The good news is:

- We may have seen the bottom of this cycle.

The Negatives

New lows peaked at 542 on the NYSE Friday January 28 and 1152 on the Nasdaq. Last Tuesday they fell to 48 on the NYSE and last Wednesday there were 114 new lows on the Nasdaq. We are not out of the bears den yet. Last Friday there were 265 new lows on the NYSE and 347 on the Nasdaq. These are scary numbers, but substantially lower than those of a week earlier.

The first chart covers the past 6 months showing the Nasdaq composite (OTC) in blue and a 40% trend (4 day EMA) of Nasdaq new highs divided by new highs + new lows (OTC HL Ratio), in red. Dashed vertical lines have been drawn on the 1st trading day of each month and dashed horizontal lines have been drawn at 10% levels for the indicator; the line is solid at the 50%, neutral level.

OTC HL Ratio rose from its low, but remained in seriously negative territory.

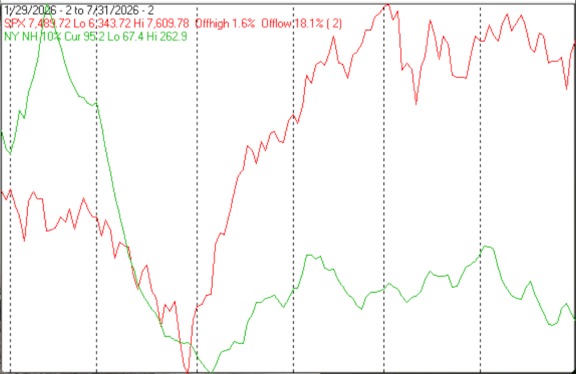

The next chart is similar to the first one except it shows the S&P 500 (SPX) in red and NY HL ratio, in blue, calculated with NYSE data.

The pattern of NY HL Ratio is similar to the previous chart.

The next chart covers the past 6 months showing the SPX in red and a 10% trend (19 day EMA) of NYSE new highs (NY NH) in green.

There is no life in NY NH, which remained near its lowest level in over a year.

The next chart is similar to the one above except it shows the OTC in blue and OTC NH, in green, calculated with Nasdaq data.

Ditto OTC NH.

The Positives

New lows declined significantly over the past week.

The next chart covers the past 6 months showing the OTC in blue and a 10% trend (19 day EMA) of Nasdaq new lows (OTC NL), in brown. OTC NL has been plotted on an inverted Y axis so decreasing numbers of new lows move the indicator upward (up is good).

OTC NL moved sharply upward last week.

The next chart is similar to the one above except it shows the SPX in red and NY NL has been calculated with NYSE data.

NY NL paused Friday and that is a little troublesome, but the direction for the week was a positive.

The new low indicators are the best bottom indicators I have.

Seasonality

Next week includes the 5 trading days prior to the 2nd Friday of February during the 2nd year of the Presidential Cycle. The tables below show the daily change, on a percentage basis, for that period.

OTC data covers the period from 1963 to 2020 while SPX data runs from 1953 to 2020. There are summaries for both the 2nd year of the Presidential Cycle and all years combined. Prior to 1953 the market traded 6 days a week so that data has been ignored.

Average returns for the coming week have been modest; a little weaker for the SPX than the OTC, but they are not calculated over the same periods.

