Morning Call For July 7, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.12%) are down -0.06% ahead of Jun ADP employment data later this morning and European stocks are up +1.21%. Energy producing stocks higher as crude oil (CLQ16 +1.08%) is up +0.97% after API data released late yesterday showed U.S. crude stockpiles dropped -6.7 million bbl last week. Increased M&A activity is another positive factor for stocks with Danone up 7% after it agreed to buy WhiteWave Foods for about $10 billion. EUR/USD fell -0.20% and gains in European stocks were limited after German May industrial production unexpectedly declined by the most in 1-3/4 years. Asian stocks settled mixed: Japan -0.67%, Hong Kong +1.03%, China -0.01%, Taiwan +0.76%, Australia +0.59%, Singapore -0.09%, South Korea +1.13%, India +0.13%.

The dollar index (DXY00 -0.02%) is down -0.03%. EUR/USD (^EURUSD) is down -0.20%. USD/JPY (^USDJPY)is down -0.17%.

Sep T-note prices (ZNU16 -0.05%) are unchanged.

German May industrial production unexpectedly fell -1.3% m/m, weaker than expectations of +0.1% m/m and the biggest decline in 1-3/4 years.

UK May industrial production fell -0.5% m/m and rose +1.4% y/y, stronger than expectations of -1.0% m/m and +0.5% y/y.

U.S. STOCK PREVIEW

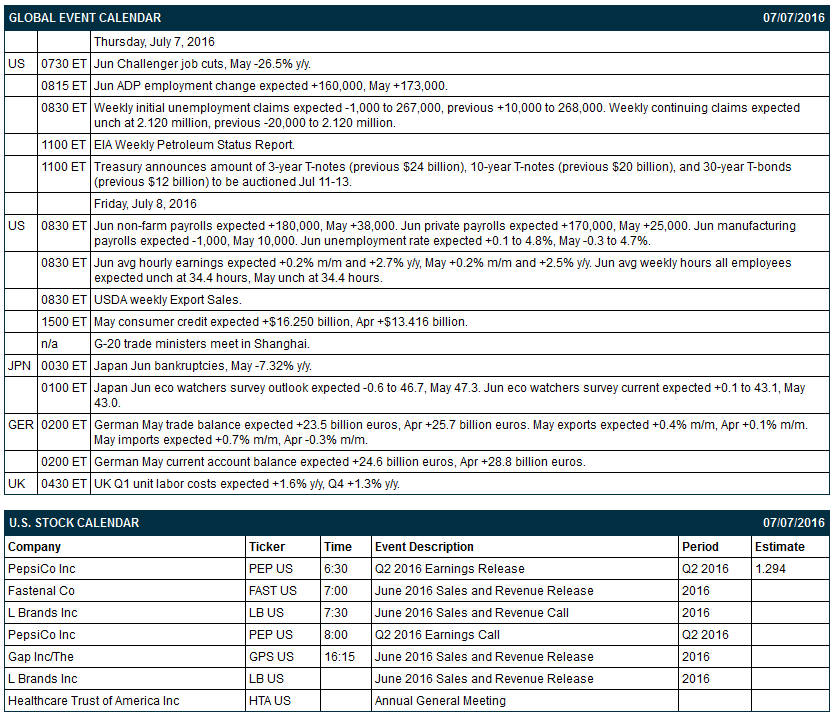

Key U.S. news today includes: (1) Jun Challenger job cuts (May -26.5% y/y), (2) June ADP employment change (expected +160,000, May +173,000), (3) weekly initial unemployment claims (expected -1,000 to 267,000, previous +10,000 to 268,000) and continuing claims (expected unch at 2.120 million, previous 20,000 to 2.120 million), and (4) EIA Weekly Petroleum Status Report.

Russell 1000 companies reporting earnings today: PepsiCo (consensus $1.29).

U.S. IPO's scheduled to price today: none.

Equity conferences this week include: none.

OVERNIGHT U.S. STOCK MOVERS

First Solar (FSLR +2.85%) slipped 3% in pre-market trading after it was downgraded to 'Hold' from 'Buy' at Deutsche Bank.

