The pandemic, inflation, supply chain frictions, and policy tightening by central banks remain the central drivers of the economy and markets across the world in 2022. In our pint-sized January update, we look at how these themes are likely to play out.

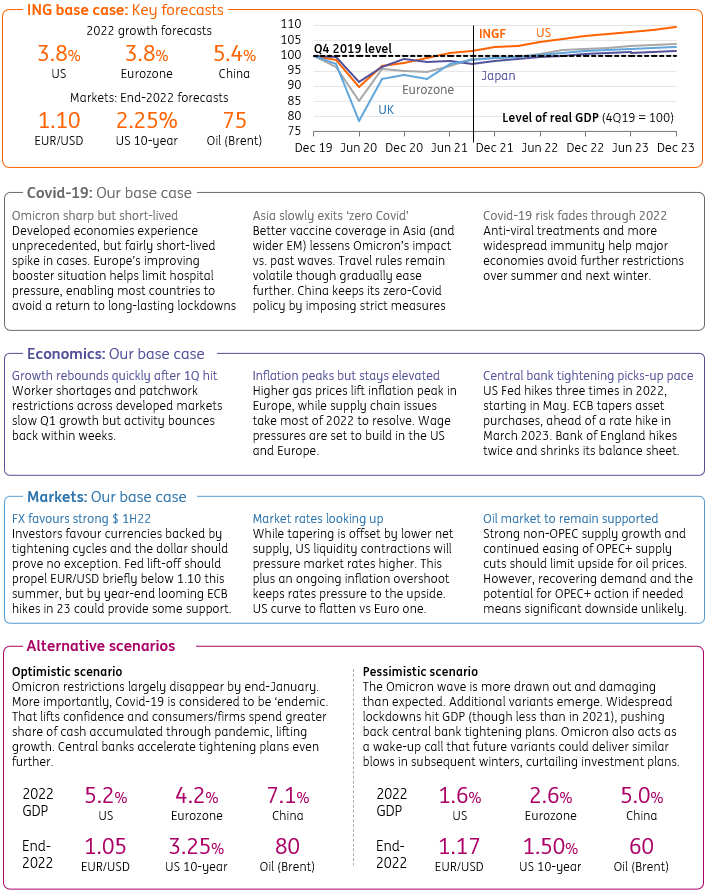

ING's three scenarios for the global economy and markets

Source: ING

At a glance: the world right now

Happy New Year to all of you. As we are all slowly and gradually returning from holiday, our macro-economic year starts with a very light update and forecasts. Luckily, we were not completely wrong with our big outlook pieces at the end of last year which would require us to give you a fresh overhaul of our predictions in January. The big themes for 2022 are still the same: virus, inflation, supply chain frictions, and the grand policy rotation with central banks exiting ultra-loose monetary policies and governments shifting towards longer-term fiscal stimulus.

As the world continues to face the Omicron wave, even newer variants are emerging indicating that life without the virus will hardly happen this year. As for Omicron, it's becoming clear that it's much more contagious than previous variants but its health implications, particularly for triple vaccinated people, seem to be much milder. However, this is not where it stops. A surge in infections and subsequent quarantine and sickness leave could aggravate existing labor shortages and add to pressure in systemic-relevant sectors; remember that a particularly bad flu wave in Germany in 2015 shaved off some 0.3 percentage points of quarterly GDP growth.

Governments in most industrialized countries are trying to avoid a fully-fledged lockdown so keeping the economic damage more limited than during previous waves; Omicron is likely to test Asia's zero-COVID strategy. I hate to use a trite remark but even if Omicron is not the negative gamechanger some feared in the wake of virus exhaustion, things could still first get (economically) worse before they get better in the European spring.

As for inflation, the first days of the new year will show whether headline numbers in the US and the eurozone really peaked at the turn of the year. We still think they did but this does not automatically mean we have entered a period of constantly dropping inflation rates. On the contrary, the pass-through from higher energy and producer prices is still in full swing and we should expect inflationary pressures to broaden across more sectors, even if headline inflation comes down somewhat.

