The jump in May services activity follows a steep plunge into contraction territory in April. So, we prefer to look at a two-month average, which paints a picture of solid but slowing service sector growth. With employment in contraction territory for a fourth consecutive month, businesses appear wary about the future.

Image source: Pixabay

The May US ISM services index rose quite a bit more than expected to a nine-month high of 53.8 from 49.4. It was led by strong business activity (61.2 versus 50.9 in April) and rising new orders (54.1 versus 52.2) which, in turn, appears to be driven by export order strength (61.8 versus 47.9 in April). The volatility in the activity component is surprising and it may be best to take an average of May and April, which would give 56.1 versus 57.4 in March and 57.2 in February.

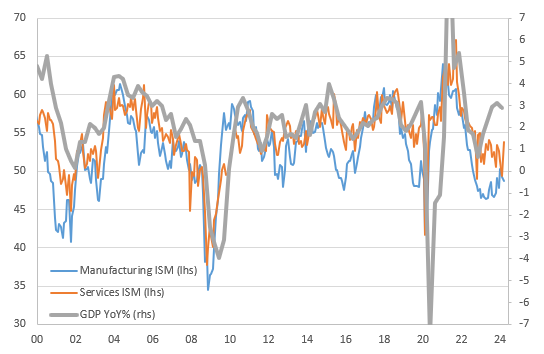

So that would be consistent with firm, but modestly slowing services activity. As the chart below shows, the ISM business surveys, which have historically been amont the best lead indicators for the path of the economy, continue to paint a weaker growth story than the official GDP growth numbers indicate.

ISM headline indices and GDP growth (YoY%)

Source: Macrobond, ING

The employment sub-component did improve modestly but remains in contraction territory at 47.1 (the fourth month in a row it has been below the 50 break-even level). It seems firms remain reluctant to add additional workers and again points to a cooling of employment in Friday’s jobs report - as did the softer-than-expected ADP employment number. It also, perhaps, suggests again that the surge in business activity seen in today’s May report is not seen as sustainable, hence why we should indeed take an average of April and May.

Rounding out the main components, prices paid slowed to 58.1 from 59.2 and we would expect that to ease further over the next couple of months as lower oil prices feed through into lower fuel costs.

More By This Author:

Bank Of Canada Cuts Rates By 25bp

Rates Spark: US Growth Pessimism Drives Yields Lower

FX Daily: Can Softer US Data Slow The Carry Trade Unwind?

Comments

Log in or sign up to join the conversation.