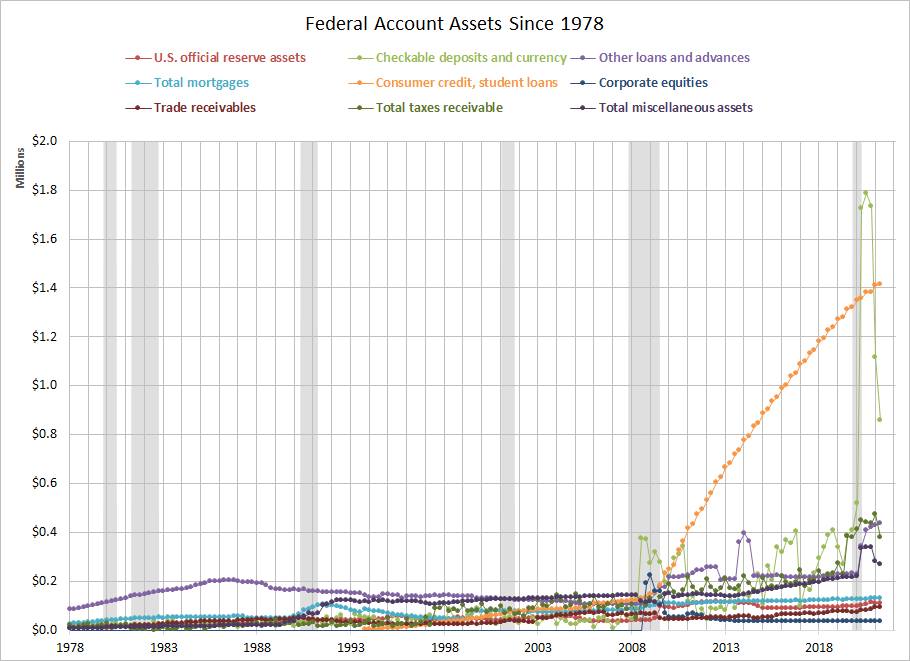

The Fed's Financial Accounts: What Are Uncle Sam's Largest Assets?

Note: We've updated the quiz based on this month's release of Q2 2021 Financial Accounts of the United States (previously referred to as the Flow of Funds Accounts).

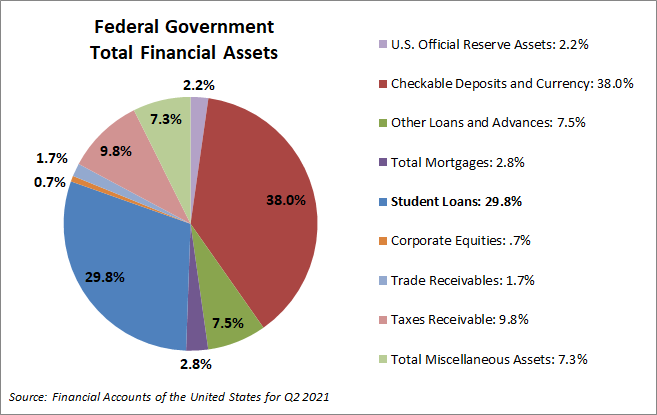

Pop Quiz! Without recourse to your text, your notes, or a Google search, which line item is the largest asset in Uncle Sam's financial accounts?

- A) Checkable Deposits and Currency

- B) Total Mortgages

- C) Taxes Receivable

- D) Student Loans

The correct answer, as of the latest quarterly data, is A) Checkable Deposits and Currency - but followed very closely by D) Student Loans! This is due to a decline in student loan balances because of CARES Act forbearances. Checkable Deposits and Currency has soared as a result of massive stimulus and reduced consumption from the COVID pandemic.

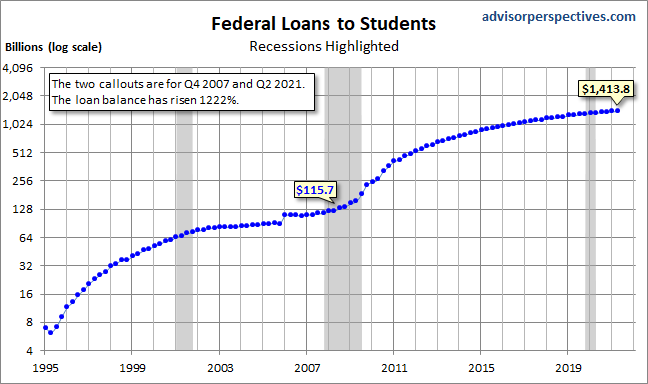

The rapid growth in student debt has been an ongoing topic in the financial press. A stunning chart that continues to haunt us illustrates the rapid growth in federal loans to students since the onset of the great recession. The chart is based on the Federal Reserve's Financial Accounts data (available here) for the government's assets and liabilities. We've used a log-scale vertical axis.

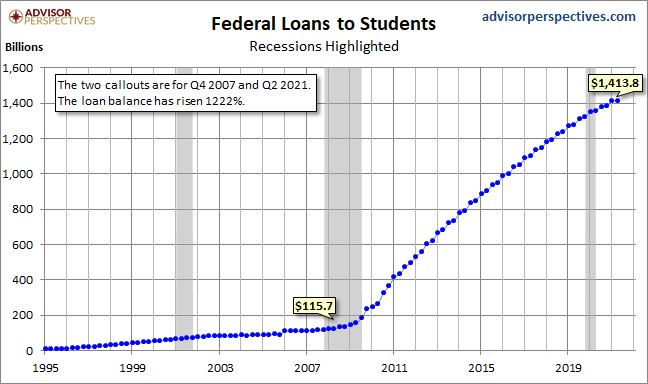

For a more dramatic look at the same data, here it is with a standard linear axis.

