Not Your Grandfather's Trade War: The Revenge Of Bad Money, Part 1

With his China Trade Wars tweet this AM, the Donald has proved once again that he has an uncanny ability to get to the heart of matters....even if by sheer accident!

Yet he's right.The trade war was "lost many years ago" and it's the reason Flyover America has rallied to his bluster and bombast on imports and the nefarious practices of furin guberments:

We are not in a trade war with China, that war was lost many years ago by the foolish, or incompetent, people who represented the U.S. Now we have a Trade Deficit of $500 Billion a year, with Intellectual Property Theft of another $300 Billion. We cannot let this continue!

But, alas, the "foolish or incompetent people" skewered in the Donald's 7:22 AM tweet are not some defunct Commerce Department or USTR officials from bygone times.

Nope, it's not pointy-head trade bureaucrats at all. The actual culprits are the "low interest" men and women resident in the Eccles Building, who over the past three decades have transformed the Fed into a Bubble Finance machine and the main street economy into a hollowed out tower of debt.

In a manner of speaking, free money has trumped free trade. And that means what is aborning is not your grandfather's garden-variety trade war; it's the abiding revenge of bad money-----a debilitating affliction that cannot be bargained away by cooler heads among professional trade negotiators as the dip buyers are so foolishly betting again today.

The truth is, the Red Ponzi is an absolute freak of economic nature that has laid waste to much of the US industrial economy. But the dark secret unbeknownst to the Donald, and the Wall Street/Washington establishment alike is that the China monster was enabled, fostered and feed by the US central bank's pursuit of an upside-down monetary policy after 1987.

The turning point came when Mr. Deng concluded that Mao had been wrong about the source of state power: Rather than emanating from the barrel of a gun, as the Great Helmsman had insisted, Deng Xiaoping ordered a 60% depreciation of the yuan, thereby recognizing the far greater efficacy of the credit power that issued from the end of the central bank's printing press.

Then and there the die was cast. Faced with world history's greatest mercantilist export campaign and the draining of China's vast rice paddies of tens of millions of cheap workers to fill Mr. Deng shiny new export factories, the US economy required one thing above all: Namely, a systematic deflation of its bloated price, wage and cost structure; high interest rates to dampen consumption and encourage savings; and sustained supra-historical levels of investment in plant, equipment and technology to equip American workers with an insuperable edge in tools and labor productivity.

Needless to say, Greenspanian money-pumping, soaring debt and wealth effects driven financialization were not merely the opposite of what a regime of sound money would have generated; they were the kiss of death for jobs, prosperity, and hope in Flyover America, as the chart below so dramatically illustrates.

Folks, this chart is not the fruit of Adam Smith's unseen hand of free trade going about the work of the economic gods. China's monthly exports to the US of just $490 million in November 1987 did not explode by 98X over the next 30 years to $48.2 billion in November 2017 owing to comparative advantage!

Indeed, the chart below would not have happened in 10,000 years under a regime of sound money and honest price discovery in the capital markets. To the contrary, China's initial advantage in cheap labor would have led to a large inflow of reserve assets (e.g. gold) to China and a large outflow from the US, causing wage and cost inflation in China and deflation in the US.

Stated differently, when coupled with sound money, the free market is not suicidal. Instead, current account imbalances get settled via the movement of true reserve assets. That settlement process, in turn, causes domestic interest rates to fall and credit to expand in the case of inflows, and the opposite to occur in the case of persistent trade deficits and reserve asset outflows.

At length, domestic prices, costs and wages clear at sustainable levels and current accounts remain in reasonable equilibrium among trading partners over the longer run. By contrast, the purple peak in the upper right hand of the chart below represents a 17% compound annual rate of growth for thirty years running; it's the work of free money, not the free market.

Nevertheless, the so-called "free traders" of the mainstream media are out in force today lamenting the Donald's purported economic ignorance. When it comes to cardinal intellectual error, however, we are not sure which is worse as between the Donald's 17th-century mercantilism or a bit of undiluted tommyrot we heard this morning from CNBC's in-house Wall Street shill, Steve Liesman.