Report for the week before the 2nd Friday of February. The number following the year is the position in the Presidential Cycle. Daily returns from Monday to 2nd Friday. OTC Presidential Year 2 (PY2) Year Mon Tue Wed Thur Fri Totals 1966-2 0.37% 0.18% -0.28% 0.84% -0.10% 1.01% 1970-2 1.46% 0.53% -0.19% 0.61% 0.60% 3.01% 1974-2 -1.34% -0.46% 0.30% 0.08% -0.66% -2.08% 1978-2 0.05% 0.47% 0.42% 0.02% 0.37% 1.32% 1982-2 -1.90% -1.15% 0.25% -0.39% 0.15% -3.04% 1986-2 0.64% 0.15% 0.39% 0.55% 0.58% 2.32% 1990-2 0.60% -0.17% 0.66% 0.12% 0.36% 1.56% 1994-2 0.25% 0.45% 0.49% -0.40% -0.26% 0.53% 1998-2 -0.24% 1.10% -0.02% 0.33% -0.23% 0.95% Avg -0.13% 0.08% 0.35% 0.04% 0.12% 0.46% 2002-2 -2.91% -0.92% -1.40% -1.69% 2.06% -4.86% 2006-2 -0.17% -0.61% 0.98% -0.49% 0.27% -0.02% 2010-2 -0.70% 1.17% -0.14% 1.38% 0.28% 1.98% 2014-2 0.54% 1.03% 0.24% 0.94% 0.08% 2.84% 2018-2 -3.76% 2.12% -0.89% -3.88% 1.43% -4.99% Avg -1.40% 0.56% -0.24% -0.75% 0.82% -1.01% OTC summary for PY2 1966 - 2018 Avg -0.51% 0.28% 0.06% -0.14% 0.35% 0.04% Win% 50% 64% 57% 64% 71% 64% OTC summary for all years 1963 - 2021 Avg -0.13% 0.03% 0.07% 0.18% 0.05% 0.20% Win% 40% 59% 56% 66% 62% 59% SPX PY2 Year Mon Tue Wed Thur Fri Totals 1954-2 -0.27% -0.23% -0.11% -0.31% 0.23% -0.69% 1958-2 -0.60% -0.89% -0.44% 0.02% 0.95% -0.95% 1962-2 0.10% 0.11% 0.66% 0.23% -0.14% 0.96% 1966-2 0.35% -0.04% 0.55% -0.24% -0.02% 0.59% 1970-2 0.79% -1.05% 0.98% -0.24% -0.22% 0.26% 1974-2 -2.13% -0.31% 0.28% 0.04% -1.04% -3.16% 1978-2 -0.13% 0.93% 0.55% -0.58% -0.24% 0.52% Avg -0.20% -0.07% 0.60% -0.16% -0.33% -0.17% 1982-2 -2.24% -0.83% 0.86% -0.20% -0.04% -2.45% 1986-2 0.78% -0.15% 0.02% 0.66% 1.09% 2.41% 1990-2 0.28% -0.66% 1.24% -0.24% 0.20% 0.82% 1994-2 0.42% -0.15% 0.36% -0.81% 0.27% 0.08% 1998-2 -0.18% 0.82% 0.10% 0.40% -0.39% 0.75% Avg -0.19% -0.19% 0.52% -0.04% 0.22% 0.32% 2002-2 -2.47% -0.40% -0.60% -0.31% 1.49% -2.30% 2006-2 0.08% -0.81% 0.87% -0.15% 0.25% 0.24% 2010-2 -0.89% 1.30% -0.22% 0.97% -0.27% 0.89% 2014-2 0.16% 1.11% -0.03% 0.58% 0.48% 2.30% 2018-2 -4.10% 1.74% -0.50% -3.75% 1.49% -5.11% Avg -1.44% 0.59% -0.10% -0.53% 0.69% -0.80% SPX summary for PY2 1954 - 2018 Avg -0.59% 0.03% 0.27% -0.23% 0.24% -0.28% Win% 47% 35% 65% 41% 53% 65% SPX summary for all years 1953 - 2021 Avg -0.27% -0.04% 0.11% -0.05% 0.09% -0.15% Win% 39% 52% 57% 44% 56% 58%

Conclusion

New lows declined from their extremes offering hope that their extremes indicated a cycle bottom. Next week should clarify that picture.

The strongest sectors last week were Energy (same as the week before) and Banks while the weakest were Transportation and Precious Metals (same as last week).

I expect the major averages to be higher on Friday, February 11 than they were on Friday, February 4.

Comments

Log in or sign up to join the conversation.