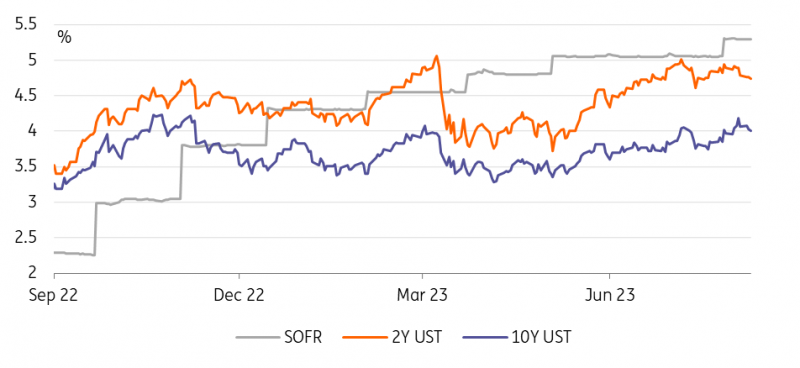

The US 10yr fell back below 4% briefly, but it took a decent bout of risk-off to force it there. There is a more natural place for the 10yr yield at above 4%, based on the forward discount for the funds rate (and that has not materially changed).

US yields are off last week’s highs, but still feel under net upward pressure

It took a bout of risk-off to briefly take the US 10yr yield back below 4%, well below the high of 4.2% seen on Friday. That was always likely to be the cleanest route to taking the US 10yr yield down. But it did not stay below 4% for long, and we remain of the opinion that the 10yr sits more naturally at above 4%, at least for now. The 10yr should trade at a 20-30bp premium to the forward discount for the funds rate low, and that's only just below 4%.

We’ll also get an inflation reading on Thursday, likely confirming that US headline inflation moved back up towards 3.5%, while core inflation is finding it tough to make a material break below 5%. The point estimates here at 3.3% and 4.7% respectively on 0.2% month-on-month outcomes. These are much better than they were (the headline peaked at 9%), and the rise in the headline rate for July is just a base effect. But inflation dynamics are not yet in what could be called a comfort zone.

We also have continued supply to take down over the course of this week. The 3yr auction on Tuesday saw a good reception. It was well covered, saw a strong indirect bid (including central banks), and no tail (or technically a negative one, which is good). There is more duration to take down ahead as the 10yr and 30yr auctions are up in the coming days. The volume of supply has been upped since the last outing. It should get taken down okay.

In fact, the flow of data over the last few weeks shows good demand for the duration despite the upward pressure seen on bond yields. Had it not been for this buying, the 10yr Treasury yield could likely have attacked the previous high seen in the 4.25% area. We’re still at better levels than before for buyers. But supply is also a weight to be taken down, placing upward pressure on market rates.

Off the recent peak, but we think 10Y UST sit more naturally above 4% for now

Refinitiv, ING

Today’s events and market view

Global growth concerns eying developments in China, a new bank tax in Italy, as well as rating jitters surrounding US banks all contributed to the risk-off sentiment that sparked yesterday’s bull flattening.

While tomorrow's US CPI data looms large, today’s calendar holds little to extend that rally. The focus could instead be on today’s supply where Germany taps its 10Y benchmark for €5bn and the US Treasury later sells US$38bn in new 10Y notes.

More By This Author:

FX Daily: Temporary And Contrasting DriversAustralia: How to ride a bumpy disinflationary path

To Hike Or To Hold? Three Scenarios For The Bank Of England’s Next Steps

Comments

Log in or sign up to join the conversation.