Not to worry about giant trade deficits or a 98X growth in imports from China, he opined, because it's actually a sign of success.

"When we get wealthier we buy everything made here and then add some more from abroad".

Not so fast, we'd say. Liesman was talking about the kind of transient paper wealth that is measured by multiplying billions of equity shares by their fantastically inflated prices. As we have learned twice already this century, however, that kind of wealth can plunge by 50% or more in a relative heartbeat when the Fed's serial financial bubbles finally collapse under their own weight.

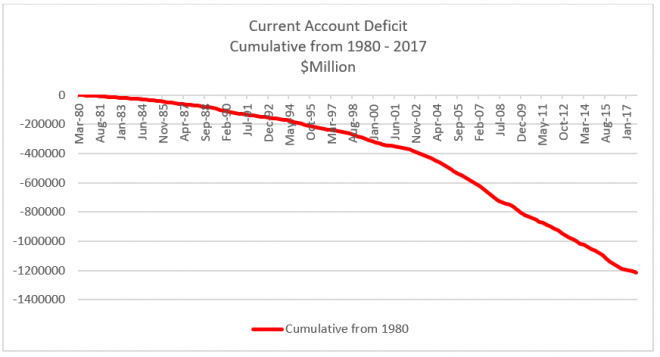

The truth of the matter, of course, is that the above chart for China is not an aberration; it's only the poster child for the underlying economic rot that has been induced by bad money. As we will demonstrate in the balance of this series, the chart below for total US trade (including both goods and services) has been enabled by a central bank driven monetary inflation that has nothing to do with sustainable wealth at all.

In a word, the Fed printed---so they printed. We are referring to virtually every other major central bank in the world, and the mercantilist disease that has spread to all four corners of the planet.

Under this baleful regime, statist rulers and politicians everywhere have empowered their central banks to swap the resources of their lands (the petro-states and resource countries) and the sweat of their workers brows (China, India and like EMs) for US dollar liabilities (US Treasury debt and GSEs) in a misguided and futile effort to protect their export-based prosperity.

In the middle term, of course, this enabled the US to pull off one of the greatest heists in economic history. We issued debt in fantastic abundance and traded it for their goods and services. Since 1980 this heist has accumulated to $12.5 trillion of consecutive current account deficits; and when you inflate those historic dollars to present purchasing power, the total is more like $19 trillion.

That's right. The US has essentially borrowed the entirety of its current GDP from the rest of the world in order to temporarily live high on the hog.

Needless to say, this doesn't bother the Liesman's of the world one bit because today's Wall Street casino is basically a historic and agnostic when it comes to the fundamentals of sound money and finance. In their benighted Keynesian framework, the central bank is always making the future better and stock prices are therefore always going higher---and that's all that matters. Period.

So, apparently, even 30 years of going to hell in a hand-basket on the current account is of small moment, and if noted at all, it gives rise to entirely asinine rationalizations like the Liesman gem quoted above.

Of course, the latter belongs to the same category of pettifoggery as they perennial sell-side claim that any sharp drop in the stock market is a welcome purge of weak hands; or the astounding statement today by St. Louis Fed president, James Bullard , that no more interest hikes are needed because the Fed is already at the "neutral rate".

That's right. At today's 1.62%, the Fed funds rate is negative after LTM inflation of 2.2%. Then again, if we can have giant, consecutive current account deficits forever, why not negative real interest rates in perpetuity, too?

The point, however, goes far beyond the truth of Herb Stein's famous observation that unsustainable trends tend to stop. In this case, in fact, it appears that the economics of stopping unsustainable trade deficits are getting some help from America's most unlikely politician, who saw the resulting hurt in Rust Belt America and proceeded to rub it raw via endless recitation of his long-standing "bad trade deals" trope.

