The equity market struggled again last week as the S&P 500 saw its fourth consecutive weekly loss. The Nasdaq underperformed, ending the month lower by more than 10%. It was the worst month for technology shares since 2008. Disappointing earnings reports from tech giants such as Amazon (AMZN) and the prospect of a more aggressive tightening by the Fed pushed equities lower. The energy sector outperformed on the back of higher oil prices. The WTI crude rose for the week as tensions rose between Russia and the European Union over energy. The Commerce Department reported that the U.S. economy contracted by 1.4% in the first quarter, way below expectations. A record trade deficit was mainly to blame as consumer spending remained strong. Other economic data such as capital goods orders and personal spending showed continued expansion. The 10-year U.S. Treasury yield ended the week unchanged at 2.94%, but there was underlying volatility as the yield reached the low of 2.72% earlier in the week before rising.

The Fed will convene at its upcoming FOMC meeting on Tuesday and Wednesday, and it is widely expected to raise the Federal Funds Rate by 50 basis points on Wednesday. The Fed is also expected to begin winding down its balance sheet this month. Several key economic data on the labor market’s strength will also be released with the JOLTS report on Tuesday, ADP National Employment Report on Wednesday and the Labor Department’s nonfarm payrolls report on Friday. Hiring in April is expected to remain strong despite preliminary data showing that the U.S. GDP contracted by 1.4% in the year’s first quarter. Earnings season continues with many notable companies reporting, such as Pfizer (PFE), AMD (AMD), Starbucks (SBUX), and Uber (UBER).

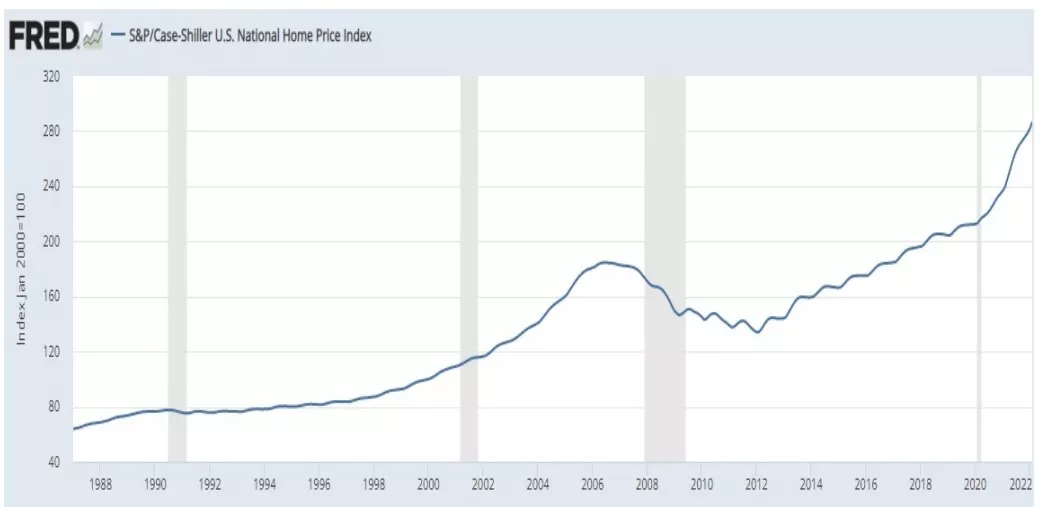

The U.S housing market continues to run hot as single-family home prices and price appreciation have reached new records. According to the S&P Case-Shiller national home price index, home prices increased by almost 20% in February from a year ago. The supply of existing homes for sale is the tightest in several decades, and housing affordability is at its lowest point since the financial crisis. Rising mortgage rates have historically ended home price appreciation, but it might be different this time. The limited supply of homes for sale, significant home equity, and healthy household for sale, indicate that we will not see the housing market correction during the financial crisis. Homeowners today are in better shape financially than in previous housing cycles, as they have less debt, more home equity, and manageable mortgage payment. The supply of homes should remain low as mortgage rates rise and homeowners have more incentive to stay locked into their lower rates. For this reason, home price growth might slow but will remain positive soon. SOURCE: FRED Economic Data

Comments

Log in or sign up to join the conversation.