“The Dominant Risk For Wall Street” May Be Manifesting In Small Caps

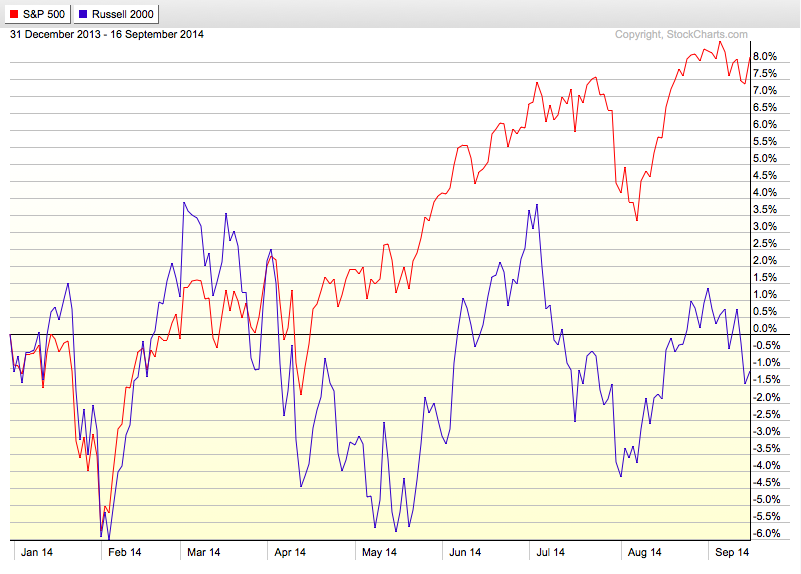

A good deal of attention has already been paid to the growing divergence between small cap and large cap stocks so far this year. The former have seen a small decline while the latter have risen about 8%. But I’ve seen very little commentary regarding WHY this might be happening. Of the many divergences the market has seen recently I think this one may be the most significant as the small caps could be the “canary in the coal mine” for the broader market.

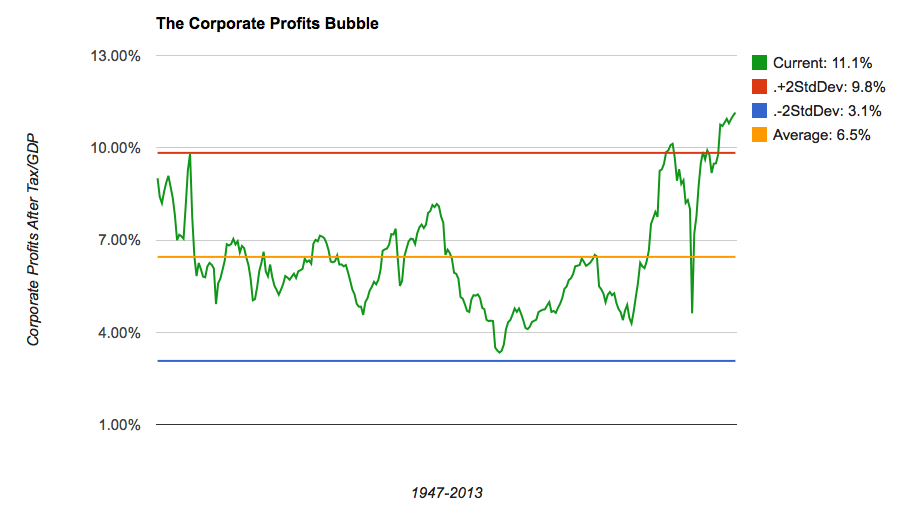

It all comes back to what I have argued amounts to a bubble in corporate profit margins. Jeremy Grantham has used a 2-standard deviation event as one benchmark for a bubble. Using that definition, it’s hard to argue that profit margins are not currently in a bubble.

Warren Buffett also weighed in on unsustainably high margins back in 1999:

In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems—and in my view a major reslicing of the pie just isn’t going to happen.