Now that the Donald is attempting to dose the patient with his protectionist patent medicine, however, something more than the unsustainability of $19 trillion in current account deficits is coming to the fore. Namely, the futility of tit-for-tat tariffs in a global context where the underlying economic foundation has been everywhere deformed.

That deformation is obvious enough on the US side of the equation. Real median household income has not increased by one dime since 1999, and at barely 0.25% per year since 1989 shortly after the Greenspan era of Bubble Finance incepted.

In part 2, we will address how the Fed's destructive pursuit of 2.00% inflation has fostered this lamentable outcome, and how its transformation of the equity and other capital markets into gambling arenas has generated rampant financial engineering in the C-suites of corporate America and the effective de-capitalization of main street.

But the ultimate deformation lies in the Red Ponzi, which is inherently an economic powder keg looking for a match.

In fact, as a freakish product of 30 years of bad money it is the very opposite of the preposterous Wall Street/Washington presumption that it's just another really big economy that overdid the "growth" thing; and which is now looking to Beijing's firm hand to effect a smooth transition. That is, an orderly migration from a manufacturing, export and fixed investment boom-land to a pleasant new regime of shopping, motoring, and mass consumption.

Would that it could. But China is not a $12 trillion growth miracle with transition challenges; it is a quasi-totalitarian nation gone mad digging, building, borrowing, spending and speculating in a magnitude that has no historical parallel.

So doing, it has fashioned itself into an incendiary volcano of unpayable debt and wasteful, crazy-ass overinvestment in everything. It cannot be slowed, stabilized or transitioned by edicts and new plans from the comrades in Beijing. It is the greatest economic trainwreck in human history barreling toward a bridgeless chasm.

And that's what makes Wall Street's current assumption that the Donald's trade war is nothing to sweat about so stunningly insensible.

Indeed, the notion that today's dueling tariffs will be compromised out in some grand global crony capitalist style settlement is not only dead wrong; it's completely oblivious to the rotting economic foundations that got us here.

Stated differently, the burned-out industrial precincts of Pennsylvania, Ohio, Michigan, Wisconsin and Iowa may well have chosen the Donald to huff and puff about trade deficits, but in so doing they have also brought into the line of fire the entire bad money regime that underlies the unsustainable globalist order.

If China goes down hard the global economy cannot avoid a thundering financial and macroeconomic dislocation. And not just because China accounts for 17% of the world's $80 trillion of GDP or that it has been the planet's growth engine most of this century.

As we have indicated, China is the rotten epicenter of the world's three-decade long plunge into an immense central bank fostered monetary fraud and credit explosion that has deformed and destabilized the very warp and woof of the global economy.

As further indicated above, China's financial madness has gone to an unfathomable extreme because in the early 1990s a desperate oligarchy of despots who ruled with machine guns discovered a better means to stay in power. That is, the printing press in the basement of the PBOC----and just in the nick of time (for them).

Print they did. Buying in dollars, euros, and other currencies hand-over-fist in order to peg their own money and lubricate Mr. Deng's export factories, the PBOC expanded its balance sheet from $40 billion to $4 trillion during the course of a mere two decades.

That's 100X and there is nothing like that in the history of central banking-----nor even in economists' most febrile imagings about its possibilities.

The PBOC's red-hot printing press, in turn, emitted high-powered credit fuel. In the mid-1990s China had about $500 billion of public and private credit outstanding---hardly 1.0X its rickety GDP. Today that number is $40 trillion or even more.

Yet nothing in this economic world (or the next) can grow at 80X in only 20 years and live to tell about it. Most especially, not in a system built on a tissue of top-down edicts, illusions, lies and impossibilities, and which sports not even a semblance of financial discipline, political accountability or free public speech.

To wit, China is a witches brew of Keynes and Lenin. It's the financial tempest which will slam the world's great bloated edifice of central bank fostered faux prosperity.

So the right approach to the horrible danger now at hand is not to dissect the dueling tariff lists to guess which tit will be traded for what tat.

Instead, it is time to recognize that the Red Suzerains of Beijing have built a Potemkin Village. But since they actually believe it's real, they do not have even a passing acquaintanceship with the requisites and routines of a real capitalist economy.

