Image Source: Pexels

As you read this, the U.S. debt smashed through a record level of $33.5 trillion. And it’s rising by the minute.

But this isn’t the only cloud on the domestic or global horizon…

As you know, last week, Hamas launched an unprecedented attack on Israel. Israel declared war on Hamas in retaliation.

And regional and global ramifications are mounting in the Middle East in a very fluid, escalating situation.

At the same time, Congress has no Speaker. The 2024 congressional budget debates continue, with no agreement on an official budget. And the war in Ukraine rages on.

With all of the turmoil, global volatility, and booming U.S. debt, one story hasn’t been getting much attention lately. But it could have an even bigger impact on your money.

I’m talking about the global push away from the dollar, which I’ve been writing about in these pages.

Today, I’ll show you how the BRICS+ bloc is angling to break the U.S. dollar’s position… And use it as more fuel for its de-dollarization fire.

The De-Dollarization Wave Is Sweeping the World

To be clear, the U.S. dollar isn’t going away.

In fact, it has been bolstered as a safe haven in the wake of the Hamas attacks on Israel… And Israel’s latest call for 1.1 million Palestinians to evacuate Gaza in what could be a pre-emptive move into ground strikes.

And, as I wrote last Thursday, the dollar won’t cease to be the world’s primary reserve currency in any of our lifetimes.

But steps are underway right now to curtail some of its uses.

That matters because its influence and power in many ways helped steer the U.S. economy over the past few decades. Now, swipes against it are growing in number and severity.

The dollar has been the world’s main reserve and international business currency since the end of World War II. That’s when the U.S. became the global economic superpower it is today.

And although it’s still on top, the U.S. dollar’s share of central bank currency reserves has dropped from more than 71% in 1999 to 59% today.

Meanwhile, the euro stands at 21% and the Japanese yen around 6% of global central bank reserves.

In the past, U.S. dollar alternatives and rivals came from other G7 currencies like the euro and even the British pound sterling.

[G7 stands for Group of Seven. It’s a political forum consisting of Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.]

These currencies largely offered stability and minimal volatile swings, and they were in relatively secure countries that investors could rely on.

In 1999, for example, I was running the analytics group as a senior managing director at Bear Stearns in London.

The big question that year was whether the euro would overtake the U.S. dollar as the world’s reserve currency… or at least take a big chunk out of it.

As we now know, that didn’t happen. King dollar still shines, just a little bit less brightly.

But, while those other G7 currencies were once seen as a threat, they aren’t the reason behind the dollar’s decline today.

The Other Contenders

Since the time of the euro’s launch in 1999, China has emerged as a true global superpower.

The Chinese economy opened its doors to the world and experienced a growth boom that offers no comparison.

But around the world, we’ve rarely seen two great powers exist without mounting competition. That competition often leads to war or proxy cold wars.

That’s why, today, China is a main driver of de-dollarization.

Yes, it is true that, for now, China’s currency as a share of global reserves remains low – just under 2.5%.

But China’s drive to replace U.S. dollar-based trade with yuan-based trade has been enough to chip away at the dollar’s dominance.

Allocation to the dollar in global central bank reserve accounts is a case in point. It fell to 59% – a 25-year low – in 2020.

China’s BRICS partner, Russia, has played a part in this. Russia’s central bank now holds about a third of all of its reserves in the Chinese yuan.

