Image Source: Unsplash

So much for the idea of equity investors rooting for a stronger economy, at least for today. This morning’s reaction to the stronger-than-expected December jobs report revealed that stock traders are once again more concerned about the potential for monetary accommodation rather than the type of robust economy that can improve corporate fundamentals.

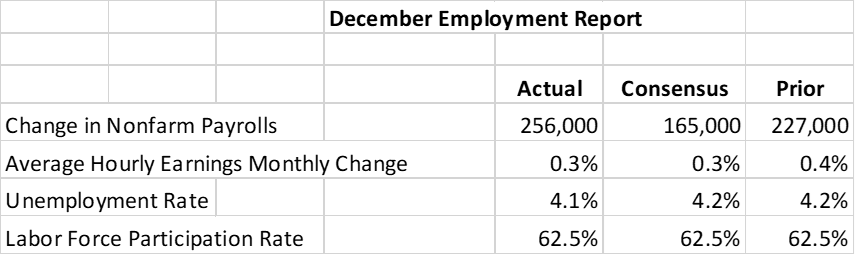

My initial comment immediately after seeing the numbers this morning was “Wow!”A set of key statistics that are so outside consensus will inspire that type of reaction.I happened to be on live TV at the time, and went on to say:

The problem here now is if you were looking for [interest] rate cuts based on a weakening labor market, this fits in with the Fed [Federal Reserve] rhetoric that we’ve heard. Stop looking for those. It’s not going to happen, at least in the immediate term… Unfortunately for stocks, the bond market doesn’t like that.

We can forget about the weaker labor narrative for a while, and that anyone basing hopes for a more accommodative Fed on the employment portion of the dual mandate need[s] to wait a while.

Remember, the Federal Reserve has a “dual mandate” to “foster economic conditions that achieve both stable prices and maximum sustainable employment”. One of the justifications for the 1% cuts in the Fed Funds target that we saw over the past three Fed meetings was a softening labor economy, one that was moving away from maximum sustainable employment.Today’s report pushed the data in the opposite direction.It is impossible, at least for now, to assert that these numbers reflect any sort of labor market weakness:

(Click on image to enlarge)

Sources: U.S. Bureau of Labor Statistics, Bloomberg

Combine the strong labor report with the comments made in the recently released minutes to the December FOMC meeting that showed members’ concerns about inflation risks and it becomes difficult to justify rate cuts – not when we are running closer to “maximum sustainable employment” while our ability to maintain “stable prices” is in question.Fixed income markets agree with that notion.The CME FedWatch now prices in only a single rate cut for 2025 no earlier than September, whereas yesterday two cuts beginning in June were expected.The IBKR Forecast Trader is broadly in line with that assessment, showing a 67% chance that rates will not be above 4.125% (a 25bp cut) in June while the CME is at 76%.

Having assessed the changing rate cut picture, we can only assume that it is driving the woeful stock market response.Indeed, bond yields are higher across the curve, though the curve is flatter.We have 2-year yields up 10bp to 4.37% while 10-years are up 6bp to 4.75%, which reflects the lower likelihood of near-term cuts.But the vast majority of stocks are lower, with decliners outpacing advancers by over 4:1.We do have stocks like Walmart (WMT) and Target (TGT) rising – people with jobs can buy things at stores – but the general malaise is the “tell”.A stronger economy should broadly help the earnings, dividend, and cash flow streams of a wide range of companies, but that clearly doesn’t matter right now.Don’t forget that at this time last year that we were expecting 7-8 cuts for 2024 yet the market rallied solidly even though we got only the equivalent of 4.The solid economy more than made up for that deficiency.

One final observation: volatility appears to be back.Assuming we close as weakly as we appear at midday, this would be the fourth week in a row with two S&P 500 closes of greater than +/- 1%.That would make 8 of the past 15 sessions with relatively sizeable moves – 5 up and 3 down. While some might interpret the current readings of VIX around 20 as showing fear, it more likely reflects the recent propensity of SPX to move more aggressively in recent weeks and concerns that the upcoming earnings season and potential policy moves by the incoming administration could result in outsized moves.Remember, volatility measures moves in both directions – up AND down – even if traders’ desire to pay to hedge that volatility tends to reflect concerns about the potential for downdrafts.

More By This Author:

Jensen Huang’s Quantum Splash Of Cold Water

Options Market Expectations For The Payrolls Report

Tariffs? No Biggie, As Long As Nvda Is Up

Comments

Log in or sign up to join the conversation.