Volatility in gas prices is a big concern for European households in the short run, while the energy transition could lead to more inflationary pressure in the medium term. It, therefore, does not come as a surprise that the economic world is currently in a heated debate about possible price controls. As so often with economists, the range of views on this topic is wide and extreme. However, if and when inflation continues to remain high, expect the topic of price controls again to enter the political arena. It would be the next step in the mix-up between fiscal and monetary policy if politics starts mingling with inflation after central banks for so many years have been crisis fighters, often stretching their own mandates.

As much as all of us would have liked to start the new year on a purely positive note, the reality is that the well-known challenges for the global economy didn't simply disappear over Christmas. On the 20th anniversary of the first Harry Potter movie, only too much binge-watching of magic wands could have led to the idea that 2022 will bring nothing but blue skies. But there is hope. Even if the first quarter brings more disappointment, we stick to our view that the global economy will take off in the spring and that the topics at the Christmas and 2022 New Year’s celebrations will no longer exclusively be about the virus and vaccines. Just hang on in there.

US is preparing for first rate hike in 2Q

The Omicron wave sweeping across the US and the consumer caution resulting from that has led us to cut our forecast for 1Q 2022 GDP to just below 1.5% from a little above 4%. In addition, increased worker absences mean more bottlenecks and supply chain strains that will hamper economic activity and keep price pressures intense through the first half of the year.

The hope is that Omicron soon fades and we see growth re-accelerate in 2Q although delays (and the prospect of further cuts) to the Build Back Better plan argue for a slightly weaker medium-term growth profile than we had previously penciled in. Nonetheless, we still see the economy expanding 3.8% this year with inflation averaging close to 5%. Given this situation, the Federal Reserve’s “dot plot” of forecasts that projects three rate hikes in 2022 and three more in 2023 seems fair. We favor 2Q as being the starting point.

Chinese New Year will be more vivid than in 2021

COVID is spreading in Xi’an, which is located in the central region of China. The economic impact has been limited so far as the city is more of a tourist destination than a manufacturing hub. However, the Omicron threat should lead to some travel restrictions during the upcoming Chinese New Year. We expect the movement of people to be above levels seen during the 2021 New Year break but still below the pre-COVID level. With more travel, spending should also be above levels seen last year.

Manufacturing and export activities will be limited from now to the end of the Chinese New Year. This is a normal pattern. Due to longer freight times, we expect export orders for Easter to be placed right after the Chinese New Year holiday.

The main risks to the outlook are real estate developers’ repayments and a surge in Omicron infections. Regarding the former, the central government has lined up some developers to see if M&A can help Evergrande (EGRNF), which raises the possibility that a bond due in January may not be repaid.

Eurozone sees stalling growth with higher inflation

The fourth-quarter slowdown in the eurozone (EZU) is likely to continue in the first quarter of 2022, potentially dragging quarterly growth down to close to zero. The more contagious Omicron variant has pushed the infection rate up to the highest level since the start of the pandemic. While we don’t think that lockdown measures will be tightened further, growth is still likely to be hampered by a rising proportion of workers on sick leave.

The worldwide increase in COVID-19 infections might also temporarily worsen supply chain problems again. However, we stand by our scenario of an acceleration in growth from 2Q onwards, leading to 3.8% GDP growth in 2022. While inflation is still likely to drop just below 2% in 4Q 2022, we've again had to revise up the near-time outlook on the back of high energy prices, yielding an average 2.9% headline inflation rate for the year. With some second-round effects likely to kick in over the coming years, we pencil in a slow upward trend for core inflation, with 2% now clearly in reach in the medium term. That will set the scene for a first rate hike in March 2023.

Rest of Asia is facing the Omicron wave

The COVID-19 pandemic remains the largest source of forecast risk for the Asia-Pacific (APAC) region. Vaccine rollout in APAC has come a long way after a disappointingly slow start in 2021. But the Delta variant has shown that there are still gaps in existing vaccines’ armor even where there are high rates of vaccination. Omicron could test this still further, especially in the three relatively low vaccination rate countries of India, Indonesia and the Philippines, leaving them vulnerable to a sharp rise in severe infections that could threaten the capacity of local healthcare. The apparent lower efficiency of the Sinovac vaccine against Omicron could put zero-COVID strategies to the test.

