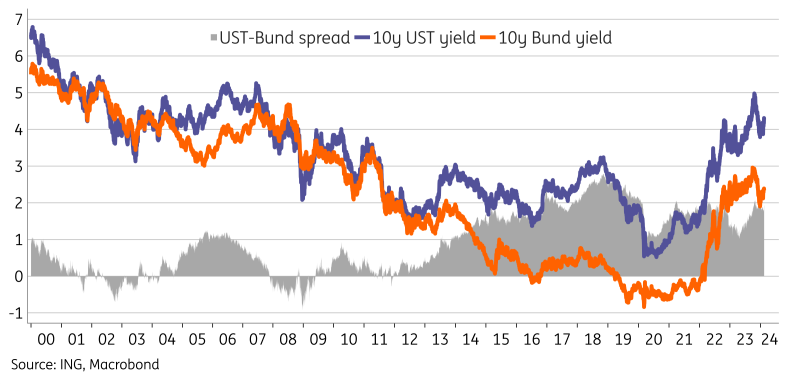

The spread between 10y USTs and Bunds is still too wide in our view and relied on a few big US numbers. At the same time, the economic outlook in the eurozone has also been improving and thus justifies a smaller spread. We tactically target 2.45% for the 10y Bund yield.

Image Source: Pexels

The UST-Bund 10y spread widening should see some reversion

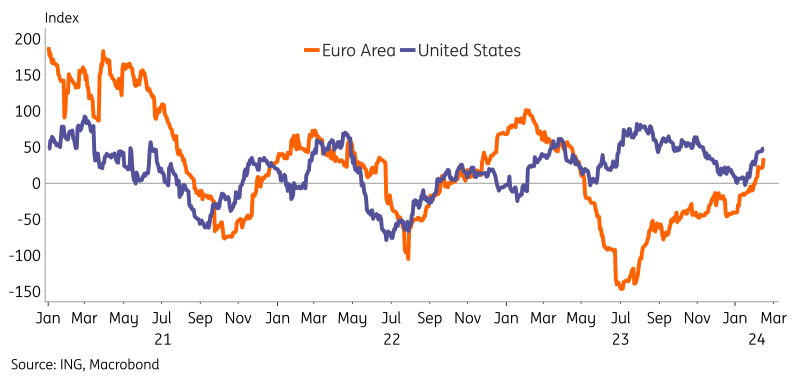

The sharp uptick of US yields in reaction to the CPI release earlier this week has again widened the spread between USTs and Bunds and thus we see some catch-up is needed by Bund yields. Today already saw a few basis points of spread compression, but we see scope for more. First of all, the eurozone economy has shown positive signs of late, but since this wasn’t centered around a few single numbers – such as the big payroll figure in the US – the growth side has been less pronounced. Nevertheless, in aggregate, upside surprises have dominated as evidenced by the Citi Surprise Index in the chart below.

Secondly, looking forward we see scope for growth to recover in the eurozone, even if only subdued. For example, consumption growth will provide some support on the back of falling inflation and strong wage growth. Credit demand also seems to decline at a lower pace, which should be interpreted as a positive development in light of a restrictive monetary policy stance. Next week's PMI figures could be a catalyst to point markets to the conclusion that the US is not the only one with an improving economic outlook.

Eurozone economic surprises have turned more favourable

Lastly, as in the US, we do not see rate cuts being priced in earlier than they currently are – much of the 10y yield moves were driven by the timing of rate cuts. In Europe, Lagarde made it very clear today that the European Central Bank will move with patience. Notably she did not downplay the importance of wage data this time, which suggests that the ECB will want to wait for those data points in April before plotting the next move.

Currently, the 10y UST-Bund spread is hovering around 190bp, well above historical averages (see second chart) and also in our structural view we think this should be lower. A spread model based on differentials on the short end of the curves suggests that the scope for a lower spread is currently at least 10bp. Together with our tactical call for slightly higher UST yields, we thus target 2.45% for the 10y Bund yield in the near term.

UST-Bund 10y spreads are also high relative to historical values

(Click on image to enlarge)

Friday's events and market view

After already a busy release calendar, the UK finishes the week with retail sales. After disappointing GDP figures on Thursday, the retail numbers could shed some light on the most recent economic developments, which according to our economists should look brighter going forward. In the US producer price inflation at sub-2% could still confirm sub-3% inflation expectations allowing Treasury yields to further fade from this week's peak. A nudge higher in consumer sentiment as is expected from the University of Michigan surveys could work in the same direction. Other data releases are housing start numbers and building permits.

The Fed's Barkin, Barr and Daly will speak on Friday. From ECB we have Schnabel speaking, who is one of the most influential hawks, and from the BoE Huw Pill.

More By This Author:

UK Growth Outlook Improving Despite Fourth Quarter SetbackWeak Start To The Year For U.S. Retail Sales And Manufacturing

Asia Week Ahead: Central Bank Decisions, RBA Minutes And Activity Data From Japan

Comments

Log in or sign up to join the conversation.