The BoJ decision to widen the YCC band was a surprise in the sense that it's been viewed as a “when, not if” matter (while still messaging quite “dovishly” in the press conference, with Kuroda going out of his way to message repeatedly that this was not policy tightening, as they did not raise short-term policy rates nor adjust the monetary base target).

Markets knew the BoJ eventually had to true-up the 10Y point with the rest of the JGB curve and fundamentals... and eventually, begin a gradual policy alignment with the rest of the world’s already robust tightening, as they had instead continued to ease throughout ‘22...

Nonetheless, most everybody expected this move to come after the Kuroda term ended in April ‘23, with most expecting a “phase-in” executed in smaller increments over time.

But, as Bloomberg macro strategist Simon White, details below, the yen, not USTs, stands to be the main adjustment mechanism for the BOJ’s policy shift, with the currency facing potentially significantly more upside, but the rally in USTs remaining intact for now.

This time of year is replete with “Top Christmas Films” lists, but one festive movie we’ve seen before is the BOJ surprising markets in December. They have not disappointed this year, announcing today they would widen the trading band in the 10-year JGB to -0.5% to +0.5%.

It was a matter of when, not if, we would see this change: a policy that involves buying unlimited JGBs -- when the BOJ already owns more than half of the market -- to keep the 10-year yield artificially low when rates are rising across the rest of the world, would always eventually have to face its own inherent contradictions.

Japan is a net capital exporter, so to appreciate the net effects of such a change, understanding the likely behavior of Japanese investors in foreign assets is key. In a nutshell, rising short-term US yields as the Fed raised rates has made USTs increasingly unattractive to them after FX hedging costs.

Adjusting the net yield pick-up for Japanese buyers of USTs by US and Japanese inflation gives a close leading relationship with USDJPY. This has dropped precipitously this year, and if the relationship continues to hold, USDJPY annual growth would fall to 5-10% in the next six months or so, taking USDJPY down to the 115/120 level.

Rising yields on JGBs (the 10-year has risen to 0.4% from 0.25% today) will pressure more Japanese capital to return home, or not leave the country in the first place.

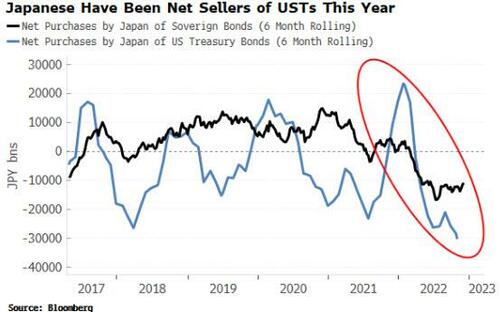

But this will not likely be enough to unseat the rally in USTs. First of all, Japan investors have been net sellers of Treasuries for most of this year, even as Treasuries have rallied.

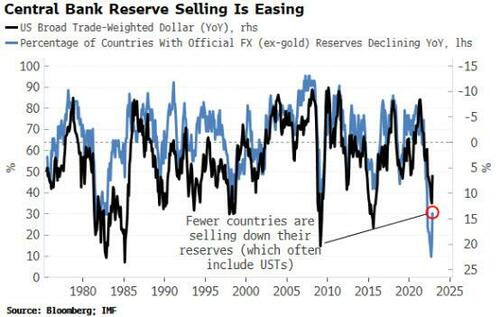

Secondly, the tailwinds for USTs I noted in October that would likely trigger a rally are still valid. The Fed’s hawkishness has very likely peaked for now; rising recession risk is likely to spur haven demand next year; while central-bank reserve selling (mostly USTs), which had reached extreme levels, is abating as easing commodity prices takes pressure off commodity importers (including Japan).

Treasuries also remain historically oversold and positioning is very net short, while seasonality continues to be favorable.

Finally, Nomura's Charlie McElligott points out that there is also an authentic “macro story” reality here on the YCC move from the BoJ, which is that prices are higher with growth also above trend, while too, inflation expectations continue to rise, which is why Yen (stronger) in my eyes was the best way to play “Short USD” in 2023...although this move happening ahead of schedule now takes some of the luster out of remain risk / reward in the trade, as this was the “easy part”.

-

The next incremental YCC adjustment after this initial move becomes more difficult, because with the Fed nearing the end of their policy tightening, UST yields have stopped going meaningfully higher - so a “unilateral” move higher in JGB yields from additional YCC adjustment risks a more “unruly” market impact.

-

From here on the currency side, any $Yen potential for 120-130 and beyond is likely a waiting-game on the US recession, likely requiring a Fed messaging pivot towards outright “policy easing / rate cutting” to get that “rates differentials” kicker to take the Yen strengthening to relative overdrive.

The biggest question now is whether this Yen strength and domestic bond market yield “pick-up” will see repatriation back home from many Japanese investors out of foreign bond markets, who since NIRP began in early 2016, have moved large amounts of money into overseas fixed-income.

This should be bullish for Japanese banks and insurers, and yet shouldn’t come close to hurting Corporate Japan, as the 25bps in the scheme is relatively negligible - I’d be a buyer of upside in Japan Equities / TOPIX Banks through options on this pullback, bc it’s a positive “nominal growth” story.

More By This Author:

These Are The World's Most Expensive Cities

Oil Exports From Key Russian Port Cut In Half As Price Cap Kicks In

Green Vs Green: Endangered Flower May Wipe Out Nevada Lithium Mine

Comments

Log in or sign up to join the conversation.