Ever since the aging oligarch(s) who run China were delivered from Mao's hideous dystopia by Mr. Deng's chance discovery of printing press prosperity, they have lived in an ever-expanding bubble that is so economically unreal that it would make the Truman Show envious. Any rulers with even a modicum of economic literacy would have recognized long ago that the Chinese economy is booby-trapped everywhere with waste, excess and unsustainability.

Here is but one example. Somewhere near Shanghai some credit-crazed developers built a replica of the Pentagon on 100 acres of land. This was not intended as a build-to-lease deal with the PLA (People's Liberation Army); its a shopping mall that apparently has no tenants and no customers!

Projects like the above-----and China is crawling with them-----are a screaming marker of an economic doomsday machine. They bespoke an inherently unsustainable and unstable simulacrum of capitalism where the purpose of credit is to fund state-mandated GDP quota's, not finance efficient investments with calculable risks and returns.

Accordingly, the outward forms of capitalism are belied by the substance of statist control and central planning. For example, there is no legitimate banking system in China---just giant state bureaus which are effectively run by party operatives.

Their modus operandi amounts to parceling out quotas for national GDP and credit growth from the top, and then water-falling them down a vast chain of command to the counties, townships and villages below. There have never been any legitimate financial prices in China---all interest rates and FX rates have been pegged and regulated to the decimal point; nor has there ever been any honest financial accounting either----loans have been perpetual options to extend and pretend.

And, needless to say, there is no system of financial discipline based on contract law. China's GDP has grown by $11 trillion dollars during this century alone-------that is, there has been a boom across the land that makes the California gold rush appear pastoral by comparison.

Yet in all that frenzied prospecting there have been almost no mistakes, busted camps, empty pans or even personal bankruptcies. When something has occasionally gone wrong with an "investment" the prospectors have gathered in noisy crowds on the streets and pounded their pans for relief----a courtesy that the regime has invariably granted.

Indeed, the Red Ponzi makes Wall Street look like an ethical improvement society. Developers there built an entire $50 billion replica of Manhattan Island near the port city of Tianjin----- complete with its own Rockefeller Center and Twin Towers----- but have neglected to tell investors that no one lives there. Not even bankers!

Stated differently, even at the peak of recent financial bubbles in London, NYC, Miami or Houston they did not build such monuments to sheer economic waste and capital destruction. But just consider the case of China's mammoth steel industry.