Note that margins are now nearly twice the 6% level that Buffett considered a long-term upper threshold. Now I haven’t heard him say anything about current levels of profit margins (and I’d love for somebody to ask!) but I think his logic is still valid. At some point, the pendulum will have to swing the other way and profits will revert to some extent.

Like the price divergence between small and large caps, the forces behind the scenes here have also been the subject of much ink. It’s that 99% versus the 1% thing. You see over the past few years as the economy has slowly recovered in the wake of the financial crisis companies have seen their revenues grow but have been reluctant to add to their employee base. The result is that a larger and larger portion of these revenues fall to the bottom line. This goes on for a period of five years and, voila! Record profit margins. The 1% (owners of these companies) celebrate while the 99% stagnate.

Until now…

There are signs recently that this dynamic is shifting. After all, you can only milk your current employee base so much before they become overextended and your product or service suffers or you can’t meet the growing demand, etc. At some point in the recovery or expansion process you have to start adding employees AND paying your current employees a little better in order to retain them.

And it’s beginning to look like this is exactly what’s starting to happen. As the BLS reported a couple of weeks ago, job openings are improving pretty dramatically. July saw a 22% gain year-over-year. And as we learned today, real wage growth spiked in August by the largest amount in years.

This is fantastic news for the 99%. It looks like more jobs and better pay are finally on the way. And it’s exactly the result the FOMC, with their albeit super-blunt tools, have been trying so hard to create. As Pimco’s Paul McCulley writes:

But as Martin Luther King intoned long ago, the arc of the universe does bend toward justice. And as I wrote in July, I think it will do so with the Fed letting the recovery/expansion rip for a long time, fostering real wage gains for Main Street. This implies that the dominant risk for Wall Street is not bursting bubbles, but rather a long slow grind down in profit’s share of GDP/national income.

But do bubbles usually unwind in a “long slow grind down”? Maybe. But sometimes they burst. Either way, this is not so good for the 1% and those record-high profit margins. And we’re seeing this happen already in what area of the market? You guessed it – the small caps and “middle market” companies. Sober Look reports:

While over 50% of [middle market] companies are seeing revenue growth, the fact that over 50% are experiencing EBITDA declines suggests margin compression. For the sixth consecutive quarter, more middle market companies experienced EBITDA declines than gains.

It’s been six consecutive quarters now that these smaller companies have experienced, “margin compression.” Make no mistake, this epic stock market rally has been built on the back of this profits boom. It’s been the source of much of the earnings growth we’ve seen and inspired investors to bid valuations to what has historically been rarified air. Should profits decline it would mean already extended valuations are even more inflated than they currently appear and would remove a major underpinning of the bull market.

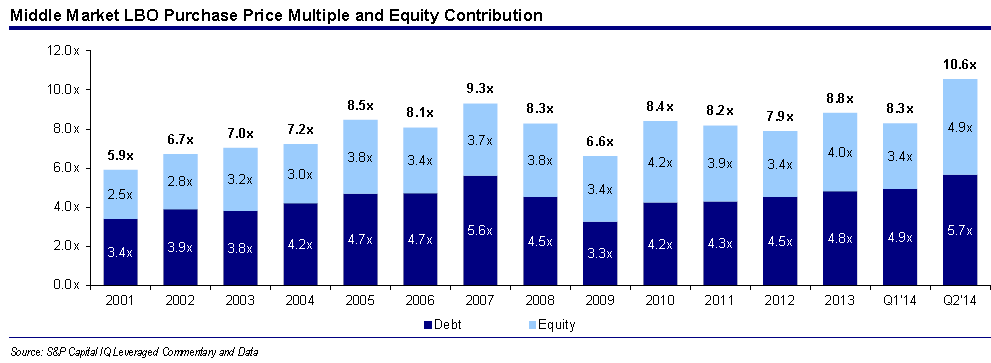

What I worry about even more, however, is the amount of risk that has been assumed recently based upon the expectation that profit margins will remain at these record levels indefinitely. As Sober Look recently reported, leveraged buy out valuations are at heights not seen at any other time during the past 14 years. More importantly the amount of debt in relation to targets’ EBITDA is also at a record:

Chart via Sober Look

If EBITDA at more than half of these companies is actually declining now these multiples will soon look even more inflated than they already do and the massive amount of debt used in buying them is at risk even greater risk of becoming unsustainable than it originally appears.

