The economically-sensitive Russell 2000 stock index (IWM) has given back all of its early 2023 rebound and is now negative year to date, -29% from its cycle peak in October 2021 and just 1% higher than where it was in August 2018.

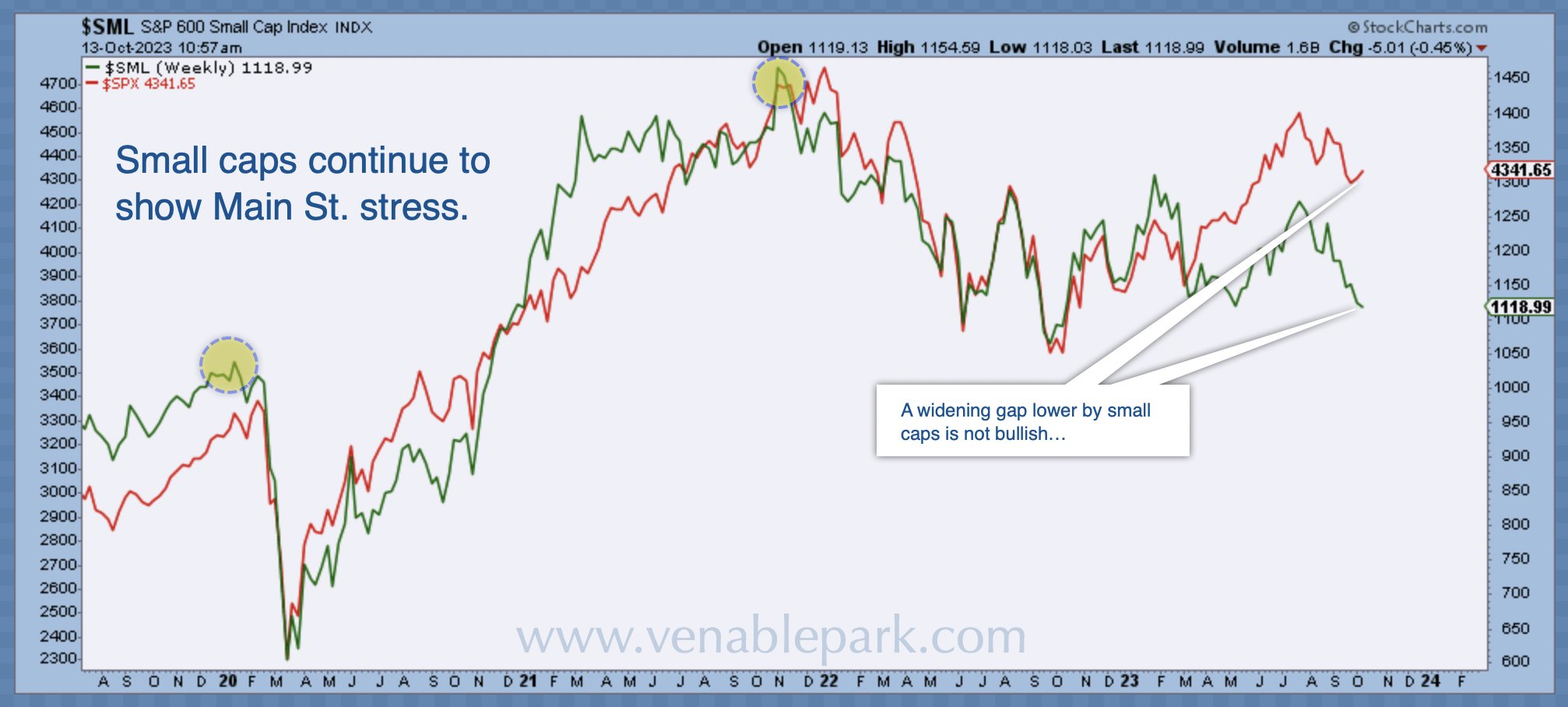

The more concentrated US small-cap 600 index (SML in green below since April 2019, courtesy of my partner Cory Venable) is 20% lower than its November 1, 2021 cycle peak and 2.8% higher than five years ago. Small-cap indices typically lead the economy and the large-cap S&P 500 index (below in red).

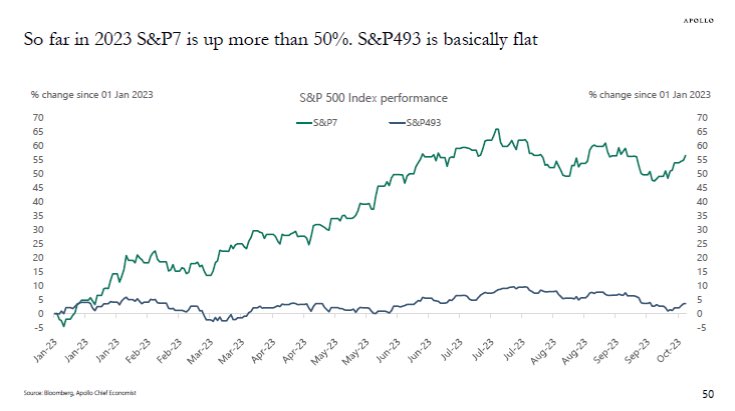

Under the surface, 98% of S&P 500 stocks are indeed following the small-cap lead. Four hundred and ninety-three (black line below, courtesy of Apollo Global Management) are flat year to date. Just the seven most expensive companies (Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla and Meta Platforms) have rebounded to lower highs (green line below).

It has been wisely observed that markets are most vulnerable when narrow. The much-hyped ‘magnificent seven’ presently comprise a freakish 28% of the S&P 500 market capitalization today, a concentration rivalled only near the March 2000 tech-wreck top.

For those betting that last October was the low for stocks this cycle, it bears noting that the equal-weighted S&P 500 index outperformed the market-cap-weighted S&P 500 coming out of the market bottoms in 2002 and 2009, and no such lead is evident thus far. The case for capital protection looms large.

More By This Author:

Resisting Financial SentinelsBuying Power Has Halved, Do The Math

Housing-Led Downturn To Rival 2008

Comments

Log in or sign up to join the conversation.