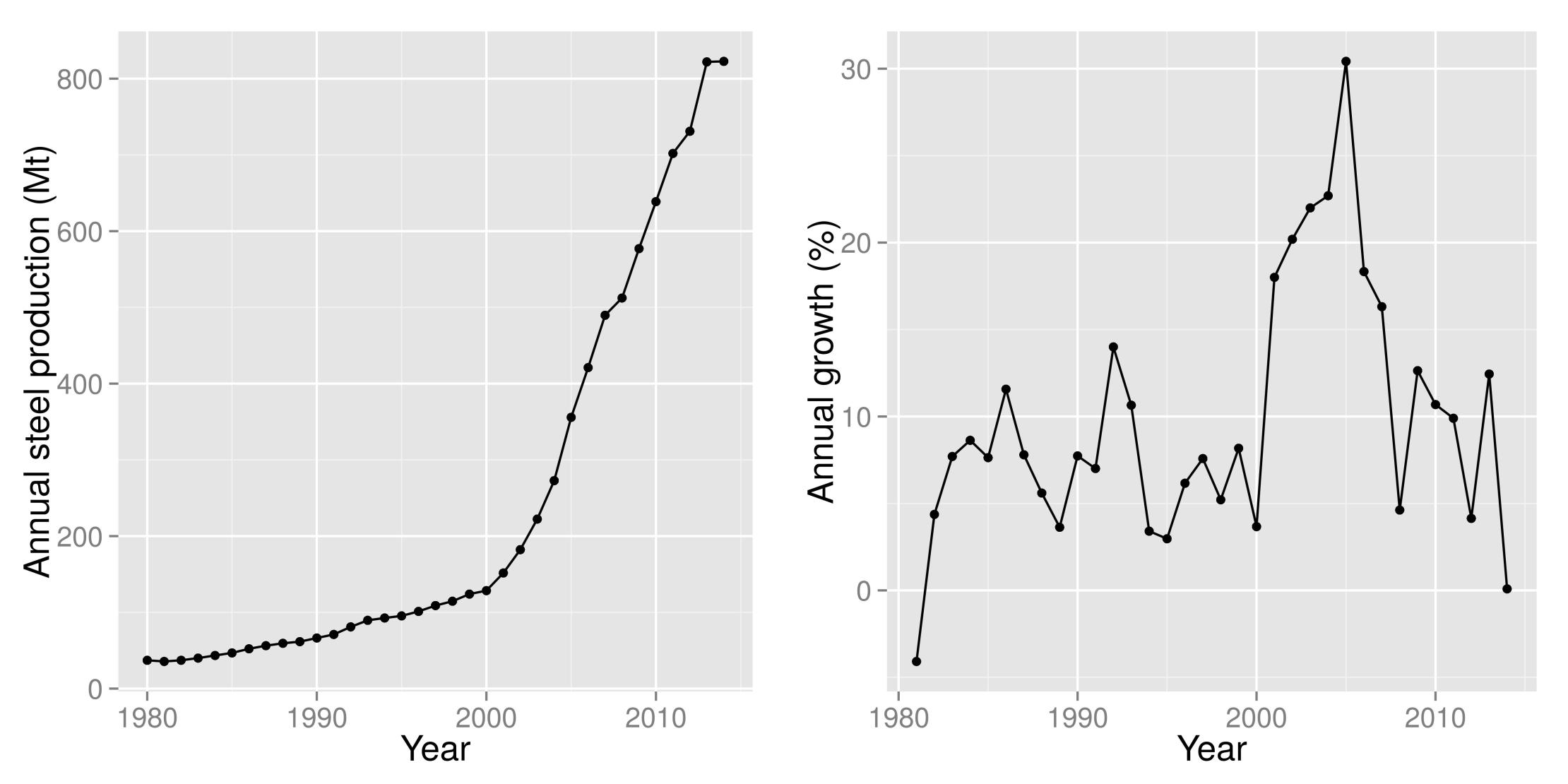

It grew from about 70 million tons of production in the early 1990s to 832 million tons in 2017. Beyond that, the capacity build-out behind the chart below tells the full story.

To wit, Beijing’s tsunami of cheap credit enabled China’s state-owned steel companies to build new capacity at an even more fevered pace than the breakneck growth of annual production. Consequently, annual crude steel capacity now stands at nearly 1.3 billion tons, and nearly all of that capacity----about 65% of the world total------ was built in the last ten years.

Needless to say, it's a sheer impossibility to expand efficiently the heaviest of heavy industries by 17Xin a quarter century.

This means that China’s aberrationally massive steel industry expansion created a significant increment of demand for its own products.

That is, demand for plate, structural and other steel shapes that go into blast furnaces, BOF works, rolling mills, fabrication plants, iron ore loading and storage facilities, as well as into plate and other steel products for shipyards where new bulk carriers were built and into the massive equipment and infrastructure used at the iron ore mines and ports.

That is to say, the Chinese steel industry has been chasing its own tail, but the merry-go-round has now stopped, and with the completion of the Mr. Xi's coronation last fall the last burst of Potemkin construction is being ground to a halt.

The fact is, China will be lucky to have 500 million tons of true sell-through demand----that is, on-going domestic demand for sheet steel to go into cars and appliances and for rebar and structural steel to be used in replacement construction once the current one-time building binge finally expires. That's just 40% of its massive capacity investment.

