Wednesday, June 16, 2021 2:00 AM EDT

Industrial output is rising, but supply chain strains mean that manufacturers are struggling to keep pace with orders. In an environment of robust consumer demand, this is leading to more and more shortages and the risk of higher and higher prices.

Output rises, but it should have been better

US manufacturing output increased 0.9% in May versus the 0.8% consensus, but there were some hefty downward revisions with April now reported as having seen output grow 0.1% versus the 0.5% rate initially reported.

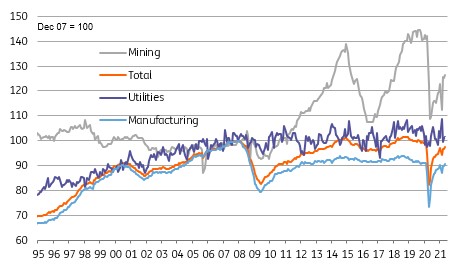

US industrial output levels December 2007 = 100

Source: Macrobond, ING

The details indicate manufacturing rose 0.9% month-on-month as autos rebounded 6.7% MoM from a period of weakness while utilities rose 0.2% and mining posted a 1.2% increase. This leaves manufacturing output 0.7% down on the pre-pandemic peak, having fallen 19.8% peak to trough from January to April last year. This is an encouraging story with all the lost output set to be fully recovered within the next couple of months. Nonetheless, the long term structural headwinds are underlined by the fact that output peaked in December 2007 – fast approaching 14 years ago.

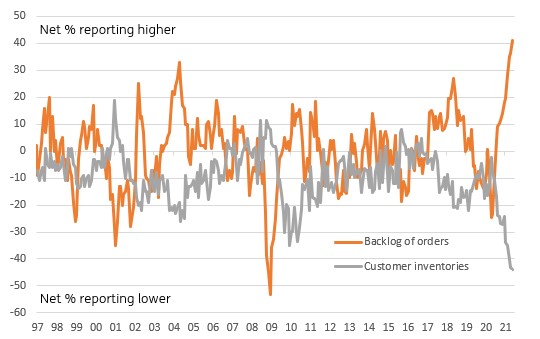

That said we remain upbeat on growth and job prospects for the sector this year since the Institute for Supply Management has reported that new orders continue to grow strongly, but supply chain issues appear to be holding back production. This is resulting in a record for order backlogs so there is plenty of opportunity for output growth and job creation.

ISM backlog of orders hits new highs while customer inventories are at record lows

Source: Macrobond, ING

Supply chain strains imply more inflation risks

Our bigger concern in the near-term is that the supply chain strains continue far longer. Manufacturers already suspect that their customers may be becoming more desperate with inventories at record lows, as indicated by the ISM time series in the chart above. In an environment of robust consumer demand ongoing shortages mean that prices can rise even more rapidly.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.

No Thumbs up yet!

No Thumbs up yet!