WhiteWave Foods (WWAV +0.94%) jumped 18% in pre-market trading after Danone agreed to buy the company for about $10 billion.

Endologix (ELGX +2.49%) was upgraded to 'Outperform' from 'Market Perform' at BMO Capital Markets.

Depomed (DEPO +3.79%) was downgraded to 'Neutral' from 'Buy' at UBS.

Red Hat (RHT +1.25%) was downgraded to 'Equalweight' from 'Overweight' at Morgan Stanley.

Pepsico (PEP -0.47%) reported Q2 EPS of $1.35, better than consensus of $1.29.

Plains GP Holdings LP (PSGP unch) was downgraded to 'Hold' from 'Buy' at Evercore ISI.

Seagate Technology (STX +1.55%) gained almost 2% in after-hours trading after the company announced that Mark Long will become CFO in addition to his current role as chief strategy officer.

Time Warner (TWX +0.93%) was rated a new 'Buy' at Brean Capital with a 12-month price target of $90.

Western Digital (WDC +1.65%) climbed nearly 3% in after-hours trading after it reported preliminary Q4 adjusted EPS of 72 cents, above a previous forecast of 65 cents-70 cents.

CBS Corp. (CBS +0.77%) was rated a new 'Buy' at Brean Capital with a 12-month price target of $65.

MARKET COMMENTS

September E-mini S&Ps (ESU16 -0.12%) this morning are down -1.25 ponts (-0.06%). Wedneday's closes: S&P 500 +0.54%, Dow Jones +0.44%, Nasdaq +0.77%. The S&P 500 on Wednesday rebounded from early losses and closed higher on the +3.6 point increase in the U.S. Jun ISM non-manufacturing index to 56.5, stronger than expectations of +0.4 to 53.3 and the fastest pace of expansion in 7 months. Stocks were also boosted by a rally in drug companies that lifted the health-care sector.

Sep 10-year T-note prices (ZNU16 -0.05%) this morning are unchnaged. Wedneday's closes: TYU6 -7.00. FVU6 -4.25. Sep T-notes on Wednesday fell back from a 3-1/2 year nearest-futures high and closed lower on signs of economic strength after the U.S. Jun ISM non-manufacturing index expanded at the fastest pace in 7 months (+3.6 to 56.5). T-notes were also undercut by reduced safe-haven demand after the S&P 500 rebounded from early losses and moved higher. T-notes found support from carryover support from rallies in German bunds and UK gilts to all-time highs and from dovish comments from Fed Governor Tarullo who said that inflation and unemployment haven't yet reached levels that would justify an interest rate hike.

The dollar index (DXY00 -0.02%) this morning is down -0.032 (-0.03%). EUR/USD (^EURUSD) is down -0.0022 (-0.20%). USD/JPY (^USDJPY) is down -0.17 (-0.17%). Wedneday's closes: Dollar Index -0.113 (-0.12%), EUR/USD +0.0024 (+0.22%), USD/JPY -0.42 (-0.41%). The dollar index on Wednesday fell back from a 1-week high and closed lower on weakness in USD/JPY, which fell to a 1-week low, and on dovish comments from Fed Governor Tarullo who said that inflation and unemployment haven't yet reached levels that would justify an interest rate increase. The dollar index was boosted by weakness in GBP/USD which fell to a fresh 31-year low, and by the stronger-than-expected U.S. Jun ISM non-manufacturing index.

Aug WTI crude oil (CLQ16 +1.08%) this morning is up +46 cents (+0.97%). Aug gasoline (RBQ16 +2.13%) is up +0.0313 (+2.18%). Wedneday's closes: CLQ6 +0.83 (+1.78%), RBQ6 +0.0042 (+0.29%). Aug crude oil and gasoline on Wednesday closed higher as Aug crude recovered from a 1-week low and Aug gasoline rebounded from a 2-3/4 month low. Crude oil prices were boosted by a weaker dollar and by expectations that Thursday's weekly EIA report will show that U.S. crude inventories fell -2.5 million bbl.

(Click on image to enlarge)

Disclosure: None.