Morning Call For Aug. 6, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 -0.26%) this morning are down -0.34% at a 2-month low and European stocks are down -1.41% at a 4-1/2 month low amid escalating tension in Ukraine. The Polish Foreign Ministry said the risk of Russia invading Ukraine has increased in the "last dozen hours or so" after Russian President Putin increased the number of troops on his country's western border. Concern over the European economy is another negative for stocks after German factory orders unexpectedly fell by the most in 2-3/4 years and after Italy Q2 GDP fell -0.2% q/q after falling -0.1% q/q in Q1, which pushes Italy into recession. Asian stocks closed mostly lower: Japan -1.05%, Hong Kong -0.26%, China -0.26%, Taiwan +0.03%, Australia-0.12%, Singapore -0.22%, South Korea -0.38%, India -0.94%. Commodity prices are mixed. Sep crude oil (CLU14 +0.37%) is up +0.21%. Sep gasoline (RBU14 +0.88%) is up +0.71%. Dec gold (GCZ14 +0.41%) is up +0.47%. Sep copper (HGU14 -1.08%) is down -1.11% at a 2-week low. Agriculture and livestock prices are mixed. The dollar index (DXY00 +0.44%) is up +0.43% at a 10-3/4 month high. EUR/USD (^EURUSD) is down-0.25% at an 8-3/4 month low. USD/JPY (^USDJPY) is down -0.22%. Increased safe-haven demand from a slide in stocks has boosted U.S. and German government bonds with Sep T-note prices (ZNU14 +0.20%) up +8.5 ticks at a 2-week high and as the yield on the 10-year German bund fell to 1.100%, the lowest on record.

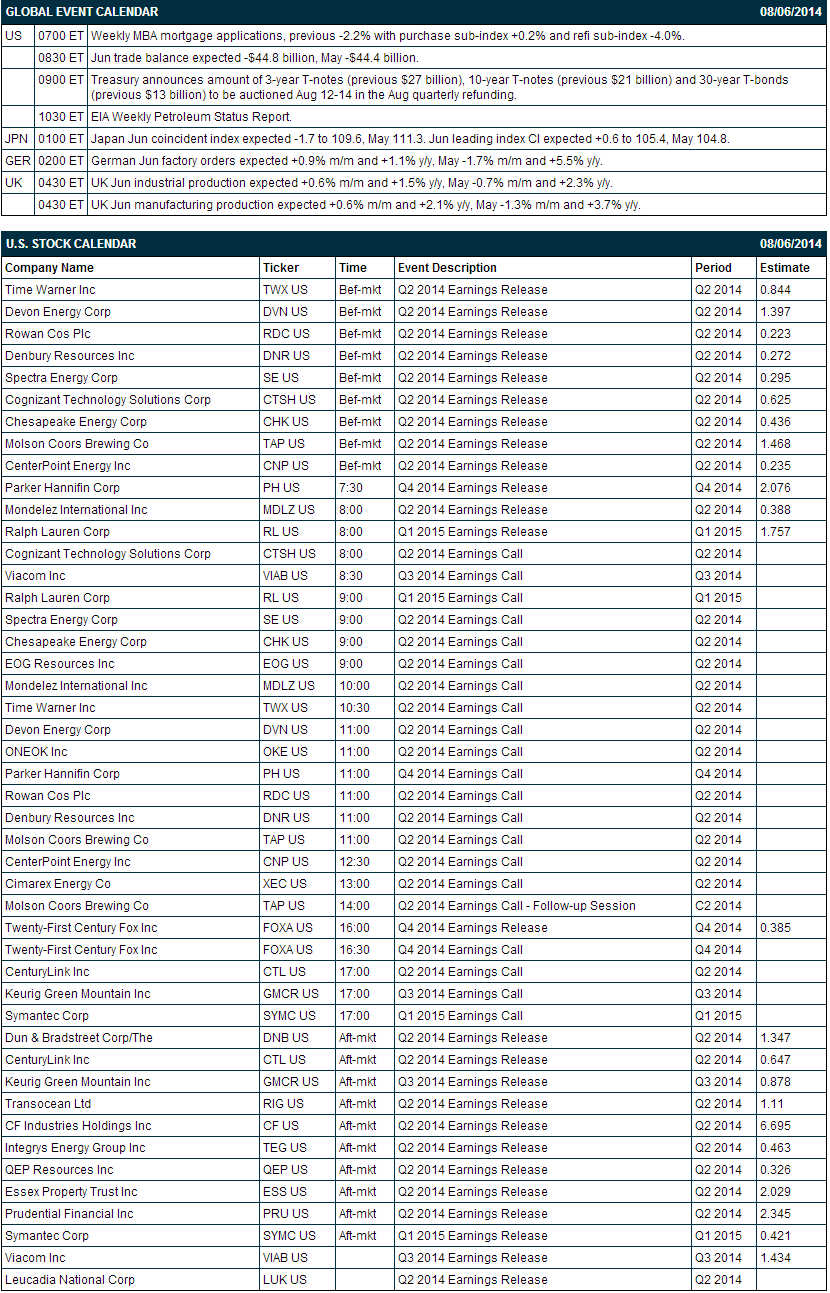

German Jun factory orders unexpectedly fell -3.2% m/m, much weaker than expectations of +0.9% m/m and the largest monthly decline in 2-3/4 years. On an annual basis Jun factory orders fell -2.4%, weaker than expectations of +1.1% y/y.

UK Jun industrial production rose +0.3% m/m and +1.2% y/y, weaker than expectations of +0.6% m/m and +1.5% y/y.

