Image Source: Unsplash

Spread between USD and EUR rates can widen further

Since Trump's election, global rates seem less correlated to US rates, also helping the euro swap curve move more independently. Trump’s tariff threats, for instance, are seen as inflationary for the US, whilst potentially deflationary for the targeted country, triggering opposite rate reactions. In the eurozone we already saw a strong repricing for more European Central Bank cuts when Trump initially threatened with tariffs against Canada, Mexico and China – whilst the impact was on the hawkish side for the Fed. The latest reaction to Trump's steel tariffs had almost no notable impact on euro rates.

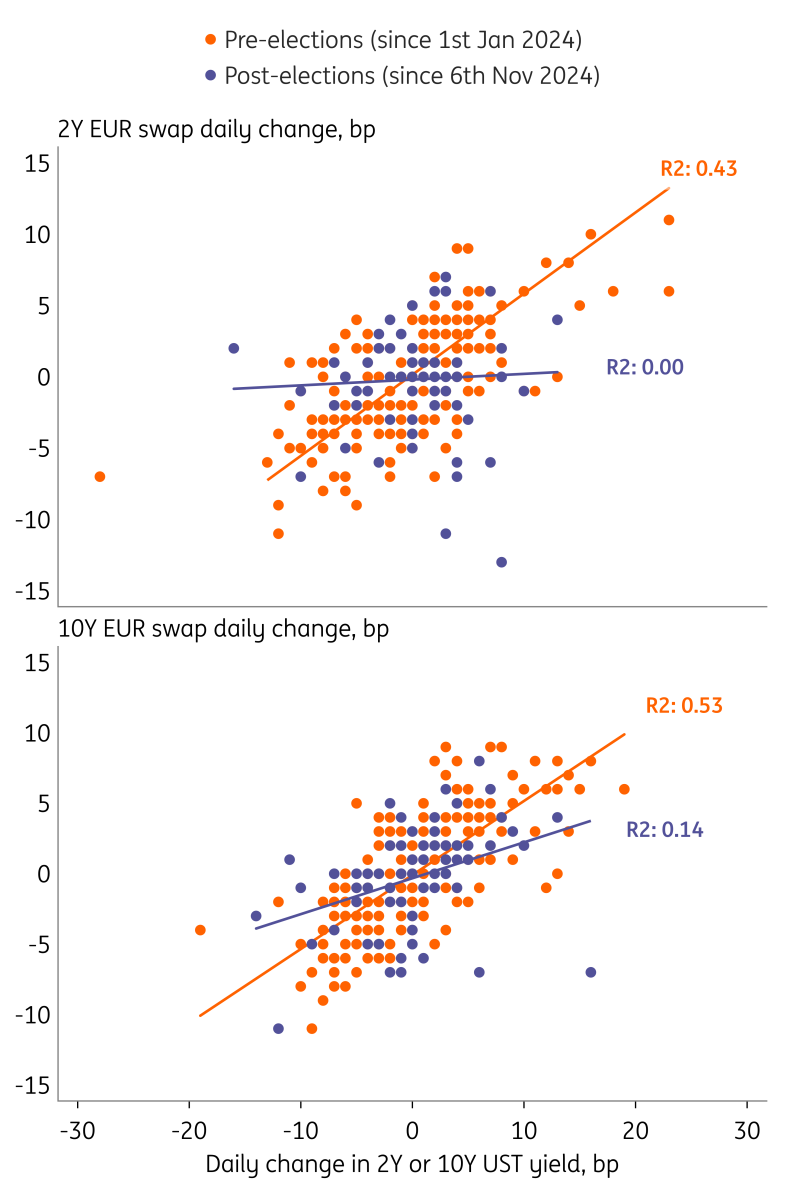

When looking at the entire period since Trump’s election, the correlation between daily changes of the 2Y euro swap rates and 2Y UST yields actually fell to zero (see figure below). Further out the curve we also see that USTs have less spillovers than earlier in 2024. Before the elections in November, more than 50% of the daily variation in 10Y euro swap rates could be explained by changes in the UST yields. This is reduced to 14% since. Besides tariff threats there were other factors in play here, including the more downbeat data releases in the eurozone compared to the US.

With euro rates less tied to US dynamics, the spread differential with UST yields could widen further. The spread between the 10Y euro and the 10Y SOFR swap is now 175bp, just below the peak of 185bp in 2018. We see more scope for the front end of the euro curve to nudge lower in the near term, and the spillovers hereof further out the curve would put widening pressure on the back end too.

Correlation between eurozone and US rates has declined sharply

Source: ING, Macrobond

Tuesday's events and market views

Another light day in terms of data, with the US NFIB small businesses survey the most notable release. The optimism index is expected to tick slightly lower from 105.1 to 104.7. More interesting may be the various central bank speakers, including the ECB's Schnabel and from the Fed Powell, Williams and Bowman.

Plenty of supply scheduled, including an EU dual-tranche syndication for an estimated €10-11bn (7Y and 25Y increases) and an Italian syndication of a new 15Y for c.€10bn. The Netherlands will auction a €2bn DSL, whilst Germany has a 5Y Bobl auction planned for €5bn. Also, the UK has announced a syndication for a total of around £12bn of new 10Y gilts. Lastly, the US has planned a 3Y Note auction for $58bn.

More By This Author:

The Commodities Feed: Trump Plans 25% Tariffs On All Imports Of Steel And AluminumFX Daily: Spreads And Tariffs Keep Dollar In Demand

Think Ahead: Inflation Confidence Shifts To Caution

Comments

Log in or sign up to join the conversation.