Semiconductor Stocks At New Highs: Can It Continue?

Semiconductors stocks are on fire. The VanEck Vectors Semiconductor ETF (SMH) is up by almost 28% year to date and trading near historical highs as of the time of this writing.

In this context, it makes sense for investors to wonder if it's still a good time to buy the semiconductor ETF or if the best is already in the past for stocks in the much cyclical industry.

(Click on image to enlarge)

Data by YCharts

Let's take a look at The VanEck Vectors Semiconductor ETF considering key aspects such as valuation, industry trends, and quantitative momentum indicators.

Valuation And Industry Trends

Semiconductor stocks typically trade at a discount versus the broad tech sector because semis are far more volatile and unpredictable in terms of financial performance.

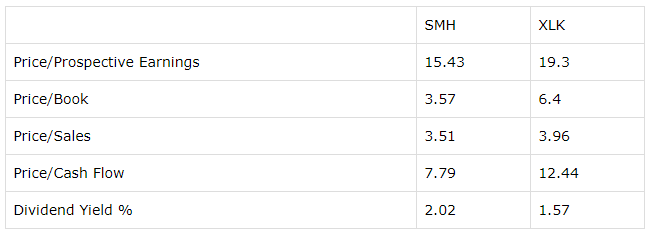

The table below compares the different valuation ratios for VanEck Vectors Semiconductor ETF versus Technology Select Sector SPDR ETF (XLK) and semiconductors as a group are clearly much cheaper than tech stocks in general when looking at a multiplicity of ratios.

(Click on image to enlarge)

Data Source: Morningstar

When considering valuation metrics for semiconductors it is of utmost importance to keep cyclicality into consideration. If you are near the top of the cycle then you should pay low valuations based on current earnings because those earnings are going to decline in the middle term.

Conversely, if the outlook for earnings is improving, then buying semiconductor stocks at a discount versus current earnings can lead to remarkably attractive returns.

The sector has been facing some headwinds over the past several months. Part of this weakness is due to the industry's intrinsic supply and demand dynamics, and the uncertainty produced by the trade war has created additional problems for semiconductor companies.

But the stock market is a forward-looking mechanism. Many of the top players in the sector are seeing signs of a rebound in sales over the coming months, and this is being reflected on rising prices for semiconductor stocks.

In the words of Hock Tan, Broadcom (AVGO) President & Chief Executive Officer:

Our semiconductor business held up relatively well. Not surprisingly, our wireless business was down sharply and our storage business underperformed somewhat. However, these challenges were more than mitigated by our networking business, which grew double digits year-over-year.

In addition, we were very pleased to see that the broadband business has started to recover and stabilize in the quarter. In fact, putting it all together, the semiconductor segment was actually up year-over-year in the first quarter, if you exclude the expected sharp decline in wireless.

Management at Lam Research (LRCX) is also quite optimistic about industry dynamics. From the most recent earnings conference call:

For NAND, 2019 offers what we believe is a solid long-term setup for the industry as the supply growth rate is expected to decline throughout the year. NAND demand should continue to benefit from content increase in consumer and enterprise applications and we began to see initial signs of demand elasticity in the client SSD markets as we exited 2018.

In DRAM, while near-term dynamics remaining challenging, customer behaviour remains rationale and industry profitability characteristics remain compelling. We believe customers are making prudent adjustments to capacity in response to the overall demand environment they are seeing. We expect DRAM WFE spend correction to extend through 2019 with supply growth fall into the mid-teens as we exit the year.

Non-memory segments are expected to grow in 2019 and with the continued rise in the importance of 3D architectures, technology innovation for transistor, interconnect and advanced packaging applications remains a critical priority for us as we grow our strategic relevance with our customers in this segment. In aggregate, we feel confident that we’re operating in a rational industry environment, one that is well positioned to deliver attractive long-term growth and opportunity.

