Ever Growing Case For A Faster Taper

News surrounding the new Omicron variant of the Covid virus are likely to maintain the upper hand today. Steep increases in case counts in South Africa, where the variant was first detected and has quickly become the dominant strain, the notion that perhaps not all cases are as mild as hoped put a damper on sentiment, especially as the first case has now been detected in the US. In the absence of hard scientific evidence, markets continue to cling to every new headline.

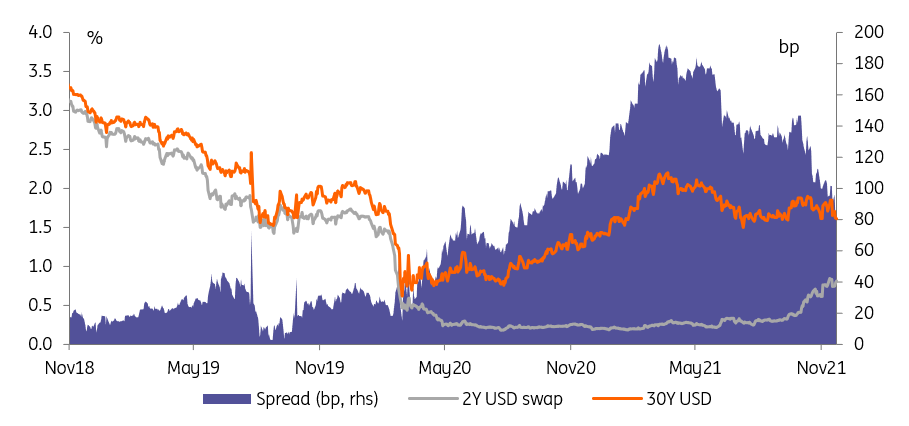

30Y US Rates Are Caught Between Omicron And A Hard Place

Image Source: Refinitiv, ING

The economic backdrop would make a strong case for the Fed to accelerate tapering soon

10Y US Treasury yields are testing last month's lows just above 1.41% for now, but in light of a Fed turning more hawkish has yet refrained from breaking lower. Omicron aside the economic backdrop would make a strong case for the Fed to accelerate the tapering of asset purchases soon. Powell laboured the point in his second day of congress testimony, and Loretta Mester was the latest FOMC official to throw her weight behind the idea. What's more, yesterday’s ISM manufacturing index not only highlighted the strong job markets in the sector – raising expectations of a robust non-farm payrolls increase tomorrow – but also the increasing pricing power of companies. A similar picture was painted by the Fed’s Beige Book, reporting “robust wage growth” in nearly all districts and price pressures also being pointed out.

Postponed ECB Decisions? Careful What You Wish For...

Even more so than for the Fed the outlook is muddied for the ECB at a critical vantage point. A sources story on Reuters pointed to an increasing desire to postpone any long-term decision on the future of its asset purchase programmes to a later stage. An announcement to end PEPP after the first quarter next year is still very likely, but what follows may only be decided shortly before that date, ie, as late as the February meeting.

Reportedly, a growing number within the ECB that believes inflation could be at or above target in 2023

At first reading, a delay may be seen as dovish, but it is a two-edged sword. Not only does it extend a period of uncertainty and, alongside it, volatility. As there is reportedly a growing number within the ECB that believes inflation could be at or above target in 2023, sitting out the current turmoil surrounding the fourth pandemic wave and the Omicron variant, may actually lead to less dovish decisions further down the road. The resurgence of the virus could prolong supply chain disruptions and therefore add to growing medium-term inflation concerns.

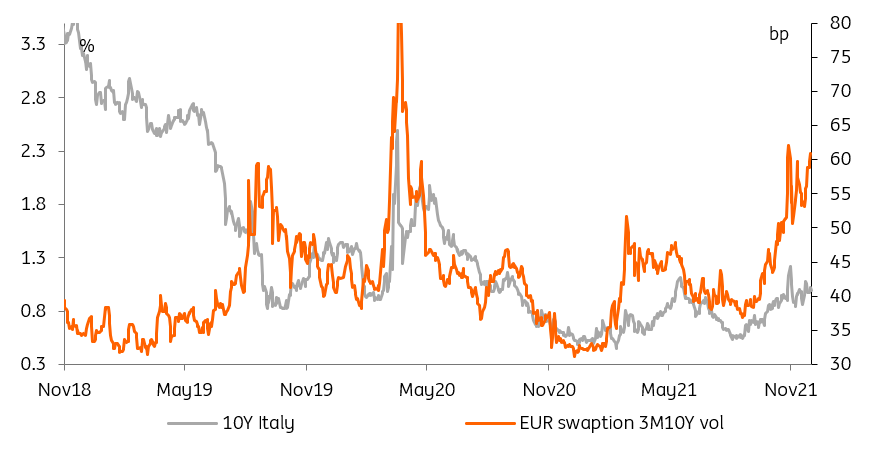

Prolonged ECB Uncertainty Means Higher Volatility And Italian Yields

Image Source: Refinitiv, ING

Markets have already been stubborn in pricing in the possibility of ECB rate hikes already in 2022. It appears that also periphery debt is increasingly waking up to the notion of fading ECB support via asset purchases – and that could happen even quicker than rate hikes. This is especially painful as market volatility has already been increasing with prospects of tightening monetary policies globally. The benchmark 10Y spread between Italian and German government bonds stood at times 5 basis points wider yesterday and has now at 135bp reached its highest level in more than a year.

Today's Events And Market View

Markets remain very much at the whim of Omicron-related headlines. In data, the US will be looking at initial jobless claims, though it is likely again today’s Fed speakers that will grab the headlines. They include Bostic, Daly and Barkin. The Eurozone will see the release of producer prices and an appearance by the ECB’s Panetta, a dove.

Supply will come from France and Spain. France’s smaller sized (€3-4bn) reopening of three bonds in the 10Y to 15Y sector will be its final sale for the year. Spain will sell up to €3.25bn in 4Y, 10Y and inflation linked bonds, but has still one more auction scheduled for the year.

Comments

Log in or sign up to join the conversation.