The Hawks Are Circling - How To Protect Your Portfolio

No, this week’s Market Outlook is not about the Atlanta Hawks who are hoping to get into the NBA playoffs by focusing on what they can control (and hoping what they can’t control, will go their way).

We’re talking about financial hawks that grew in number this week, and the game these hawks are playing will affect not only their net worth, but your net worth as well.

Let’s hope they have the right game plan.

Last week the stock market’s multi-week rally was rudely interrupted when a historically dovish Federal Reserve Board Governor, Lael Brainard, let the markets know that she’s moved to a more hawkish belief (see her confession below).

In reaction to this news, bonds (understandably) tanked across the whole curve, and the stock market’s sectors reacted with mixed results. Defensive sectors rallied and economically sensitive sectors fell leaving the indexes weaker but not broken.

The heart of the issue is that the economy is a hot mess. It’s experiencing both supply and demand shocks created by a pandemic and a war In Ukraine impacting economic growth and inflations around the world.

Consumer prices (especially food products) are rising at an alarming rate. This, along with a sharp rise in gasoline prices, are punishing the average American. See table below and the last several weeks of Market Outlook for the data on the punishing inflation conditions.

It’s inflation data like the table above that has continued to convert the “transitory” belief among officials, and most recently, Lael Brainard, to an increasingly hawkish stance which she communicated in a recent speech as follows:

“Currently, inflation is much too high and is subject to upside risks…It is of paramount importance to get inflation down,”

To bring inflation down, the Fed will “continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting,”

“Given that the recovery has been considerably stronger and faster than in the previous cycle, I expect the balance sheet to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017–19,”

The Fed is “prepared to take stronger action if indicators of inflation and inflation expectations indicate that such action is warranted,” Brainard said.

In the past, Brainard had been one of the more dovish Governors. She is now joining other Fed Governors, such as James Bullard, who have been communicating the need for more aggressive Fed tightening. In fact, Bullard has been stating for months that the Fed borrowing rates need to be at 3.0% or higher in the near future to have any chance to fight the out-of-control inflation. In March, when the Fed raised rates by 0.25%, Jerome Powell indicated that they anticipated raising an additional 8 or 9 times to get the Fed Funds rate to 1.9% by the end of 2022.

Lael Brainard’s new HAWKish view suggests that Fed borrowing rates should go up much faster and be above 3.0% by year-end to have any real chance of bringing down inflation.

The market immediately interpreted these comments as “gospel” and short-term rates rose quickly. This sent the yield curve into its second inversion in 2022 whereby short-term rates (2-year Treasuries) are higher than longer term rates (10 year).

This inversion was construed by the market (and every financial commentary) that we are headed into a recession. See chart below.

Most hurt by the hawkish comments were tech/growth and small-cap stocks. These are areas of the market that have been at high multiples (P/Es) and are likely to be more hurt by a combination of a slowing economy and higher borrowing costs.

For this past week the QQQ was down 3.5% and IWM fell 4.6% for the week. The mega cap core stocks closed flat for the week (DIA), and the S&P 500 was down 1.0%.

While previous inverted yield curves have accurately forecasted an economic slowdown, they did not send the economy or the stock market into an immediate downward move. Past recessions did not occur for a long-time into the future (average 18 months or greater).

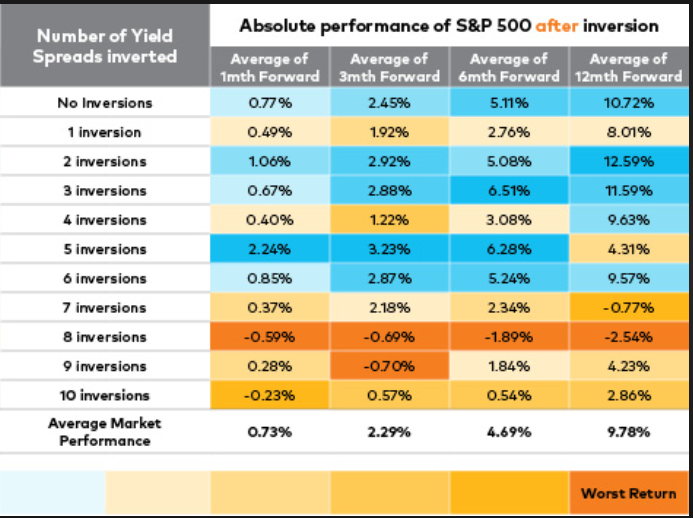

It’s important to consider the number and the duration of the inversions.

With regard to potential negative returns in the S&P500 over the periods of 1, 3, 6, and 12 months following a curve inversion, the chart below shows that on average, market returns have been positive in all time frames until the market has experienced 7 inversions.

April is typically a positive period for the stock market.

You may not be aware that April has historically been one the best months to invest in the stock market. This is only slightly muted in mid-term election years but remains positive. In fact, April has seen a positive return in 15 of the last 16 years.

We suggest you not get too caught up in the mainstream media and all the negative commentary.

Last Week’s Noteworthy Market Conditions:

Risk-On / Bullish

- Energy sectors continue to be strong.

- Value (VTV) segment rose and remains in a bullish phase. This balance a bearish week in growth stocks (VUG).

- The Dollar Index (UUP) broke out of a 4-week range to its highest level since early 2020.

- Biotech (IBB) continues to consolidate, and has a positive reading on our Triple Play Price and Volume indicators.

Risk-Off/Bearish

- Utilities (XLU) continue its strong move higher.

- Consumer Discretionary (XLY) was down 3% while Consumer Staples (XLP) was up almost 2%.

- Notable pattern in the sector rotation: The worst three groups for the week (SMH, IYT, XHB) suggest fears of economic weakness, while three of the four best performers are defensive (XLU, XLV, XLP) with the fourth being XLE which benefits from high oil prices.

- IWM broke its 50 DMA putting it back in a bearish phase.

- Market internals are in a neutral zone, but adv/decline metrics weakened, and the number of new lows confirmed the index’s weakness.

- Bonds, especially in the longer durations, got hit hard.

Neutral

- Risk Gauge moved from bullish to neutral

- The price action of the SPY, QQQ, and DIA has set up a range with support on the 50 DMA and prior swing highs from early March, and resistance near the 200 DMA and swing highs from February.

- VIX measures remained calm.

Disclaimer: Like to learn more about relative strength methodology? Our most recent free training material can be found more