Market Analysis

The USDA’s upcoming crop & supply/demand updates on September 11 will be highly anticipated. This summer’s WCB dryness, a recent jump in rainfall west of the Mississippi River, and the USDA announced that it would utilize the current FSA sign-up levels in their September crop updates (one month earlier than normal) because higher reporting levels have added to the trade’s uncertainty about the upcoming USDA report. Recent trips across N IL & to the Farm Progress Show in Decatur IL revealed to us the fast maturity of the crop in the northern quarter of IL, Plus, C IN’s dryness the past 30 days has tempered our yield ideas for these 2 states, The USDA’s 10-state field samples will be our first widespread hard data this crop year.

Image Source: Unsplash

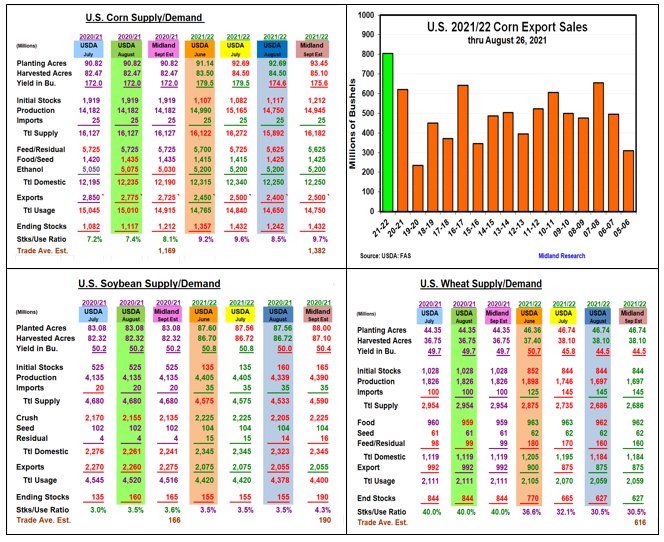

In corn, the trade is expecting a 600,000 higher harvested area led by the western Midwest which is the same as our estimate. The trade’s September yield of 175.8 bu is 1.2 bu higher than last month producing 14.942 billion bu crop. This is also similar to our 2021 crop outlook, The high cost of cash corn has prompted many ethanol plants to slow their output after mid-summer & overseas buyers to switch their purchases to the new crop. This may slice 95 million bu. off old-crop demand upping corn’s carryover to 1.212 billion bu. China’s earlier 2021/22 buys have pushed new-crop exports to a record late August 805 million level. Brazil’s recent slowing of their corn exports has us projecting a modest 1.432 billion rise in stocks this month. Overall, no change in the 2021 soybean harvested area is expected by the trade vs our 380,000 higher estimates. We are expecting a 0.4 higher yield to 50.4 bu, similar to the trade, which could up bean’s output by 51 million bu to 4.39 billion. The US domestic crush has stagnated the past few months. However, overseas shipments have held together so beans’ ending stocks will likely be up just 5 million to165 million. With limited new-crop demand changes, a slightly higher 190 million 2021/22 ending stocks is expected. With no US wheat crop changes normally until Sept 30 Small Grain Report, no adjustments in our US S&D levels.

What’s Ahead

Given 2021’s erratic US growing season with the ECB receiving more timely rains while the WCB experienced stress from drought, particularly in the Dakotas, the USDA’s upcoming Sept 10 crop report will be highly influential to prices. China’s export purchases in the 2021/21 crop year will also be highly impactful to price. Hold new-crop sales at previous 20-25% levels for now.

Comments

Log in or sign up to join the conversation.