As we point out on the chart, the two callouts are for Q4 2007, the quarter in which the Great Recession began (December 2007), and the most recent quarter on record, Q2 2021. The loan balance has risen an astonishing 1,220 percent over that time frame, most of which dates from after the recession.

This chart only includes federal loans to students. Private loans increase the debt burden. The Federal Reserve Bank of New York regularly tracks household debt and credit. In their most recent update, they calculate student loan debt to be $1.57 trillion. However, "the share of student loans that are delinquent remains very low as the majority of outstanding federal student loans remain covered by CARES Act forbearances."

But back to our quiz. Student loans may be a liability on the consumer balance sheet, but they constitute an asset for Uncle Sam. Just how big? It's about 29.8 percent of the total Federal assets. This is about 11 times larger than the 2.8 percent for the Total Mortgages outstanding and 3.0 times the size of Taxes Receivable at 9.8 percent.

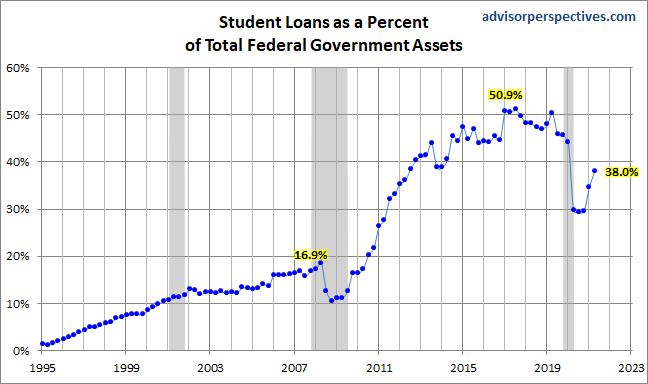

The 29.8 percent referenced is below its peak. Here is a look at how this metric has changed since 1995.

Here's a look at each of the assets over time from the pie chart above. You can see that Checkable Deposits and Currency spiked in 2020. The CARES Act has clearly had a massive impact on the money supply and the Fed's assets overall. Clearly, the Fed has injected money into the economy in order to maintain liquidity in the current recession, but the repercussions are yet to be seen.

Of course, assets are, sadly, the trivial side of Uncle Sam's Financial Accounts balance sheet — about 4 Trillion. The liability side totaled over 27 Trillion at the end of Q2 2021.

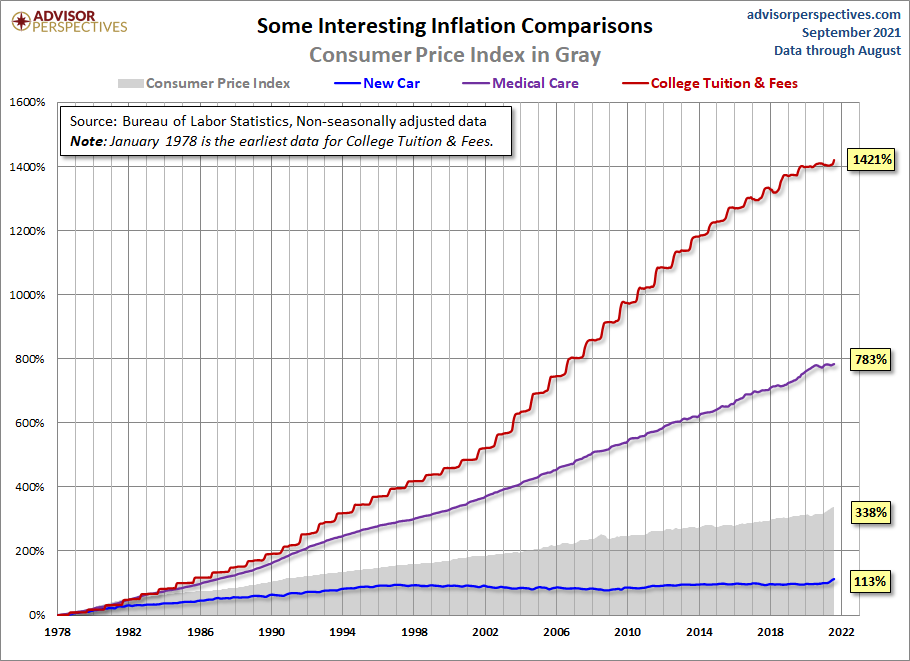

Here is a chart of data from the relevant Consumer Price Index sub-component reaching back to 1978, the earliest year Uncle Sam provides a breakout for College Tuition and Fees. As an interesting sidebar, we've thrown in the increase in the cost of purchasing a new car as well as the more substantial increase for the broader category of medical care, both of which pale in comparison.

During the decade of the 1990's, when real out-of-pocket funding declined 25%, tuition and fees rose 92%, which sounds substantial ... until you compare it to the 1421% across the complete data series. For early boomers, paying for college was sort of like buying a car. But in recent decades, it has become more like buying a house, for which the strategy of a minimum down payment is commonplace for first-time buyers.

The student loan bubble, the biggest slice in Uncle Sam's asset pie, will haunt us for many years to come.

Closing note: For a fascinating perspective on student debt repayment, see this article by a team of economists at the Federal Reserve Bank of New York.

Comments

No Thumbs up yet!

No Thumbs up yet!