Rates Spark: No Respite

The respite has been brief for rates markets as the sell-off resumed yesterday, taking yields back to the previous week’s highs. Inflation angst is still playing out with inflation swaps and breakeven rates climbing. At least the Fed should have more room to act. US curves are starting to come around to this but still need convincing.

Does the Fed have more room after all?

While UK rates have been in the lead again in the European session, even in the US, usually more removed from the impact of oil and gas prices, breakeven rates broke above recent ranges and are climbing to the highest levels since June. But the move here is also underpinned by better macro data in the form of yesterday’s ISM services and PMIs as well as some warm words regarding fiscal spending plans. The fate of the debt ceiling still has a major question hanging over markets, with uncertainty about the democrats' legislative strategy, republican opposition, and a deadline approaching fast.

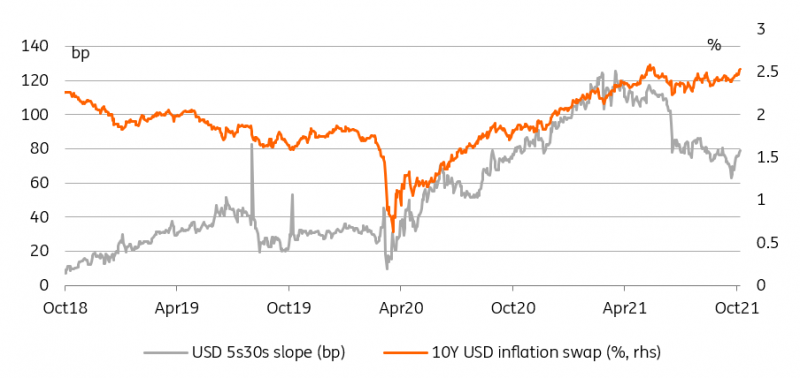

Greater inflation risk is re-steepening the US curve

Source: Refinitiv, ING

Markets are of course waiting for Friday’s US jobs data to provide the final green light for the Fed to announce the taper next month. But more importantly it appears that markets are coming around to the notion that the economic underpinnings could indeed allow for a more forceful Fed reaction to counter the inflationary dynamics without choking off the recovery in the process. To be sure, that has been the view of our economists for some time already leaving more upside for rates.

We saw yesterday the usually policy sensitive 5Y swap rate attempting to cheapen again on the curve versus 2Y and 10Y. The 30Y swap rate is almost 10bp higher this morning taking it beyond 1.87%. Lingering concerns over the long term economic outlook had kept the 5Y30Y curve trading with a flattening bias for some time, but it had started to re-steepen and continued to do so yesterday. It may be premature to say that the market has come to a final verdict, though. Taking a step back the 5Y30Y swap curve still looks flat compared to earlier episodes of higher inflation (expectations) with the 30Y swap rate itself trading at 2% the last time when break-evens were this high in early June (TLT, SPTL).

The ECB sticks to its mantra, but unease is spreading

Currently high price pressures are a transitory phenomenon is a mantra that has been reiterated over and over by the ECB. But it seems that even here subtle shifts of tone are taking place. Austria’s Holzmann voiced his concerns over more lasting effects – he of course is a known hawk among the ECB council. But even Villeroy’s once apt description of the ECB’s stance as “vigilant, but not worried” has morphed to a “vigilant, but not feverish”. Perhaps an acknowledgment of the increasing concerns.

While we see EUR (FXE) longer term inflation swap measures moving to their highest levels since 2013, it has yet to translate into any expectation of the ECB tightening its policies more aggressively in the near term. Most notably periphery bond spreads, which would be most susceptible to a significantly slowing of asset purchases, have so far remained relatively calm. Sure money market curves have steepened, but that means short-term EUR rates are now expected to reach zero in 2026.

Today’s events and market view

With little else to grab the headlines today the US ADP payrolls data – despite its mixed track record as predictor – should garner the attention of markets trying to get a better sense of Friday’s official jobs data. For the latter the consensus forecast has nudged slightly lower to 488k jobs added over September.

The eurozone will see the release of retail sales data and a public appearance of ECB’s Centeno. In light of the rising energy prices markets are on the lookout for any ever so faint change in officials’ tones regarding inflation risks.

Supply takes a bit of a breather at least in duration weighted terms with a €4bn 5Y tap out of Germany.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does ...

more