After a frenzied week that saw not just the US slide into technical recession just hours after the Fed hiked rates by a whopping 75bps for the 2nd time in a row (hence accelerating the US slowdown), as well as record bonanza of corporate earnings, markets still won't get the chance with US payrolls on Friday, followed by CPI on Wednesday 10th. If nothing out of the ordinary occurs in these two prints though maybe we can have a quiet two or three weeks according to DB's Jim Reid, who however notes that if payrolls are far from consensus and/or CPI is strong then "we may have some fun and games in August. It’s a month of low liquidity and if something big happens it can be multiplied in such thin trading."

Outside of payrolls, the other most important events this week include the manufacturing PMIs and ISM today, the RBA decision and US JOLTS tomorrow, services PMIs and ISM Wednesday, and the likely biggest hike from the BoE for 27 years alongside the increasingly important US jobless claims data on Thursday. Apart from that, earnings are still coming from all directions, but we are past halfway in the US with over 260 companies having reported. It’s 232 in the Stoxx 600. It might be hard to eclipse the big US tech week last week though. The other thing to look out for is whether US House Speaker Pelosi visits Taiwan this week on her Asian trip. It could set off a major geopolitical incident if she does and domestic accusations of backing down to China if she doesn't given she'd previously said she would visit.

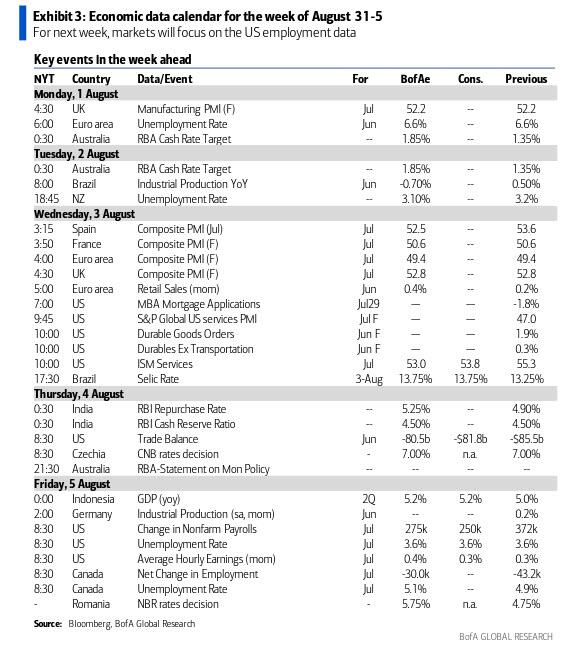

The full day-by-day week ahead is at the end as usual on a Monday but let's preview the main highlights in detail with the big one being payrolls of course.

(Click on image to enlarge)

The median strategist expects a 250k reading for nonfarm payrolls (down from 372k in June) and for unemployment rate to remain flat at 3.6%. DB economists think the gradual increase in continuing claims since last month is enough to slow the pace of job growth. Remember Jim Reid recently did a CoTD on payrolls day last month showing that the first month of a recession on average has a negative payroll print whereas the months leading up to it don't (including R-1). See here for a reminder. This is one of the main reasons Reid and DB don't think we're there yet in terms of a recession (but will be soon). The bank's favored measure of the strength of the labor market has been the JOLTS data which next comes out tomorrow for June. The problem is that it is always one month behind other data. However it gives us a decent if slightly rear-view mirror look at job openings and labor market tightness.

Moving on, the BoE's decision on Thursday will be a big event with consensus expecting a +50bps move, which will take the Bank Rate to 1.75% and become the largest single increase since 1995. It will likely also be accompanied by somewhat hawkish economic forecasts from the Bank.

Before the BoE, economists expect the RBA to also hike +50bps tomorrow. Regarding policy guidance, they expect the central bank to reiterate the need for higher interest rates, which would implicitly keep another +50bps hike in September among the options.

Turning to corporate earnings, this week's line-up will feature a number of important commodities companies, including BP, Occidental Petroleum (tomorrow), ConocoPhillips and Glencore (Thursday). Travel & leisure firms like Marriott, Airbnb (tomorrow) and Booking (Wednesday) will be in the spotlight as well to assess trends in consumer spending on services. Notable carmakers reporting results will include Toyota (Thursday), BMW (Wednesday) and Ferrari (tomorrow). In healthcare, investors will be focused on Regeneron, Moderna (Wednesday), Eli Lilly, Novo Nordisk and Bayer (Thursday). Other notable reporters will include Advanced Micro Devices, PayPal (tomorrow), Maersk (Wednesday) and Alibaba (Thursday).

