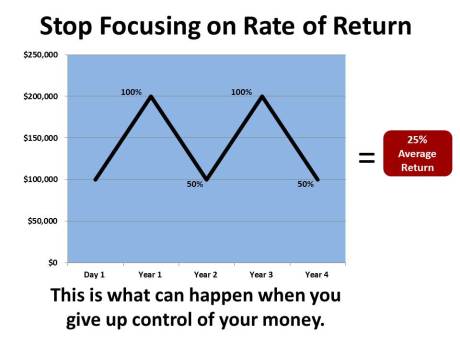

Remember this example well: over 4 years, how is it possible to invest $100,000 on year one and average a 25% rate of return for four years and have less than $100,000 after year four and have never taken a dime out of the account during that time? The answer is so easy once you understand how this works. Invest $100,000 into the account and it grows at 100% (doubles) in year one so now it is worth $200,000. Year two, the account falls by 50% (half) putting the value back down at $100,000. Year three, the account grows by another 100% and the money is back up to $200,000. Year four, the account dips back down another 50% and our money is now back to $100,000. Now you take out taxes you made on the good years (the way mutual fund taxes work is you can owe tax even though you have not sold the asset) and fees, and time value of money and your account is worth quite a bit less than the $100,000 you started your investment plan out with four years before.

Now take a look at your “average rate of return” and you will notice that if you add up 100% return years twice and subtract out your 50% years twice, that leaves you with 100%. You must divide that by the 4-year cycle and what do you get? Of course, I am a high school failure and college dropout but it looks like a 25% “average rate of return.” Did your money grow by 25% a year? Not hardly! If your money would have grown at 25% a year compounded annually your $100,000 would now be over $269,000. This is a far cry from the $80,000 your probably have left in your account when you “averaged” 25% per year for four years. Most of your 401k’s are earning an average rate of return.

Be very careful to focus on growth, not rates of return. If I am selling some kind of financial product and don’t like the last 4 year average I might try to show you the 8 year average. If that still stinks maybe the 15 year average will work? I have seen people in this day and age pull out 100 year averages to attempt to prove their point. The only problem is the economy of today doesn’t even vaguely resemble the economy of last century. This means that a 100 year average is probably a lousy way to try and predict the growth for the next 10 or 20 years of any particular product.

Instead of average rate of return focus on cash flow in and cash flow out of your accounts. Don’t get sucked into the age-old trap of just thinking about rates of return. Many times they are put in place so you will take your eye off the ball of what’s really happening. What’s really happening is that while we are all focusing on rates of return and the rise and fall of the stock market, we are happily pouring our wealth out month after month to the banks and other places with no real plan to stop the insanity. Wealth without Stocks will give you that plan.

Disclosure: none.