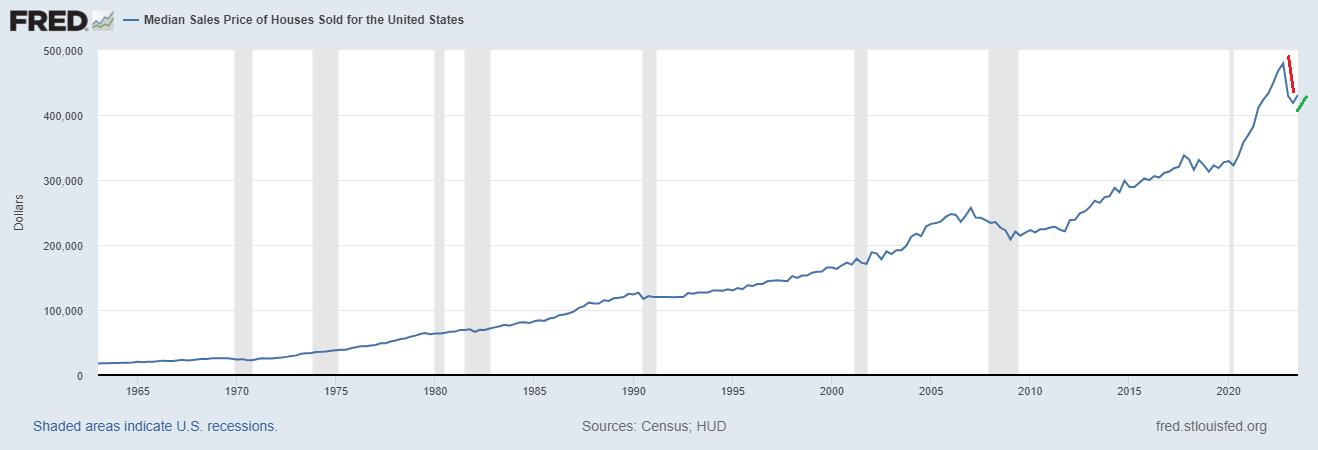

Prices peaked in Oct 2022 and came down about 9% by May 2023. People took advantage of the lower prices and sales went up in the 3rd quarter. As such, prices are up in the 3rd quarter.