Day-by-day calendar of events:

Monday August 1

- Data: US July ISM index, China July Caixin manufacturing PMI, Japan July vehicle sales, Eurozone June unemployment rate, Italy July PMI, budget balance, new car registrations, June unemployment rate

- Earnings: HSBC, Heineken, Devon Energy, Activision Blizzard

Tuesday August 2

- Data: US June JOLTS report, July total vehicle sales, Japan July monetary base, UK July Nationwide house price index, Canada July PMI

- Central banks: RBA decision, Fed’s Bullard and Evans speak

- Earnings: BP, Caterpillar, Ferrari, Marriott, KKR, Uber, S&P Global, Occidental Petroleum, Electronic Arts, Gilead Sciences, Advanced Micro Devices, Starbucks, Airbnb, PayPal, Marathon Petroleum

Wednesday August 3

- Data: US July ISM services index, June factory orders, China Caixin July services PMI, Germany June trade balance, France June budget balance, Italy July services PMI, June retail sales, UK July official reserves changes, Eurozone June PPI, retail sales

- Earnings: AXA, Maersk, CVS Health, McKesson, Just Eat, Regeneron, Nintendo, BMW, Vonovia, Moderna, Booking, Fortinet, eBay, Telecom Italia, Robinhood

Thursday August 4

- Data: US June trade balance, Germany June factory orders, July construction PMI, UK July new car registrations, construction PMI, Canada June building permits, international merchandise trade

- Central banks: BoE decision, Fed’s Mester speaks, ECB publishes its Economic Bulletin

- Earnings: Alibaba, Eli Lilly, Toyota, Intercontinental Exchange, ConocoPhillips, Merck, Novo Nordisk, Bayer, Glencore, Cigna, Rolls-Royce, adidas, Cheniere, DBS, Apollo, Lyft, Expedia, Deutsche Lufthansa, Warner Bros Discovery, Vertex Pharmaceuticals, DoorDash, Atlassian, Amgen, Block, EOG, Kellogg, AMC

Friday August 5

- Data: US July change in non-farm payrolls, unemployment rate, average hourlyearnings, participation rate, June consumer credit, Japan June household spending, labour cash earnings, real cash earnings, leading and coincident index, Germany June industrial production, France Q2 private sector payrolls, wages, June trade balance, industrial and manufacturing production, Italy June industrial production, Canada July net change in employment, unemployment rate

- Central banks: BoE's Pill speaks

- Earnings: LSE group, Deutsche Post, Suncor, Allianz

* * *

Finally, focusing on just the US, Goldman notes that the key economic data releases this week are the ISM manufacturing report on Monday, JOLTS job openings on Tuesday, the ISM services report on Wednesday, and the employment situation on Friday. There are several speaking engagements from Fed officials this week, including remarks from Reserve Bank presidents Evans, Mester, and Bullard.

Monday, August 1

- 09:45 AM S&P Global US manufacturing PMI, July final (consensus 52.3, last 52.3)

- 10:00 AM Construction spending, June (GS -0.4%, consensus +0.2%, last -0.1%): We estimate construction spending decreased 0.4% in June.

- 10:00 AM ISM manufacturing index, July (GS 51.7, consensus 52.0, last 53.0): We estimate that the ISM manufacturing index declined by 1.3pt to 51.7 in July reflecting a drag from tighter financial conditions and the deteriorating economic outlook in Europe. Domestic manufacturing surveys were mixed in the month, but the ISM has been running a bit above our manufacturing survey tracker (+0.3pt to 52.1 in July).

Tuesday, August 2

- 10:00 AM JOLTS Job openings, June (GS 11,100k, consensus 11,000k, last 11,254k): We forecast job openings declined to 11,100k in June, reflecting a modest sequential softening in the high-frequency job openings data used in our nowcast of the jobs-workers gap.

- 10:00 AM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will participate in an on-the-record breakfast conversation with reporters. In his last public appearance on June 22, Evans said, “I think that by the end of the year, we’ll be doing 25s [bp]” and “I expect it will be necessary to bring rates up a good deal more over the coming months in order to return inflation to the Committee's 2% average inflation target.” Regarding inflation, he said, “I think there are risks, but we have to take the steam out of inflation” and “I have hoped before a few times [inflation] could be transitory. We can't afford to be fooled again by this.” He added that he expects inflation “will cool substantially over the next couple of years.”

- 11:00 AM New York Fed Releases 2Q Household Debt and Credit Report

- 01:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will participate in a Washington Post live interview. In her last remarks on July 13, Mester called the June CPI report “uniformly bad”. She said, “There was no good news in that report at all. We at the Fed have to be very deliberate and intentional about continuing on this path of raising our interest rate until we get and see convincing evidence that inflation has turned a corner.” She added, “Right now, job one for us is to get inflation under control, and I say that knowing that the risks of recession have gone up…If we don’t do this right we’re going to have many more problems in the economy going forward.”

