Stock-Bond Ratio Rolling Over And Investors Aren't Prepared

-

Expect GDP growth forecasts to be slashed as extreme geopolitical turmoil and price shocks threaten the global economic rebound

-

Central Bankers are stuck between inflation and growth/stockmarket risks. Taming price increases will likely be their focus now that the US is at full employment.

-

Investors remain too heavily positioned in stocks relative to cash/bonds. We favor the latter group over the intermediate term given the unfolding risk backdrop.

Stagflation fears were largely balked at six months ago. Oh, how times have changed. Stubbornly hot inflation and imminent geopolitical risks have cast doubt on just how long growth can continue. These two trends suggest that the risk of a global economic recession has gone up significantly just in the last several weeks. Our flagship Weekly Macro Themes report investigates the real possibility of a drastic downturn in GDP growth as the year progresses.

Defensives Leading

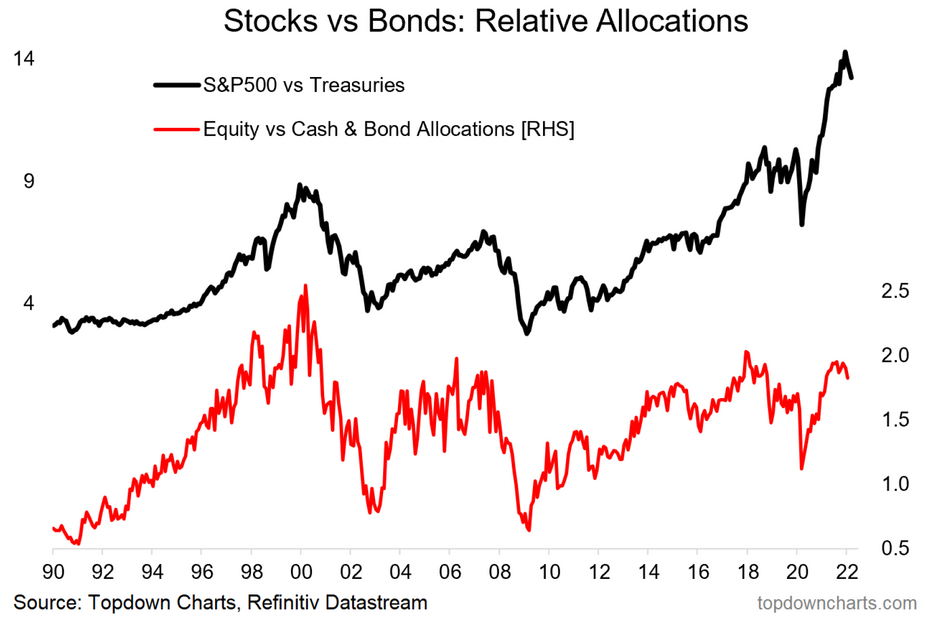

Investors have turned to defensive niches of the investable market despite this usually bullish time of the year. Consumer staples stocks, commodities (including gold), cash, and even bonds have seen money come in. Still, investors remain positioned somewhat aggressively into the broader stock market. Cash and bond allocations remain relatively light. Our featured chart illustrates how bold people are with their money even with elevated volatility in 2022.

Featured Chart: Investors Still Overweight Equities

(Click on image to enlarge)

Positioning Remains Too Bullish. That is a Bearish Sign.

Investors are saying one thing yet doing another. The latest NAAIM Exposure Index reading, which represents the average exposure to US equity markets reported by its members, fell to the poorest number in nearly two years. Typically, that can be seen as a bullish contrarian indicator, but if we do not see allocations line up, it’s less useful.

We saw a similar juxtaposition with respect to feelings on inflation and consumer spending—people report being furious about rising prices, yet they are spending as if times have never been better. Look at what people do with their money, and put less weight on how they feel.

Decades-High Inflation – Even Before Commodities Best Week On Record

Turning back to our weekly report, we find downside growth risks escalating. And this has really started to come to a head considering commodities just had their best week ever, according to S&P data on FactSet. And now everybody knows about it. Energy prices are up huge. Even non-investors see the surge at corner gas station price signs.

Moreover, coal, natural gas, agricultural, and base metals are all soaring. That will certainly eat into corporate profits and exacerbate inflationary pressures. Stagflation is on the table. The silver lining is perhaps these macro headwinds calm down by the second half if cooler geopolitical heads prevail.

Bonds Over Stocks

We reiterate our stance and raise our conviction that stocks underperform bonds in the months ahead. The US is most susceptible to downside equity price risk given the massive run-up it saw last year versus the rest of the world. Recent price action indicates a rolling over of that previously bullish trend. And the data confirms this outlook—our report investigates Leading Economic Indicators (LEI) and its relationship with future stock market price action.

Bottom Line: We expect to see downside equity trends versus bonds in the intermediate term. Slower growth, maybe even negative in some regions, along with central banks stuck between recession risks and massive inflation creates too many headwinds for risk assets. The kicker is that investors are just not positioned defensively enough yet.