Scrooge’s Income ‘L’

We keep revisiting the concept of “residual seasonality” quite purposefully, even though on its face it is an absurd one. It is in every way emblematic of the current state of Economics and the commentary derived from it. Residual seasonality is the kind of delusion that has become commonplace, a coping mechanism for an economy that continues to be very different from how it “should” be working.

It’s the real economy parallel to 2a7, tax reform corporate profit repatriation, or whatever flavor of the month to dismiss as benign these near-constant monetary problems. The Federal Reserve claims the money system is fine, so it must be. Central bank officials declare the economy in great shape and poised to boom, that, too, must be so.

Prominent and conspicuous exceptions abound, of course. One of those is how the US economy has tended to behave in each and every Q1. For “some” reason, each year starts out in weakness rather than anticipated strength. The rest of each year to some degree follows in bewilderment from it, spoiling every time the planned resurgence.

This residual seasonality is for the mainstream a statistical artifact rather than a real process; but only in the sense that such bias leads to this kind of increasingly ridiculous. In common sense terms, by contrast, the idea is surprisingly (to many) simple:

Our contention behind “residual seasonality” has always been that there is no residual but to some extent an understandable and easily explainable seasonal issue. Each Q1 appears to be unusually weak because, well, it is unusually weak. The reason is simply Christmas. Americans splurge for the holiday and then spend the first several months of the following year to some degree regretting it.

Those clear commercial compunctions take the form of a consumer after-holiday holiday. They go on a spending strike of sorts, if only because their spending was pulled forward into the prior Christmas season.

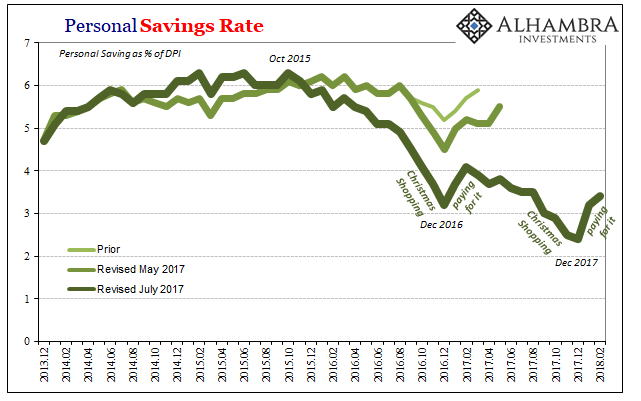

(Click on image to enlarge)

The BEA’s latest estimates for Personal Income and Spending display exactly the same characteristics as we have described. For the second straight year, the Personal Savings rate declined sharply in the months leading up to season, and then rises in the months (January & February) immediately following.

But wait; residual seasonality is perfectly evident over the last two years, but as a concept was born earlier, springing from historical observations going even further back in time. If this Q1 pattern existed during those prior seasons, why do we only see it so clearly over the past few?

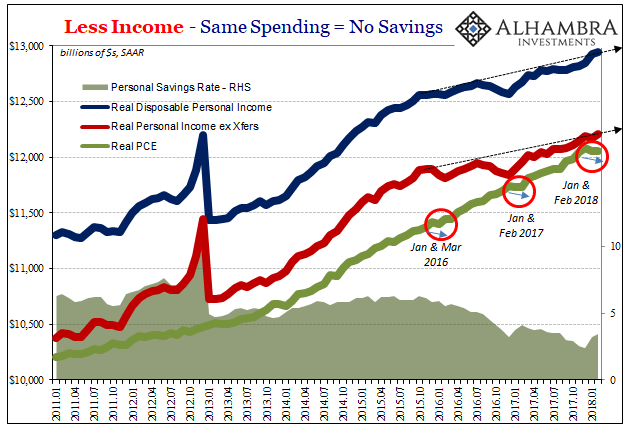

(Click on image to enlarge)

The answer is once again quite simple. Because the economy since the 2015-16 downturn is doing the opposite of booming “residual seasonality” has actually become more flagrant. Going by mainstream rhetoric alone, guided exclusively by the unemployment rate, these are shocking results. Using instead the several key income statistics the BEA also supplies, they are all perfectly and uniformly consistent – both with the honest version of residual seasonality as well as the picture of an economy stuck in distress.

The degree to which it has been struggling is somewhat obscured even on the chart above where the downward bend for the income trajectory is still perfectly evident. This is the part that is captured in the Personal Savings Rate and its collapse since 2015.

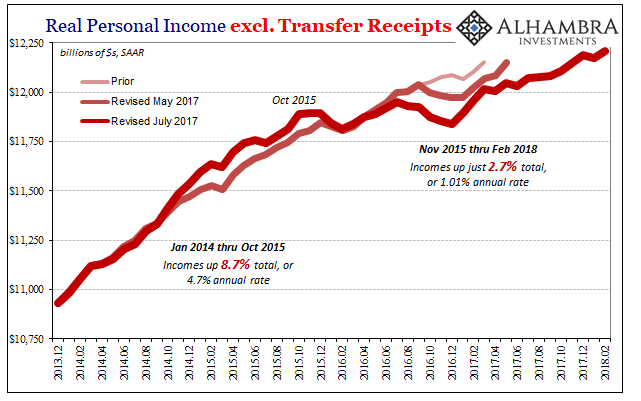

(Click on image to enlarge)

In other words, when policymakers were closest to finally embracing recovery, 2014, Real Personal Income excluding Transfer Receipts (RPIxTR) was growing at a nearly 5% annual rate. Given the last ten years, that appeared to be significant. Given historical experience, it was still lackluster.

Thus, just when the economy was thought ready to take off it fell into the opposite. Worse, however, that “unexpected” and “transitory” downturn has month after month proven to be lasting. Since November 2015, through the latest estimates for February 2018, a significant span of 28 months, RPIxTR has gained just 2.7% total; an annual rate of just about 1%.

That’s utterly atrocious suggesting lasting economic strain, especially as it represents labor income across the whole of the economy and for more than two years (and counting). There is absolutely no way the economy can be booming, or can be about to, given these figures.

Rather, what they propose is what we are seeing in China. These are the effects of an “L” paradigm, where for each downturn (starting with the big one in 2008) there isn’t an actual recovery (asymmetry) from it. Every time whichever economy, including our own, goes through these “dollar” originated events, it emerges worse off for the experience.

Last year, 2017, was after clearing the last downturn in 2016 supposed to be the year which changed all our economic fortunes; the beginning of different. It got off to the worst possible start, the same residual seasonality only amplified by that much-reduced income trajectory.

(Click on image to enlarge)

This year, 2018, is already emerging with the same pattern. More concerning, it takes on that pattern from a weaker starting point. What might that propose for the rest of the year and beyond? The only way to answer that question by claiming an imminent boom is to purposefully turn residual seasonality into a statistical question far outside of corroborated common sense.

Disclosure: None.