- 05:00 PM Lightweight motor vehicle sales, May (GS 13.3mn, consensus 13.5mn, last 13.0mn)

- 06:45 PM St. Louis Fed President Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will discuss the economic and policy outlook at an event with the Money Marketeers of New York University. Text and audience Q&A (no media) are currently expected. On July 15, Bullard noted, “I would now say that we may have to try to hit [a funds rate of] 3.75 to 4% by the end of 2022.” He said, “It probably doesn't make too much difference to do 100 basis points here and less in the other three meetings of this year, or to do 75 basis points here and slightly more in the remaining three meetings for the year.” He added that inflation “has come in broader and hotter than previously had been expected…But we've got the right policy to bring it back to 2% in a relatively short timeframe, and I would say something like 18 months.”

Wednesday, August 3

- 09:45 AM S&P Global US services PMI, July final (consensus 47.0, last 47.0)

- 10:00 AM Factory orders, June (GS +1.2%, consensus +1.0%, last +1.6%); Durable goods orders, June final (consensus +1.9%, last +1.9%); Durable goods orders ex-transportation, June final (consensus +0.3%, consensus +0.3%); Core capital goods orders, June final (last +0.5%); Core capital goods shipments, June final (last +0.7%): We estimate that factory orders increased 1.2% in June following a 1.6% increase in May. Durable goods orders increased 1.9% in the June advance report, and core capital goods orders increased 0.5%.

- 10:00 AM ISM services index, July (GS 53.3, consensus 53.7, last 55.3): We estimate that the ISM services index declined by 2pt to 53.3 in July, reflecting a sentiment drag from tighter financial conditions and sequential weakness in the real estate market. Our non-manufacturing survey tracker decreased 2.6pt to 51.3.

Thursday, August 4

- 08:30 AM Trade balance, June (GS -$79.5bn, consensus -$80.0bn, last -$85.5bn): We estimate that the trade deficit decreased by $6.0bn to -$79.5bn in June, reflecting an increase in exports.

- 08:30 AM Initial jobless claims, week ended July 30 (GS 260k, consensus 260k, last 256k); Continuing jobless claims, week ended July 23 (consensus 1,338k, last 1,359k): We estimate initial jobless claims increased to 260k in the week ended July 30.

- 12:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will discuss the economic and policy outlook at an event hosted by the Economic Club of Pittsburgh. Audience Q&A is currently expected.

Friday, August 5

- 08:30 AM Nonfarm payroll employment, July (GS +225k, consensus +250k, last +372k); Private payroll employment, July (GS +175k, consensus +230k, last +381k); Average hourly earnings (mom), July (GS +0.3%, consensus +0.3%, last +0.3%); Average hourly earnings (yoy), July (GS +4.9%, consensus +5.1%, last +5.1%); Unemployment rate, July (GS 3.6%, consensus 3.6%, last 3.6%); Labor force participation rate, July (GS 62.2%, consensus 62.2%, last 62.2%): We estimate nonfarm payrolls rose by 225k in July (mom sa), a slowdown from the +372k pace in June. The July seasonal factors have evolved significantly more restrictive—even more so than in June—and the seasonal adjustment software may be overfitting to the reopening-related job strength in the summers of 2020 and 2021. We assume seasonal headwind of roughly 250k in our forecast. Additionally, while Big Data indicators were mixed in the month, jobless claims have risen, consistent with a drag from tighter financial conditions and modestly higher retail and technology layoffs. On the positive side, we expect a boost from education seasonality, reflecting fewer-than-normal janitors and support staff leaving for the summer (we assume +75k mom sa, public and private).

- We estimate an unchanged unemployment rate at 3.6%, reflecting flat-to-up labor force participation and a rebound in household employment, the latter of which does not exhibit the same negative residual seasonality we expect in nonfarm payrolls. We estimate a 0.3% rise in average hourly earnings (mom sa) that lowers the year-on-year rate by two tenths to 4.9%. The arrival of the youth labor force may have eased some of the upward pressure on wages, but we expect a boost from positive calendar effects.

Source: DB, Goldman, BofA

More By This Author:

Enough With The Focus On Jobs: They Will Tell You Nothing About The Recession

Biden Nemesis Exxon Reports Record Earnings As Company Prints $20 Billion In Cash

Amazon Soars After Smashing Top-Line Expectations Thanks To Solid AWS, Blows Away Guidance

Comments

Log in or sign up to join the conversation.