Nvidia (NVDA) is also expecting an improvement over the coming months. According to Colette Kress, Executive Vice President and Chief Financial Officer in the earnings conference call:

As we look past Q1, we expect the channel inventory correction to be behind us and our business to have bottomed.

Micron (MU) President and CEO, Sanjay Mehrotra, is cautiously optimistic about industry trends. In his own words:

Now turning to our DRAM industry outlook. Since our last earnings call, DRAM pricing weakened more than expected. Our demand outlook for calendar 2019 has moderated, led by somewhat greater levels of customer inventory, weakening server demand at several enterprise OEM customers and worse-than-expected CPU shortages. We believe macroeconomic uncertainty is also contributing to hesitation in buying behavior at some customers. However, as we discussed on our last earnings call, we still expect DRAM bit shipments to begin increasing in our fiscal Q3, with demand growth strengthening in the second half of calendar 2019 as most customer inventories are likely to normalize by mid-year.

Management is an interested party in this conversation and investors should always take comments from corporate executives with a big grain of salt. Nevertheless, managers also need to be careful in terms of setting reasonable expectations. A high bar is hard to beat and an earnings disappointment can produce a lot of damage to stock prices in such a volatile sector.

In fact, many executives tend to under-promise and over-deliver since being conservative with guidance resonates well among Wall Street analysts.

You can't take the outlook from management at face value, but you also can't completely ignore what corporate executives are saying about industry trends. If multiple companies in different segments of the industry are seeing signs of improving demand in the coming months, this is probably indicating that there some encouraging signs on the horizon.

The Timing Looks Good

Winners tend to keep on winning in the stock market. When a particular sector is doing well chances are that it will continue doing well over the middle term. In fact, there is plenty of statistical research proving that investors can obtain superior performance by investing in securities with strong momentum over the long term.

The Global Rotation System is a proprietary quantitative system that rotates among a wide variety of ETFs that represent different asset classes and sectors based on risk-adjusted momentum.

The ETFs in the universe are:

- SPDR S&P 500 (SPY) for big stocks in the U.S.

- iShares Russell 2000 Index Fund (IWM) for small U.S. stocks

- iShares MSCI EAFE (EFA) for international stocks in developed markets

- iShares MSCI Emerging Markets (EEM) for international stocks in emerging markets

- Invesco DB Commodity (DBC) for a basket of commodities

- SPDR Gold Trust (GLD) for gold

- Vanguard Real Estate (VNQ) for REITs

- iShares 20+ Year Treasury Bond (TLT) for long-term Treasury bonds

- iShares 1-3 Year Treasury Bond (SHY) for short-term Treasury bonds

- First Trust Dow Jones Internet Index (FDN)

- iShares Nasdaq Biotechnology ETF (IBB)

- iShares U.S. Oil Equipment & Services (IEZ)

- iShares Expanded Tech-Software Sector (IGV)

- iShares U.S. Pharmaceuticals ETF (IHE)

- iShares U.S. Healthcare Providers (IHF)

- iShares U.S. Medical Devices ETF (IHI)

- iShares U.S. Aerospace & Defense (ITA)

- iShares U.S. Home Construction ETF (ITB)

- iShares US Industrials ETF (IYJ)

- iShares Transportation Average ETF (IYT)

- iShares US Technology ETF (IYW)

- iShares US Telecommunications ETF (IYZ)

- SPDR S&P Bank ETF (KBE)

- SPDR S&P Capital Markets ETF (KCE)

- SPDR S&P Insurance ETF (KIE)

- Invesco Dynamic Food & Beverage ETF (PBJ)

- Invesco Dynamic Media ETF (PBS)

- VanEck Vectors Semiconductor ETF (SMH)

- Materials Select Sector SPDR Fund (XLB)

- Consumer Staples Select Sector SPDR (XLP)

- Utilities Select Sector SPDR Fund (XLU)

- SPDR Series Trust S&P Oil & Gas Exploration (XOP)

- SPDR Series Trust S&P Retail ETF (XRT)

The system is basically buying the ETFs with superior risk-adjusted returns over 3 and 6 months, so it's basically buying strength and selling weakness, as simple as that.

