Image source: Pixabay

We expect the European Central Bank to pause this week after inflation slowed, rates spiked and new geopolitical risks emerged. The Governing Council may limit offering rate guidance to markets and shift the focus to non-rate monetary policy tools. Ultimately, the market impact is set to be relatively contained

The European Central Bank will, for once, face almost a no-brainer this month and keep rates unchanged, as we discuss in our preview. Inflation slowed more than expected in September, bond yields have jumped, and new sources of geopolitical risk will weigh on the growth outlook. Higher oil prices may delay the return to 2% inflation beyond the end of 2025, but that is likely a concern for December when new staff projections will be released.

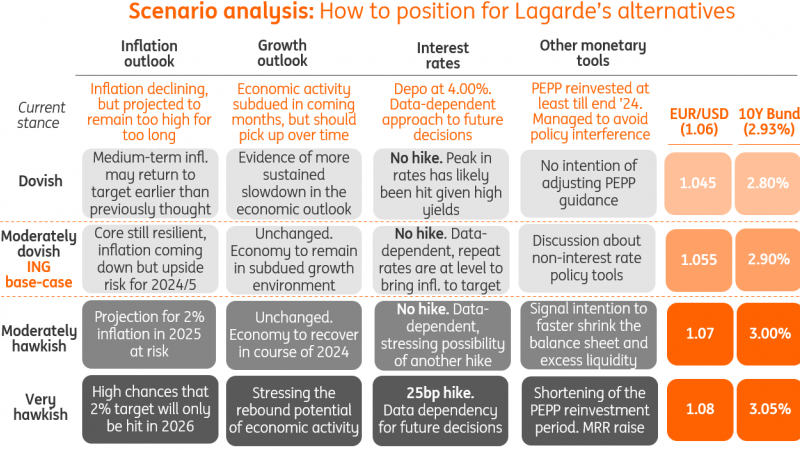

A dovish tilt in the ECB’s communication already happened, at least in the eyes of the market, at the September policy meeting. However, in the days after that meeting, ECB officials tried to sound more hawkish, stressing that the end of rate hikes had not necessarily been reached. Next week, President Christine Lagarde and her Governing Council (GC) members will have to take stock of the market’s repricing of rate expectations as well as recent geopolitical events and data - both dovish arguments - this month.

The ECB, like other central banks, is in a position where its rate cycle is probably over. But it’s still in its interest, barring a substantial dovish shift in the GC equilibrium, to keep bond yields elevated, so allowing the additional tightening to put further pressure on prices. That requires a hawkish tone to be reiterated at this meeting and could also motivate the ECB to hint at an earlier end to reinvestments under the PEPP.

However, missteps have not been uncommon in recent attempts by the bank to provide rate guidance to markets and this time, the Governing Council and President Lagarde may prefer to shift the focus to the discussion on non-rate policy tools, refraining from offering any further detailed guidance on the path of interest rates. These tools include minimum reserves, reversed tiering, and a possible earlier unwinding of the PEPP bond purchase programme.

Ultimately, a “less is more” approach when it comes to discussing rates may be the preferred – and more efficient – path for the ECB this time.

Rates: Preparing to move on from the rates tool to increase policy reach

Markets have largely embraced the ECB’s message that policy rates have reached sufficiently high levels to bring inflation back to target if held long for enough.

The market is discounting only a roughly 10% chance for another hike around the end of 2023 and is fully discounting a 25bp rate cut for July next year. Clearly, the danger is that energy prices have raised the upside risks to the projected inflation path, and some hawkish ECB members might even think a summer rate cut is too early; recall Klaas Knot assumes rates will likely stay at current levels for a year.

Bringing the focus of discussions back to the ECB’s balance sheet might be a possibility to maintain a hawkish posture and prevent the market from pricing cuts too early. However, this will also have to be balanced against the growing concerns surrounding sovereign spreads and Italy in particular. Taken by itself, the ECB continuing to attach greater weight to inflation upside risks rather than downside risks to growth could mean a bear-flattering impetus, especially in a generally more fragile risk environment.

That said, the ECB operates in an environment with greater spill-over effects in markets from a surprisingly resilient US economy. When the ECB assesses current financial conditions, it will likely note that while shorter-dated real rates have fallen below their average since July, longer real rates are still at relatively high levels, given the upward pull from US rates. Less resilient and now more exposed to geopolitical risks, the EUR curve might hold less steepening potential than its counterpart. That's something we also see in the widening of the 10Y UST/Bund spread to around 200bp.

FX: Data remains more important than ECB communication

EUR/USD has continued to find good support despite US 10-year yields reaching 5% and risk sentiment staying unstable. The EUR-USD 2-year swap rate differential has remained wide, at -120bp, on the back of delayed prospects of Fed easing. The impact of ECB communication on this differential is generally less significant compared to that of the Fed, and given our expectations for a cautious tone at this meeting with limited guidance provided, we don’t expect material spillovers into FX this month.

We suspect that a good portion of recent EUR/USD resilience is due to the dollar’s overbought status and some positioning readjustments. The pair appears to be trading on the expensive side, considering hyper-attractive USD rates, growth differentials and geopolitical risks. While it’s true that markets have priced out ECB tightening, we discuss above how a hawkish surprise won’t be easy to achieve in the current environment. A rebound in eurozone data would do much more than an attempt to signal more tightening by the ECB, but that is not our base case for now.

We expect EUR/USD to hover around 1.05/1.06 into and after the ECB meeting. The dollar leg and geopolitical events may well have a bigger say in guiding any short-term trend.

More By This Author:

European Taxonomy: Now The Banking Sector Gears Up For More DisclosuresFX Daily: Growth Differentials On Show This Week

The Commodities Feed: Geopolitical Risks Linger

Comments

Log in or sign up to join the conversation.