The Albatross Of Debt: The Stock Market's $67 Trillion Nightmare, Part 4

<< Read More: The Albatross Of Debt: The Stock Market's $67 Trillion Nightmare, Part 3

<< Read More: The Albatross Of Debt: The Stock Market's $67 Trillion Nightmare, Part 2

<< Read More: The Albatross Of Debt: The Stock Market's $67 Trillion Nightmare

The Donald seems to think that the 37% gain in the stock market between election day and the January 26th high was all about him, and in one sense that's true.

Donald Trump is all about delusional and so are the casino punters. They keep buying what the robo-machines are buying, which, in turn, persist in feasting on the dip because it's there and because it's worked like a charm for nine years running.

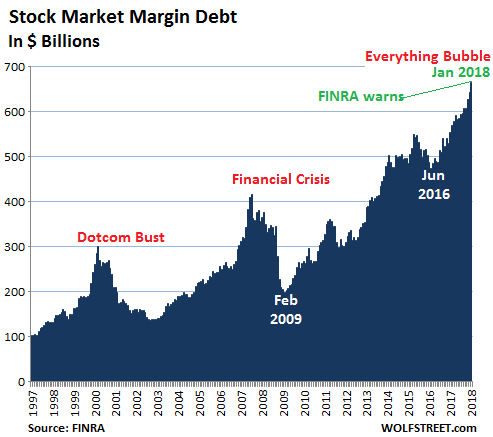

So doing, the punters have become downright reckless. After all, the market was already sky high last January----trading at 23X earnings on the S&P 500 and resting precariously on a record $554 billion of margin debt . Yet in order to load up on even more of these ultra risky shares, punters have since added $112 billion to their already staggering margin accounts, thereby helping to propel the S&P index to a truly ludicrous 27X by the end of January 2o18.

And therein lies the true danger of the Fed's 30-year long regime of Bubble Finance and the $67 trillion of debt it has piled upon the US economy. To wit, it has completely unmoored Wall Street from the main street economy, meaning that the speculative momentum and internals of the casino are operating in free flight: They will just keep levitating financial asset prices higher until some powerful shock triggers another meltdown of the type experienced during 2008, 2000 and 1987.

We happen to believe strongly that a bond market "yield shock" will be the crash-trigger this time around and for a self-evident reason. The central banks of the world have unleashed a credit monster----$67 trillion in the US, $40 trillion or more in China and $230 trillion on a global basis---and know they must finally stop the relentless monetization of existing debt and other assets.

The leadership for that task falls to the new Fed Chairman, Jerome Powell, who is a dyed-in-the-wool Keynesian and lifetime crony capitalist bubble rider. Indeed, during the 45 meetings during which he served as a member of the Bernanke-Yellen Fed, he did not dissent a single time.

So he now owns the epic bubble generated by that madcap regime of massive money printing and drastic interest rate repression, but through his Keynesian beer goggles Powell is thoroughly clueless about the resulting giant disconnect between main street and Wall Street.

Accordingly, he seems to think that there is a strong full-employment economy on main street, when it nothing of the kind; and a reformed, prudently regulated banking system at the center of Wall Street, when in fact it's teeming with the fruits of relentless speculation----FANGS, leveraged ETFs, options gambling, risk parity trades, structured finance deals loaded with hidden risk and debt and countless more.`

In other words, the Fed's new chairman avers that there is smooth sailing ahead, even suggesting to Congress today that the US economy is blessed with considerable tailwinds---including exports and fiscal policy!

We will address that tommyrot below, but what's ahead is tumult, not smooth. That's because the disconnect between a flat-lining main street economy and Wall Street's bubble ridden financial house of cards is blatantly unstable and unsustainable. Indeed, this fraught condition, which Powell and his Keynesian posse fail to see, will soon give rise to a thundering upheaval triggered by the Fed's own action.

We speak, of course, of the planned normalization of rates with four increases during the coming year, and the automatic pilot drive toward an unprecedented $600 billion per year bond dumping campaign incepting in October.

And that's just the beginning: Powell implied today that the Fed's balance sheet would keep shrinking until it hits the $2.5 trillion range. That is to say, our clueless Keynesian central bankers are fixing to dump upwards of $2 trillion of existing securities on the debt markets.