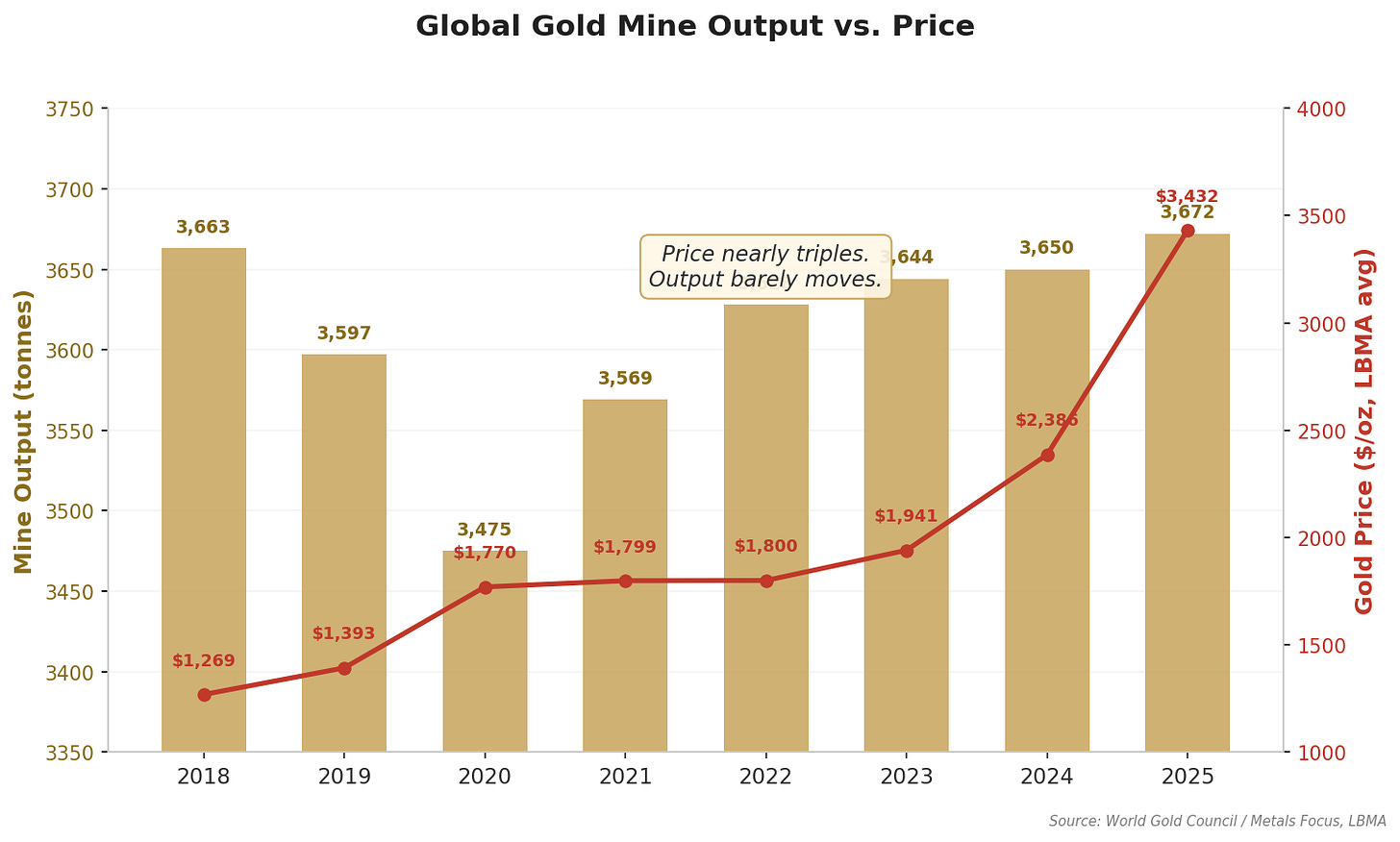

And gold also plays a factor. Central bank demand for gold in 2022 shot up 152% year-over-year from 2021. Now, gold accounts for 15% of central bank reserves.

That’s about 35% higher than it was five years ago when it sat at 11%. In the process, it has displaced 4% of reserves that used to be in U.S. dollars.

And another threat to the dollar is now emerging, too.

The Latest Kindling to the De-Dollarization Fire

Last month, Indonesia announced that it was creating a National Task Force for Local Currency Transactions.

Indonesia said the move was to support its ability to complete international transactions. It was also to promote the use of its local currency, the rupiah.

While that’s true, this announcement doesn’t just impact Indonesia.

You see, in May, Southeast Asian government leaders agreed to use their local currencies in regional transactions. The idea was that this could strengthen economic relationships within the whole region.

And this decision has global currency implications, especially against the dollar.

Southeast Asian regional central banks are taking steps toward de-dollarization. Indonesia’s central bank recently signed agreements with Malaysia and Thailand to use their local currencies in transactions with each other.

Indonesia inked similar local currency transaction deals with Japan and China. It’s also actively working on deals with Singapore and South Korea.

So, on the surface, Indonesia’s latest move might be the story of a country looking out for its own interests.

But it goes much deeper than that on the global stage.

Sidestepping the Dollar Is a Megatrend

Countries like India, China, Brazil, and Malaysia are all setting up trade channels using non-dollar currencies. Their leaders are increasingly forging ways to trade directly with each other in their local currencies.

For instance, China is paying for oil and other commodities from Russia in yuan instead of U.S. dollars. And it’s pushing for currency trade deals with Saudi Arabia and Brazil.

There’s a trend of cutting the U.S. dollar out of the equation. And it’s a sign of BRICS countries’ growing dependence on fellow BRICS and other emerging market powers.

From 2015 to 2022, BRICS imports from other emerging market countries grew from 30% to 34%.

Over the same period, BRICS exports to other emerging market countries grew from 28% to 32%.

These may seem like small changes. But they do show a pattern of broadening trade within the greater BRICS and emerging market bloc of countries.

If you couple this growing trade amongst the BRICS and emerging market bloc… With more of that trade done in non-U.S. dollar currencies… It marks an undeniable shift away from the dollar.

Every new deal struck between countries that once traded exclusively in dollars to trade in other currencies chips away at the global dominance of the U.S. dollar.

That’s the math of it. And it’s no small footprint, either.

The BRICS+ account for nearly half the global population and one-quarter of global GDP. And it’s gaining more economic ground.

That’s because six new countries will enter the BRICS by January 2024: Iran, Saudi Arabia, the United Arab Emirates, Argentina, Egypt, and Ethiopia.

And while the move seems unlikely, government leaders from the BRICS bloc are discussing a possible unified currency. Think of the euro but for the BRICS.

It could even take the form of a unified central bank digital currency (CBDC) or be backed by gold.

We don’t know yet what it would look like. But we do know one thing: The push to displace the dollar is happening.

And, as I wrote last week, all of this signals a weakened trend for the dollar’s use overall.

More By This Author:

This Payment System Is a Trojan Horse For CBDCs

The Fed Created This Financial Frankenstein’s Monster

“Death Of The Dollar” Isn’t Just Hype Anymore

Comments

Log in or sign up to join the conversation.