Economic releases should prove more relevant to interest rates' direction. Hawkish Fed soundbites are set to increasingly fall on deaf investor ears. EUR rates rightly continue their re-pricing lower, with the front-end likely staying in the lead.

FOMC minutes to sound hawkish, and to be ignored by the market

The minutes of the June FOMC meeting relate to discussions that took place before the washout in rates that has occurred in the past two weeks. Some data has been made public since then, cementing the market expectation of a sharp growth slowdown, but we would argue that this is not so much as to justify the magnitude of the move lower in yields. Our opinion is that interest rates have caught up late to what other financial markets have known for a while: the risk of recession casts a long shadow on rate hike expectations.

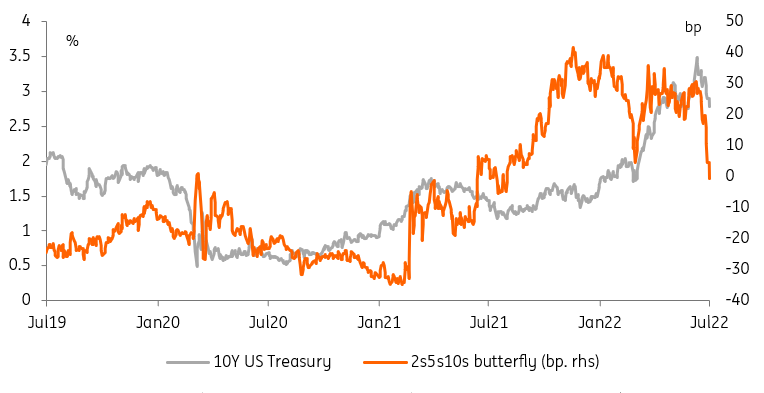

Treasury yields and the shape of the curve challenge the Fed's outlook

Source: Refinitiv, ING

If slightly dated, the minutes will show discussions that were unpolluted by the extent of the move lower in interest rates. With no clear sign of a deceleration in inflation, our economics team sees no reason for Fed officials to drop their hawkish rhetoric. In fact we even expect a 75bp hike in July, barring a sharp weakening in employment indicators in this Friday’s report. If Powell’s recent remarks are anything to go by, the tone of the FOMC minutes will cause cognitive dissonance, with markets now openly questioning how far and how long the Fed can tighten policy before having to reverse course.

Economic data will be key

It’s a tough call given the degree of market volatility, but we are of the opinion that the yield peak is in for this cycle. With markets increasingly perceiving central banks as being behind the curve, we tend to regard economic data as more liable to dictate interest rate market direction than another barrage of hawkish speak. In that regard, today’s ISM will prove key in helping bonds hold on to their recent gains.

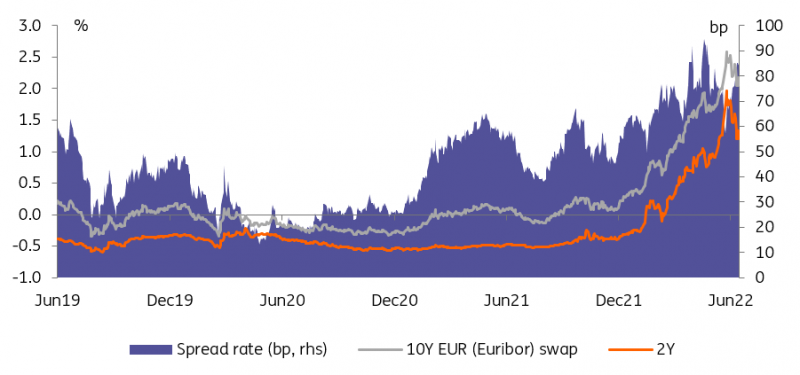

The drop in short rates should continue to outstrip the long-end

Source: Refinitiv, ING

Over in Europe, the collapse in the EUR/USD exchange rate, and sell-off in European stocks, are the latest symptoms of the economic malaise that is gripping financial markets. In this context, and bearing in mind that even with the recent re-pricing, end-2023 €STR forwards are still around 100bp above our forecast, we continue to see EUR rates downside. It seems logical to us that the move should be greater at the shorter end of the curve. In a context where recession concerns are more marked than, say, in the US, and as supply weighs on the sector, it would see logical that long bonds struggle to participate in the rally to the same extent.

Today’s events and market view

After this morning’s German factory orders, Eurozone data will be mostly second tier. Still, look out for Eurozone retail sales. The afternoon (or US session) will be livelier with no less than PMIs, ISM services, JOLTS job openings, and June FOMC minutes. As we wrote in the first section (see above), markets will be particularly sensitive to signs of a turn lower in economic activity. In that regard, the ISM services index could prove most market-moving. A low print in the employment and price sub-components in particular would push the curve to shave off more Fed hikes this year.

Hot on the heels of yesterday’s linker sales, Germany will add to supply with a 10Y Bund auction worth €5bn. Together with France's long end auction scheduled for tomorrow, it should prevent long rates from dropping as fast as their short-term equivalents.

Central bank speak will ramp up, with speeches from Olli Rehn of the European Central Bank, Huw Pill and Jon Cunliffe of the Bank of England, and John Williams of the Fed.

More By This Author:

FX Daily: Recessionary Fears Drive Dollar To 20 Year HighsEuro Credit Supply: Higher spreads are keeping supply limited

FX Daily: Risk Environment Gets Some Chinese Support

Comments

Log in or sign up to join the conversation.