UK Jun manufacturing production rose +0.3% m/m and +1.9% y/y, less than expectations of +0.6% m/m and +2.1% y/y.

UK Jul Halifax house prices rose +1.4% m/m and +10.2% in the three months through Jul, more than expectations of +0.4% m/m and +9.6% in the three months through Jul.

The Japan Jun leading index CI rose +0.7 to 105.5, right on expectations. The Jun coincident index fell -0.9 to 109.4, a larger decline than expectations of -0.7 to 109.6 and the lowest in 10 months.

U.S. STOCK PREVIEW

Today’s U.S. June trade deficit is expected to widen slightly to -$44.8 billion from -$44.4 billion in May. The markets will be watching today’s weekly MBA mortgage apps report for an update on mortgage market activity and the implications for home sales.

There are 47 of the S&P 500 companies that report earnings today with notable reports including: Time Warner (consensus $0.84), Devon Energy (1.40), Molson Coors (1.47), Cheasapeake (0.44), Ralph Lauren (1.76). Equity conferences for the remainder of this week include: CFA Society of Minnesota InvestMNt Conference on Wed, Black Hat USA 2014 on Wed-Thu, Needham Advanced Industrial Technologies Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Sprint (S -1.22%) slumped 17% in pre-market trading after a person with knowledge of the matter said the company ended talks to acquire T-Mobile.

Time Warner (TWX -0.40%) dropped 12% in pre-market trading after 21st Century Fox withdrew its takeover bid for the company.

DISH (DISH -0.45%) reported Q2 EPS of 46 cents, below consensus of 51 cents

Cablevision (CVC -7.04%) was upgraded to 'Neutral' from 'Sell' at Citigroup.

Tesla (TSLA -0.01%) was initiated with an 'Outperform' at Pacific Crest with a price target of $316.

Peugeot (PEUGY +1.45%) was upgraded to 'Neutral' from 'Sell' at Citigroup.

Credit Agricole (CRARY +0.87%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank.

Cerner (CERN -1.45%) will acquire Siemens Health Services (SIEGY -1.38%) for $1.3 billion in cash.

Disney (DIS -0.56%) rose over 1% in after-hours trading after it reported Q3 EPS of $1.28, above consensus of $1.17.

Activision Blizzard (ATVI -1.11%) rose over 3% in after-hours trading after it reported Q2 EPS of 6 cents, three time more than consensus of 2 cents.

Groupon (GRPN +0.71%) sank 17% in after-hours trading after it reported Q2 EPS of 1 cent, right on consensus, but then lowered guidance on Q3 EPS to zero to 2 cents, below consensus of 3 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 -0.26%) this morning are down -6.50 points (-0.34%) at a new 2-month low. The S&P 500 index on Tuesday slumped to a 2-month low and closed lower: S&P 500 -0.97%, Dow Jones -0.84%, Nasdaq -0.87%. Negative factors included (1) concern over escalation of the Ukraine crisis after Poland's Foreign Minister said Russia is amassing troops on the Ukraine border and are poised to invade Ukraine, and (2) Chinese economic concerns after the China HSBC Jul services PMI dropped -3.1 to 50.0, the lowest since the data series began in 2005. Stocks ignored bullish factors that included (1) the Jul ISM non-manufacturing index that rose +2.7 to an 8-1/2 year high of 58.7, and (2) the +1.1% increase in Jun factory orders, stronger than expectations of +0.6%.

Sep 10-year T-notes (ZNU14 +0.20%) this morning are up +8.5 ticks at a 2-week high. Sep 10-year T-note futures prices on Tuesday erased early losses and closed little changed after a slide in stocks boosted safe-haven demand for T-notes. T-notes had been lower most of the day on concern the Fed may hike interest rates sooner-than-expected after Jun factory orders rose more than expected and after the Jul ISM non-manufacturing index expanded at its fastest pace in 8-1/2 years. Closes: TYU4 +0.50, FVU4 -1.25.

The dollar index (DXY00 +0.44%) this morning is up +0.350 (+0.43%) at a 10-3/4 month high. EUR/USD (^EURUSD) is down -0.0034 (-0.25%) at an 8-3/4 month low and USD/JPY (^USDJPY) is down -0.23 (-0.22%). The dollar index on Tuesday jumped to a 10-1/2 month high but fell back on profit taking and closed unchanged. The dollar had moved higher after the larger-than-expected increase in the Jul ISM non-manufacturing index to an 8-1/2 year high and the stronger than expected Jun factory orders added to evidence the U.S. economy is gathering steam. EUR/USD slipped to an 8-3/4 month low as expectations the Fed will tighten monetary policy before the ECB, which boosted the dollar's interest rate differentials against the euro. Closes: Dollar index unch, EUR/USD -0.00458 (-0.34%), USD/JPY +0.026 (+0.03%).

Sep WTI crude oil (CLU14 +0.37%) this morning is up +20 cents (+0.21%) and Sep gasoline (RBU14 +0.88%) is up +0.0192 (+0.71%). Sep crude and gasoline prices on Tuesday closed lower with Sep gasoline at a 6-month low: CLU4 -0.91 (-0.93%), RBU4 -0.0094 (-0.34%). Bearish factors included (1) the rally in the dollar index to a 10-1/2 month high, and (2) concern that the shutdown of the Coffeyville, Kansas, refinery last week will lead to an increase in inventories at Cushing, Oklahoma, the delivery point of WTI futures, when EIA weekly inventory data is released on Wednesday.

Disclosure: None