And it is also evident that it will not be in a position to dump its massive surplus on the rest of the world. Indeed, that threat is at the very heart of the Donald's incipient trade war, which started with the 25% steel tariffs a few weeks ago.

What the trade war really means is that China has upwards of a half-billion tons of excess capacity that will crush prices and profits, but, more importantly, that the one-time steel demand for steel industry CapEx is over and done. And that means shipyards and mining equipment, too.

These are not simply gee whiz comparisons. It took the fastidious Japanese nearly five decades to erect the world's leading 120 million ton steel industry on the back of tens of thousands of step-by-step engineering and operational improvements. China created the same tonnage each and every year after the financial crisis, but it was all based just on a great field of dreams exercise in pell-mell expansion. Efficiency, longevity and steel-making technique were hardly an afterthought.

Nor is its own tail the only loss of market demand. Even more fantastic than steel has been the growth of China’s auto production capacity. In 1994, China produced about 1.4 million units of what were bare bones communist era cars and trucks. Last year it produced more than 29 million mostly western style vehicles or 21X more.

And, yes, that wasn’t the half of it. China has gone nuts building auto plants and distribution infrastructure. It is currently estimated to have upwards of 35 million units of vehicle production capacity. But demand has actually rolled over this year and will continue heading lower after temporary government tax gimmicks—– that are simply pulling forward future sales—–expire.

The more important point, however, is that as the China credit Ponzi grinds to a halt, it will not be building new auto capacity for years to come. It is now drowning in excess capacity, and as prices and profits plunge in the years ahead the auto industry CapEx spigot will be slammed shut, too.

Needless to say, this not only means that consumption of structural steel and rebar for new auto plants will plunge. It also will result in a drastic reduction in demand for the sophisticated German machine tools and automation equipment needed to actually build cars.

Stated differently, the CapEx depression which has been underway for several years in China, Australia, Brazil and much of the EM will ricochet across the global economy. Cheap credit and mispriced capital are truly the father of a thousand economic sins.

China’s construction infrastructure, for example, is grotesquely overbuilt------ from cement kilns, to construction equipment manufacturers and distributors, to sand and gravel movers, to construction site vendors of every stripe.

For crying out loud, in three recent year China used more cement than did the United States during the entire 20th century!

That is not indicative of a just a giddy boom; its evidence of a system that has gone mad digging, hauling, staging and constructing because there was unlimited credit available to finance the outpouring of China’s runaway construction machine.

The same is true for its machinery, solar and aluminum industries---to say nothing of 70 million empty luxury apartments and vast stretches of over-built highways, fast rail, airports, shopping mails and new cities.

In short, the flip-side of the China's giant credit bubble is the most massive malinvestment of real economic resources----labor, raw materials and capital goods---ever known.

Effectively, the country-side pig sties have been piled high with copper inventories and the urban neighborhoods with glass, cement and rebar erections that can't possibly earn an economic return. Yet all of these assets has become "collateral" for even more "loans" under the Chinese Ponzi.

China has been on a wild tear heading straight for the economic edge of the planet----that is, monetary Terra Incognito---based on the circular principle of borrowing, building, and borrowing. In essence, it is a giant re-hypothecation scheme where every man's "debt" become the next man's "asset".

Thus, local government's have meager incomes, but vastly bloated debts based on the collateral of stupendously over-valued inventories of land----valuations which were established by earlier debt-financed sales to developers.

Likewise, coal mine entrepreneurs face not only collapsing prices and revenues but also soaring double-digit interest rates on shadow banking loans collateralized by over-valued coal reserves. Shipyards have empty order books, but vast debts collateralized by soon to be idle construction bays. Speculators have collateralized massive stockpiles of copper and iron ore at prices that are on the way to becoming ancient history.

So China is indeed the greatest Ponzi scheme in recorded history. And it is that house of cards that the Donald has now frontally attacked.

More hideous still, it is that house of cards that the robo-machines brought with malice aforethought this afternoon, reversing the Dow's overnight drop by nearly 750 points.

Bad money has rarely been so insouciant; the revenge never so certain.