Rates rallied on a mix of supply relief, weaker data and the Fed pointing to the tightening impact of the still overall higher long-end rates. Before we test further downside, we likely have to see tomorrow’s payrolls report first. Today's BoE meeting should complete the unfolding holding pattern across major central banks.

The market remains firm in its expectation of the Bank of England keeping rates on hold at today’s meeting, which is also is our view.

US rates rally on a mix of supply relief, weaker data and a Fed "proceeding carefully"

US rates drove a bull flattening of curves. At the end of the US session, the 10Y UST yield rallied below 4.75% with the 2s10s curve flattening 5bp on a mix of supply relief, weaker data and the Federal Reserve pointing to the tightening impact of the still overall higher long-end rates.

The Treasury’s refunding announcement was deemed tolerable, partly because the headline requirement of the upcoming November refunding of US $112bn was $2bn lower than the market had expected. But more importantly, the gradual increases of auction sizes over the quarter were focused on shorter tenors, with 2Y, 3Y, 5Y, and 7Y sizes increasing by $9bn, $6bn, $9bn, and $3bn respectively, by the end of January 2024. In contrast, 10Y and 30Y new issue and reopening auction sizes were increased by only $2bn and $1bn, respectively, and 20Y auction sizes were left unchanged.

The Fed kept rates on hold and maintained a hawkish bias, pointing to further tightening becoming less likely. The Fed acknowledged that the higher real rates are having a clear tightening effect, and it can let the debt markets do the last of the pain infliction for them. The rise in real yields has helped to push the curve steeper, and the 5s10s has recently joined the 10s30s with a positive upward-sloping curve. Only the 2s5s spread remains inverted. This overall look does suggest the bond market is positioning for a turn in market rates ahead. The big move will come when the 2Y starts to anticipate cuts.

Yields turn lower, but 5% is not entirely out of reach yet for the 10Y

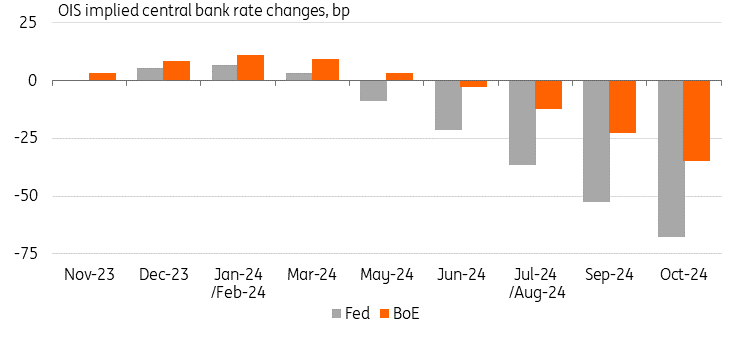

Refinitiv, ING

BoE to complete the holding pattern across major central banks

It feels like the Bank of England is more of a sideshow given the gyrations spilling over from the US. The market is also quite firm in its expectations of the BoE keeping rates on hold at today’s meeting and it is also our view. However, looking a little further ahead the markets still see a more than one-in-three chance that the bank rate could be raised one more time. The Monetary Policy Committee is unlikely to close the door to further tightening, but as holding patterns of other major central banks are unfolding, this pricing could eventually shift even more towards reflecting the “Table Mountain” once touted by the Bank’s chief economist.

Central banks seen on hold for the next months

Refinitiv, ING

Today’s events and market view

The UST yield now sits notably lower at 4.73%, but it has not materially broken any trends though. Before we test further downside we likely have to see tomorrow’s payrolls report first. An outcome close to the consensus might not be enough to materially lower rates from here.

There is still a path back up to 5%. We still feel that pressure for higher real rates remains a feature, despite the easing off on longer tenor issuance pressure. We need to see the economy really lurch lower, in particular on the labor market, before the bond bulls take over.

That said, there will be other job market indicators out already today such as the Challenger job cuts data and the usual weekly initial jobless claims figures. Factory orders and the final durable goods orders round off today's US data releases. In Europe, the BoE decision takes center stage. For the eurozone, we will be looking at the unemployment data, but probably focus more on what European Central Bank key officials Philip Lane and Isabel Schnabel will have to say.

Today’s government bond supply will come from France in 10Y to 50Y maturities and in Spain in 5Y to 30Y maturities.

More By This Author:

FX Daily: Fed Pause Renews Interest In The Carry TradeAsia Morning Bites For Thursday, November 2

U.S. Federal Reserve Keeps Its Options Open With Another Hawkish Hold

Comments

Log in or sign up to join the conversation.