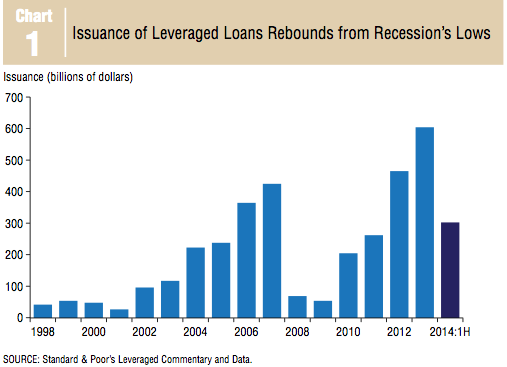

Speaking of the “massive amount of debt,” It’s important to note that the volume of leveraged loans has far surpassed it’s highs of 2007…

Chart via Dallas Fed

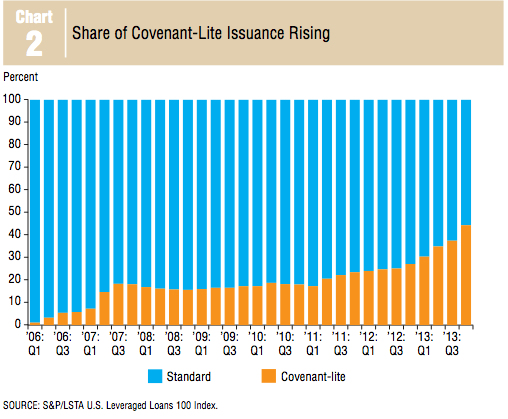

…and the risk controls embedded in these loans has fallen dramatically as covenant-lite’s share of overall issuance is now twice what it was prior to the financial crisis.

Chart via Dallas Fed

So it looks as if we may have more built up risk on the debt side of things than we did prior to the financial crisis. If margins are actually beginning to revert, as the small cap/middle market is suggesting, at 2-standard deviations above their long-term average, they potentially have a very long way to fall. And with so much risk betting against this possibility the fallout could be dramatic.

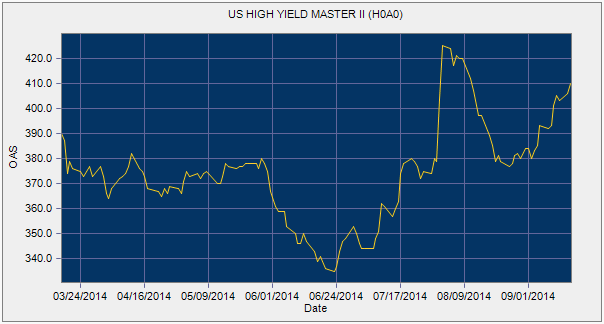

Perhaps this is why spreads have finally begun to widen just a bit over the past few months in the high-yield market.

Chart via Charlie Bilello

This is clearly a very complex system with various intermarket relationships. But we are seeing some signals that point to the fact that the Fed may be close to achieving its goals of increasing employment and wages. While this is good news for the labor force, it’s bad news for companies and investors because the resulting margin compression would remove the main driving force of this bull market along with causing potential problems (defaults) in the high-yield bond market. So keep your eyes on the small caps; there are big implications in that divergence everyone’s looking at.

Disclosure: Information in “The Felder Report” (TFR), including all the information on this website, comes from independent sources believed reliable but accuracy is not guaranteed and ...

more