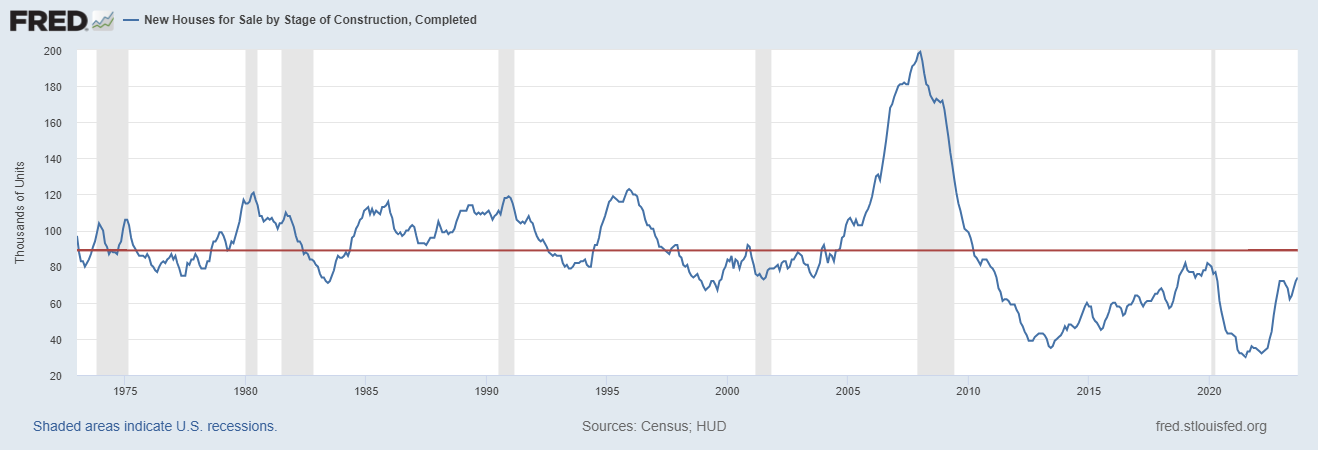

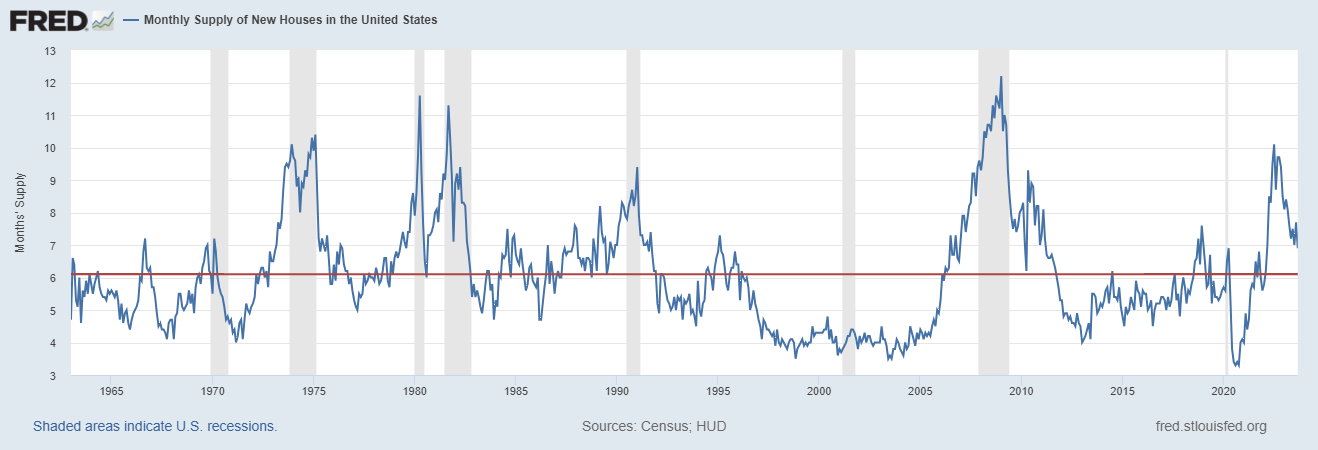

(Click on image to enlarge)

