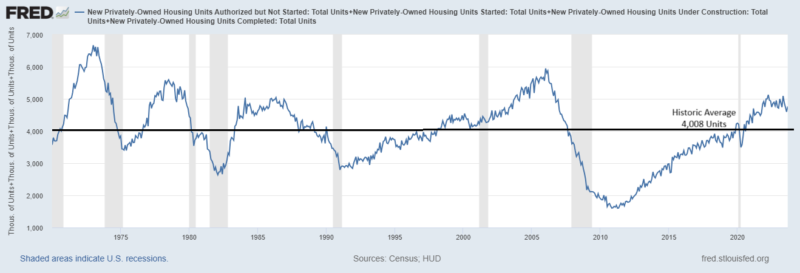

I’ve been reading some lately about all the housing units that are coming to market and the likely hit to house prices and rents that will accompany this supply. Looking at the housing pipeline (Units permitted but not started + Units started + Units under construction + Units completed this month), we are elevated by about 680,000 units on an annualized basis relative to the historic average. This is true, but not unprecedented or even unexpected given a decade of undersupply and given the existing housing market is frozen because of the rapid rise in rates.

(Click on image to enlarge)

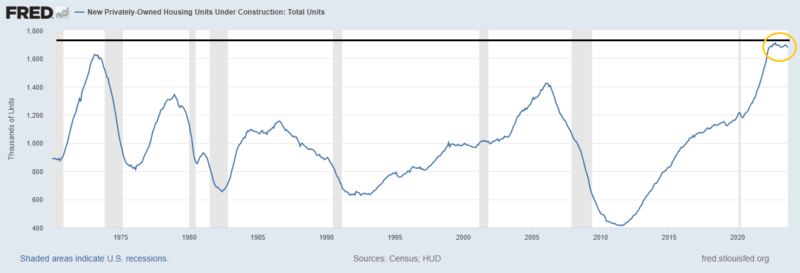

It is also true that all of the additional supply is currently under construction. This correlates to the good construction spending numbers we’ve had recently. Units under construction historically ahs been about 1,000,000 units. There are currently 1,676,000 being built.

(Click on image to enlarge)

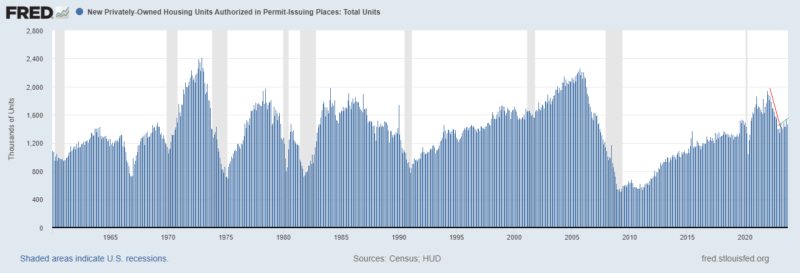

There were 1,473,000 annualized units permitted this month, about 100,000 above historic averages. Permits issued came down throughout 2022. They peaked in Dec 2021 at 1,948,000 annualized units, hit a recent low of 1,354,000 in Jan 2023, and hit a high for the year last month at 1,541,000. Based on permits issued, it does appear that the pace of construction will be easing slightly in the near future. We’ll see how much demand there is for the new units. If the supply is well received, then, in a Swifty manner, builders gonna build, build, build. If not then we may see some easing in rents which will continue to help bring CPI down. And, there is certainly a probability of some sort of outright deflation, but this would not be the base case at this time as I’ve been reading from some.

(Click on image to enlarge)

More By This Author:

Macro: Sept Industrial ProductionThe Happiest Workers Are 65 And Older

Macro: September Retail Sales

Comments

Log in or sign up to join the conversation.