Needless to say, the margin borrowers depicted in the upper reaches of the chart below most definitely do no see it coming, and do not realize that the pivoting Fed as no longer their friend.

In Part 3, we pretty much documented the disconnect: Namely, that since the pre-crisis peak 10-years ago in Q4 2007, the inflation adjusted S&P 500 index is up 58%, while the industrial economy has essentially gone nowhere.

To wit, consumer goods output is still down 5%, manufacturing output is down 2%, total industrial production including utilities is up by just 2% and business equipment output has crept forward by less than 3%. Even inflation-adjusted S&P 500 earnings are up by only 8% per share.

Nevertheless, the erroneous theory abides that the industrial sector is a relic of your grandfather's economy, and that production of energy, metals, forests, farms and factories are not all that important: Services will carry the day!

We tend to wonder, of course, as to where all the income to buyrising levels of food, fuel, consumer goods and capital equipment from abroad is supposed to come from, if it's not made here; and also how the growing ranks of workers at nail salons, Pilates studios and golf resorts are to be paid, if industrial sector value added and income is not growing apace.

In fact, not withstanding the addition of $15 trillion of new debt to the nation's public and private balance sheet since Q4 2007, which in the Keynesian method of economic reckoning did add modestly to measured spending and therefore GDP, the services sector simply didn't take up the slack.

The graph below measures everything---the industrial economy and the services sector including government---and it tells essentially the same flatlining story.

Indeed, you can't get a more comprehensive and reliable measure than real final sales (which removes the distortions caused by inventory stocking and destocking cycles and inflation). Yet real final sales have expanded by only 15.2% since the Q4 2007 peak. That's just 0.6% per annum, and that a "recovery" does not make---at least by any historic standard.

Thus, during the peak-to-peak cycle of the Reagan/Bush era (Q2 1981 to Q2 1990) real final sales grew by 3.5% per annum, and during the 1990s cycle by 3.3% per annum. Since then, however, all the money pumping in the world---from the Fed's $500 billion balance sheet in 2000 to the $4.5 trillion recent peak---has not moved the US economy forward at more than a snails pace.

To wit, the peak-to-peak growth rate of real final sales during the phony Greenspan housing boom was just 2.5% per annum; and during the 10-years since the Q4 2007 peak, it has slowed to just 1.4% per annum. Indeed, if you throw in some Kentucky windage for the government's understatement of inflation, you basically have a flatlining 1% economy on main street and a soaring bubble economy for the 1% on Wall Street.

Likewise, the true facts of the labor economy tell the same story. Back in Q4 of 2007, the US nonfarm economy employed 237 billion labor hours at an annualized rate. Yet after ten years of Jobs Friday ballyhoo on bubble vision, the figure for Q4 2017 came in at 251.7 billion labor hours or just 6.2%higher.

That's right. Notwithstanding a cornucopia of low-paying, part-time jobs in hotels, restaurants, ball parks, retail stores, temp agencies, nursing homes, day care centers etc, total labor hours utilized by the US economy have grown at just 0.6% per annum over the last decade.

Yes, like everything else, total labor hours took a big hit during the Great Recession. Total hours employed dropped by more than 7%, but the failure to rebound in the historic manner is precisely why the current so-called recovery is so very different.

During the 1980s cycle, for instance, labor hours dropped by 3% from the Q2 1981 peak to the Q4 1982 bottom, but then rebounded smartly from there. For the cycle as a whole, which ended nine-years later in Q2 1990, total labor hours expanded by 2.0% per annum, notwithstanding the big dip in 1981-1982.

Likewise, the peak-to-peak growth rate of total labor hours during the 1990s cycle---the longest in history---was 1.8% per year.

After that however, the job-generating facility of the US economy headed straight south. The growth rate for both cycles since the year 2000 has been just 0.6% per annum.

(Click on image to enlarge)

Needless to say, the punk growth of labor hours during the current so-called recovery has not been made up by a surge of productivity, either, or some kind of early arrival of the vaunted robot age. In fact, labor productivity growth during the current cycle has been barely half of that recorded during the previous three business expansions.

Thus, during the 10 years since the Q4 2007 peak, the labor productivity index has risen by just 12%----again a far cry from the 58% gain in real stock prices over the period.

On an annualized basis, that amounted to just 1.1%. And during the seven years since Q4 2010 after the post-recession economy stabilized, the productivity growth rate has skidded to just 0.7% per annum.