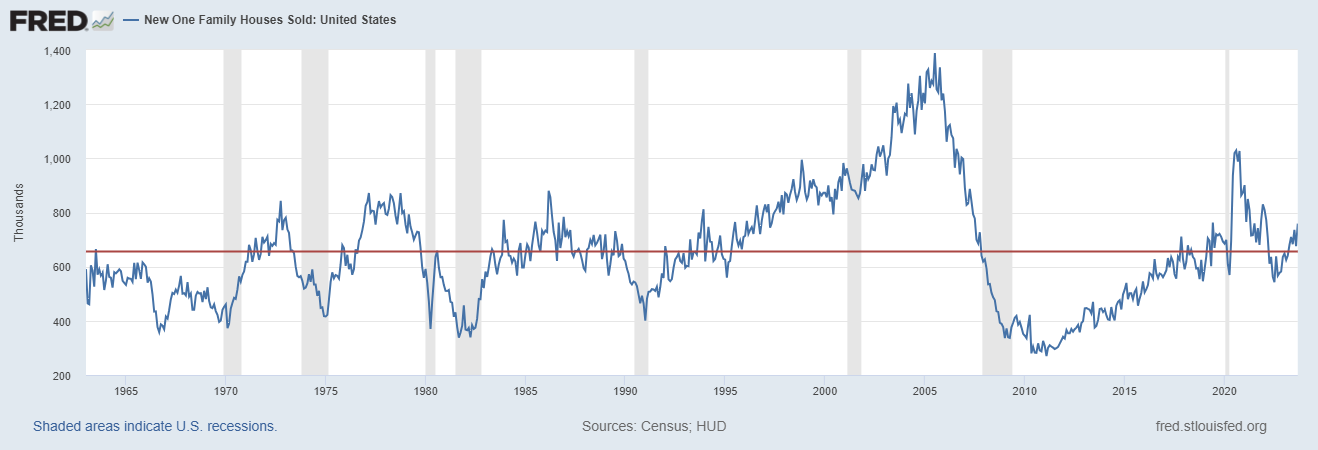

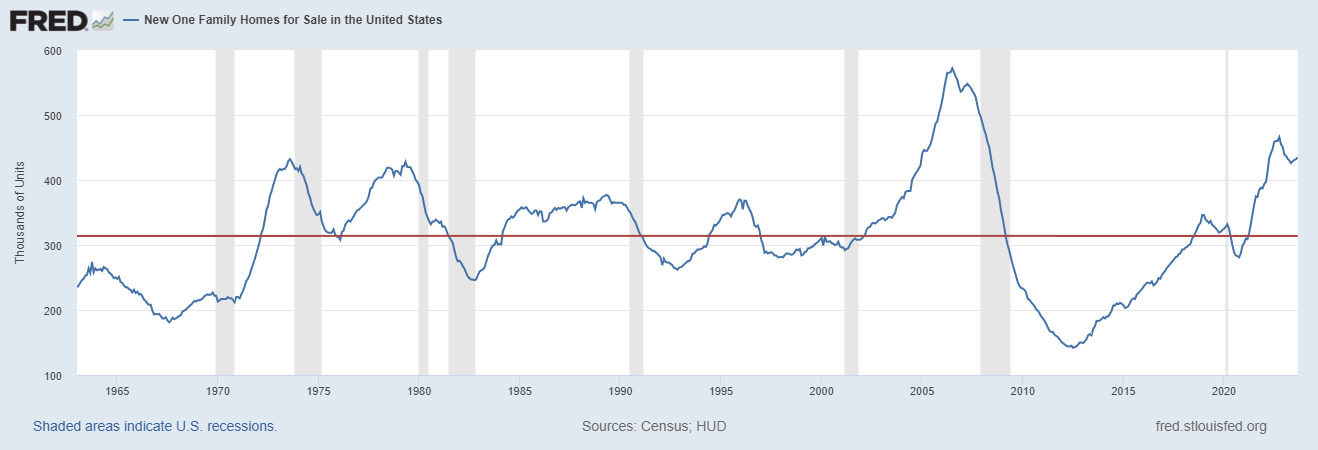

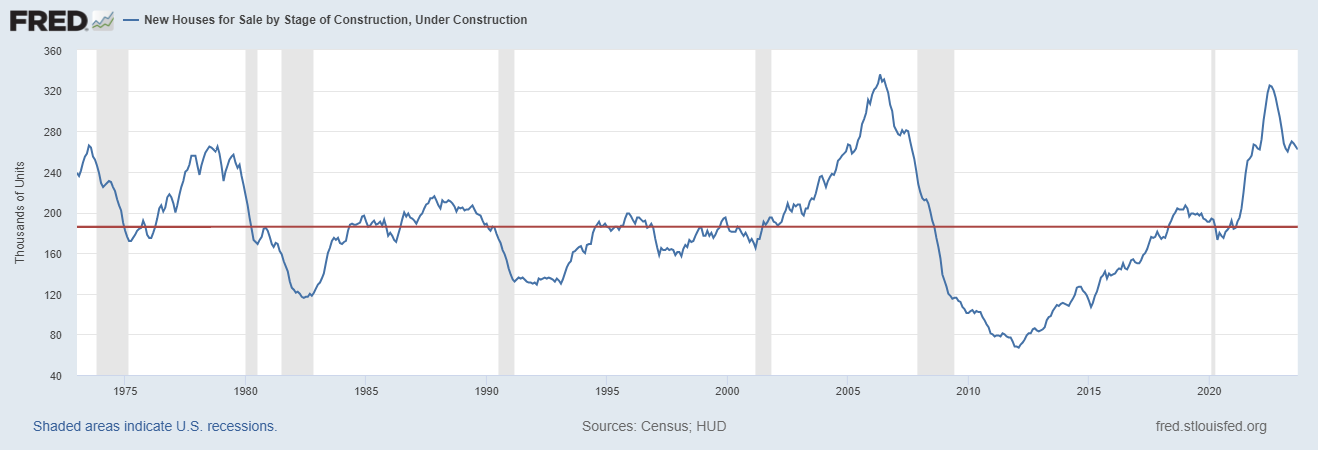

There are about 35% more units for sale than the historic average. About 2/3 of these units are currently under construction. Completed inventory though is currently less than normal.

Conclusions to draw here:

- Units for sale and under construction is elevated but coming down, this means slowing residential construction spending.

- The inventory of houses for sale is higher than the long term average. There are more houses under construction than normal and these will soon be completed. The inventory of completed homes for sale is expected to then to rise to a destination likely higher than historic norms. The elevated inventory of houses just sitting there should again put pressure on prices in the near future.

- There is plenty of inventory, but by no means a glut. This is not currently concerning given the existing home market is having its challenges resulting from the pace of interest rate hikes that is freezing owners into their existing mortgage.

(Click on image to enlarge)

More By This Author:

Macro: Flash PMI — US, EU, Japan, UK, AustraliaSurvey Of Salient Risks To Financial Stability

Fed Financial Stability Report – October 2023 – Summary

Comments

Log in or sign up to join the conversation.