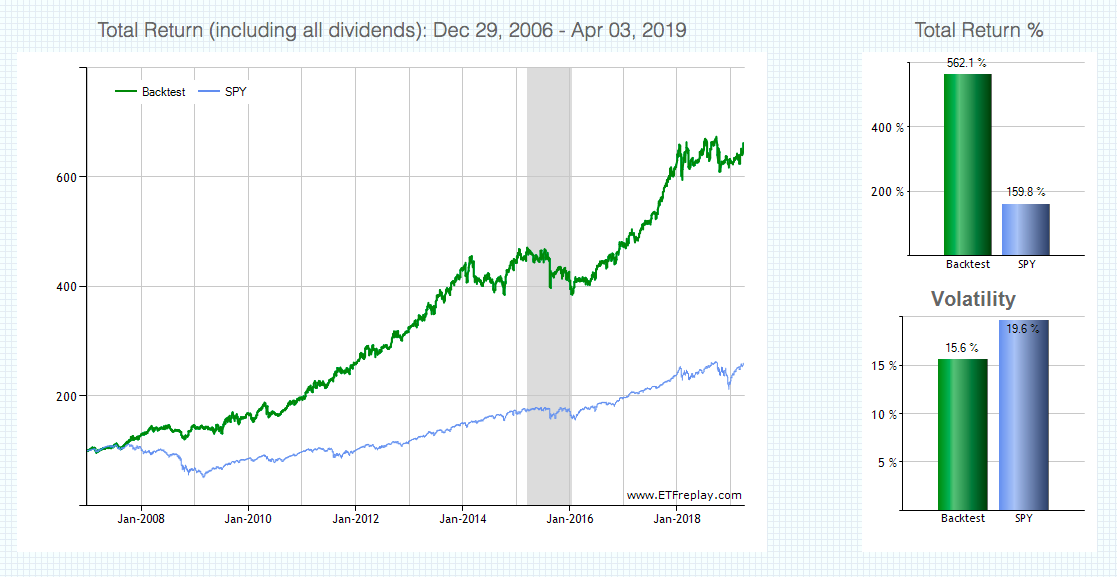

(Click on image to enlarge)

Source: ETFreplay.

Since January of 2007, the Global Rotation System produced a cumulative gain of 561% versus 159.8% for the SPDR S&P 500 in the same period. In annual terms, the system gained 16.7% versus 8.1% for the SPDR S&P 500.

(Click on image to enlarge)

Source: ETFreplay.

The system substantially outperformed the SPDR S&P 500 in terms of downside risk too. The maximum drawdown was 18.4% for the Global Rotation System versus 55.2% for the SPDR S&P 500 in the same period. Drawdown is calculated as the greatest percentage drop from the high.

This strategy does not beat the market in each and every year, and momentum can be a double-edged sword, meaning that the sectors that are delivering superior returns on the way up can many times suffer the biggest losses when markets turn around.

However, the data shows that following the main trends in momentum can be an effective way to increase returns and control for downside risk in the market.

As of the most recent update, VanEck Vectors Semiconductor ETF is one of the 3 portfolio holdings in the Global Rotation System, meaning that the ETF is ranked as one of the top 3 alternatives in the investable universe based on risk-adjusted return metrics.

Final Words

Semiconductor stocks are not too expensive at all and many of the top industry players are expecting improving demand levels in the coming months. In addition to this, the quantitative momentum metrics look quite bullish for VanEck Vectors Semiconductor ETF.

For these reasons, unless we see a significant deterioration in the economic landscape or a big setback in the trade negotiations with China, chances are that VanEck Vectors Semiconductor ETF will deliver solid returns going forward.

Disclaimer: I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in ...

more