More encouragingly, Asia remains largely unaffected by the inflation surge that is fueling monetary policy normalization expectations in other parts of the world. While Japan is an extreme example of persistent low inflation in the region, even the higher inflation countries within APAC are showing far fewer signs of a trend increase than their European or North American counterparts. Related to the inflation story, supply chain constraints in Asia are ebbing away with strong manufacturing production in recent months.

Higher UK inflation pushes BoE towards further rate hikes

Higher gas prices mean that UK inflation is now set to peak above 6% in April, and probably stay above 4% until late 2022. Admittedly, the medium-term picture hasn’t changed much – inflation is set to fall back in 2023, while wage pressures appear to have calmed a little after last year’s re-openings. But we know from December’s surprise rate hike decision that the Bank of England is wary about high rates of inflation and the feed-through to expectations. We think it’s a close call whether policymakers hike again in February, but for now, we narrowly favor a May move. That will allow more time to assess Omicron’s damage, though the hit to growth is unlikely to be huge. Staff shortages are rife, but new restrictions have largely been avoided, while any hit to consumer confidence is set to be short-lived.

CEE ahead of the curve of central bank tightening

The Polish economy remained strong in the fourth quarter of last year despite the fourth wave of the pandemic, with GDP growth expected to come in at 1.3% quarter-on-quarter. The manufacturing sector performed very well, presumably together with the stronger eurozone production, benefiting from a small window of lifted restrictions in Asia between Delta and Omicron. Headline inflation is expected to remain high, possibly denting household spending in 2022 and also pushing the central bank to further hike interest rates. We have lifted our forecast of the National Bank of Poland rate to 4% in 2022 and 4.5% in 2023.

Central bank policy rate hikes are a common theme in all central and eastern European countries, with the Czech central bank having hiked the main policy rate by 100bp to 3.75% in December with more to come, and monetary policy in Hungary also being tightened in December. In Hungary, the key interest rate (weekly deposit rate) is currently at 4.00%. As a result of central bank tightening, CEE currencies appreciated in December and at the beginning of 2022.

Rates do look up

The big question as we enter 2022 is whether the robust demand for core low-yielding bonds, seen through much of 2021, is sustained. If it is, it can again mute the potential upside for yields, just as it did in 2021. That said, despite such persistent core bond buying in 2021, the US 10yr still rose by 60bp and the German 10yr by 40bp. One of the key protagonists here, the Federal Reserve, will end its bond buying as it tapers to zero by the end of the first quarter.

The European Central Bank will also ease up through 2022 as a whole, but at a slower pace. At the same time, there will be lower net supply in 2022 as fiscal deficits shrink, both in the eurozone and in the US. That, in fact, broadly balances the taper effect, meaning that more dominant directional effects come from elsewhere, probably liquidity conditions, inflation and policy rates. With inflation remaining high, at least in the first half of the year, and major central banks starting or at least preparing first rate hikes, upward pressure on bond yields should remain.

FX - Dollar should stay strong in 1H22

The start of 2022 has seen a strong performance by those currencies backed by central banks prepared to pull the trigger on rate increases. Sterling (FXB) is the standout in the G10 space, while the CE3 currencies are extending gains in emerging markets.

We would expect the dollar (UUP) to stay strong through the first half of the year as the Fed prepares to pull the trigger in 2Q and the market starts to price the terminal US policy rate closer to 2%. Additionally, a mixed global risk environment should prevent the kind of broad-based flows into emerging markets, which can occasionally weaken the dollar. Our call is that EUR/USD briefly trades below 1.10 this summer, but could find support into year-end, ahead of the 2023 ECB rate hike (FXE).

Authors: Carsten Brzeski, James Knightley, Iris Pang, Peter Vanden Houte, Robert Carnell, James Smith, Chris Turner, Padhraic Garvey, Rafal Benecki

Comments

Log in or sign up to join the conversation.