The trend over the last seven years, especially, is simply off the historical charts----meaning that it's not a real recovery in any meaningful since of the word. For instance, during the 9-year Reagan-Bush cycle, labor productivity grew at 1.7% per annum, and then accelerated to 2.0% annually during the 1990s cycle and to 2.8% per annum over 2001-2007.

Indeed, in the great sweep of history, the labor productivity figures scream out that a huge disconnect has occurred during the present period. To wit, between 1953 and 2010, labor productivity grew at 2.2% per annum, with all the interim booms and busts averaged-in.

That's more than 3X the paltry 0.7% annual gain since Q4 2010.

(Click on image to enlarge)

The fact that almost any main street metric shows a gain of 2-15% over the last decade in real terms compared to the 58% surge in inflation-adjusted stock prices, of course, is completely lost on Powell and his posse of central bankers, as well as the sell-side stock peddlers on Wall Street.

And that's because in a market obsessed with stock prices it's all about the delta. That is, the latest noise- and revision-ridden rate of change from prior period that may give an "edge" to some headline reading robo-machine or adept carbon-based speculator.

In that context, the Fed heads claim to have only a passing interest in stock prices, but that's one of the Great Lies of modern times; they are absolutely obsessed with the stock averages, and therefore have essentially spun themselves into functional economic illiteracy.

In his presentation on Capitol Hill today, for instance, Powell pointed to the export pick-up as evidence that the US economy has continued to strengthen.

Really?

Goods and services exports in Q4 2017 posted at a $2.419 trillion annual rate. If you squint at the chart below, you can see that this figure is virtually the same as the $2.374 trillion rate posted three years ago in Q4 2014. Accordingly, the only thing that stands behind Powell's purported "export tailwind" is the good old "pig-in-the python" of the China-driven industrial/commodity/global trade mini-cycle, which has now essentially gotten back to "go".

But do not collect $200!

Over the weekend, Beijing essentially declared Mr. Xi ruler for life, nationalized without warning the massive $300 billion M&A junk pile called Anbang, and published data showing housing prices in the Tier 1 cities are now falling again on a year over year basis.

We do not think these actions bespeak boom times ahead for the Red Ponzi or that the debt and speculation ridden "locomotive" ofthe ballyhooed outbreak of "synchronized global growth" will prove up to the task. To the contrary, the pre-19th Party Congress credit binge in China is over and done, meaning that Beijing intends to get down to the serious business of wrestling its $40 trillion credit monster to the ground.

In fact, throw in the Donald's impending 10% and 25% tariffs on aluminum and steel, respectively, and the future position of the red bars on the graph below will be lucky to even stay on the flatline.

(Click on image to enlarge)

Not only is the disconnect between main street and Wall Street vast and largely ignored in the Eccles Building, but so is the direction of causation. Powell and his recycled band of money printers are complacent because their recession-warnings dashboards are blinking neither red nor even orange on most metrics.

But so what?

In the world of Bubble Finance and central bank driven financial markets, recessions do not cause stock market corrections or crashes. Instead, meltdowns in the casino actually cause recessions because they trigger brutal and sweeping "restructuring" maneuvers in the stock options obsessed C-suitesof corporate America in desperate bids to appease the trading gods. Purportedly redundant workers, inventories, fixed assets and busted goodwill from failed M&A deals all get ash-canned in a frenzy of corporate actions, which then brings the main street economy to a screeching, but temporary halt.

As always, the issue is the catalyst for the crash in the late stages of central bank fostered financial bubbles. And this time it's truly not hard to see the great bond market "yield shock" coming down the pike. That is to say, when $1.8 trillion of supply---$1.2 trillion new debt from the US treasury and $600 billion of old debt to be dumped by the Fed---hits the bond pits in FY 2019, the markets will definitely clear or perhaps "clear-cut" is a better word.

To wit, the law of supply and demand not having been repealed, and the other two important central banks of the world---the ECB and the PBOC heading for the sidelines. Accordingly, the clearing yield is going to be in the 4% to 5% range, and in the historic context of the chart below, the implications are self-evident.

Chairman Powell today told the Congress, in effect, "steady as she goes".

That's not going to happen in a month of Sunday's, and in Part 5 we will take a crack at essaying the financial carnage that lays dead ahead.