Not A Unique Equity Market: Higher Prices Ahead?

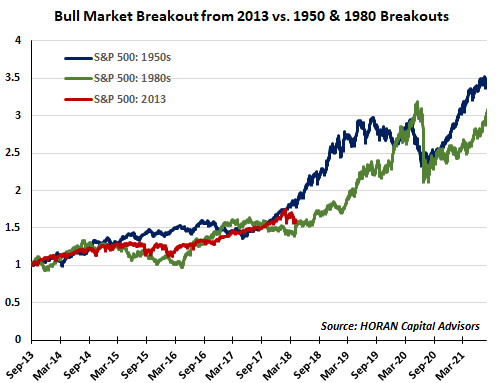

About a year and a half ago I wrote a post on the current equity market that broke out of a thirteen year trading range in 2013 and compared it to the bull markets of the 1950s and 1980s. A number of policy issues being pursued today have similarities to ones in those two decades and below is a brief summary of what I wrote then:

"...potential commonality to the current market compared to those prior decades related to policy decisions coming out of Washington, D.C. In the 1950's the Gross National Product in the U.S. more than double from 1945 to 1960. Government spending in the 1950's was targeted at construction of the interstate highway system, building of schools and an increase in military spending. In the 1980's President Reagan's policies focused on reducing the tax burden on Americans, lowering government regulation and shrinking government itself. President Elect Donald Trump also projects to implement similar policies, i.e., reduce regulation, shrink the government, increase spending on infrastructure and lower taxes. For investors the question to answer is what market segments worked then and might these same sectors outperform early in a Trump administration."

An update to a chart in that earlier post is shown below and in spite of the size of the 'point' swings in the market today, the path of this current bull market is not unique. If history is any guide, and given similar policies out of Washington as in the 1950's and 1980's, the S&P 500 Index certainly appears to have more room to the upside. In fact, the market maybe nearing a point of a sustained upside move.

(Click on image to enlarge)

One thing investors experienced in the first quarter was a return of volatility to the equity markets, and the bond market for that matter. Wednesday's market was action was a perfect case in point as the Dow Jones Industrial Average traded down over 500 points near the open yet closed up 230 points, a trading range of more than 700 points. The catalyst for the market swing seems to be connected to the discussion around tariffs and the potential negative implications resulting from the tariff negotiations. I stress 'negative' as most of the tariffs have not been instituted, yet it is the unknown that can cause difficulty for the equity markets.

I can list a number of additional potential negative issues with any single one being a headwind for the equity market: rising interest rates and consequent flattening yield curve, growth in deficit spending out of Washington and more. All but the interest rate factor are mainly political events and I would say business fundamentals and economic fundamentals remain more important variables for the market right now. Given some of the negative factors cited, just maybe the market will climb the proverbial wall of worry.

I am not recommending burying one's head in the sand regarding some of these potential headwinds. What is important though is not to place out sized weight on the 'noise' at the expense of underlying fundamentals. Importantly, policies being pursued today have similarities to policies implemented in earlier decades and those policies were bullish for stocks then.

Disclosure: None.