Increasing Speculation In “Paper Gold”

An increase in the amount of gold bullion held by GLD (the SPDR Gold Shares) and other bullion ETFs does not cause the gold price to rise. The cause-effect works the other way around and in any case the amount of gold that moves in/out of the ETFs is always trivial compared to the metal’s total trading volume. However, it is reasonable to view the change in GLD’s gold inventory as a sentiment indicator.

Ironically, an increase in the amount of physical gold held by GLD and the other gold ETFs is indicative of increasing speculative demand for “paper gold”, not physical gold. As I’ve explained in the past (for example, HERE), physical gold only ever gets added to GLD’s inventory when the price of a GLD share (a form of “paper gold”) outperforms the price of gold bullion. It happens as a result of an arbitrage trade that has the effect of bringing GLD’s market price back into line with its net asset value (NAV). Furthermore, the greater the demand for paper claims to gold (in the form of ETF shares) relative to physical gold, the greater the quantity of physical gold that gets added to GLD’s inventory to keep the GLD price in line with its NAV.

Speculators in GLD shares and other forms of “paper gold” (most notably gold futures) tend to become increasingly optimistic as the price rises and increasingly pessimistic as the price declines. That’s the explanation for the positive correlation between the gold price and GLD’s physical gold inventory illustrated by the following chart.

Now, speculation in “paper gold” is both an effect of the gold price and an important short-term driver of the gold price. It is therefore fair to say that although changes in GLD’s gold inventory don’t cause anything, they often reflect changes in speculative sentiment that at least on a short-term basis do have a significant influence on the gold price. At the same time it is also fair to say that the influence of speculative buying/selling in the futures market is vastly greater (probably at least an order of magnitude greater) than the influence of speculative buying/selling of GLD shares. Refer to “The scale of the gold market” for details on relative size an influence.

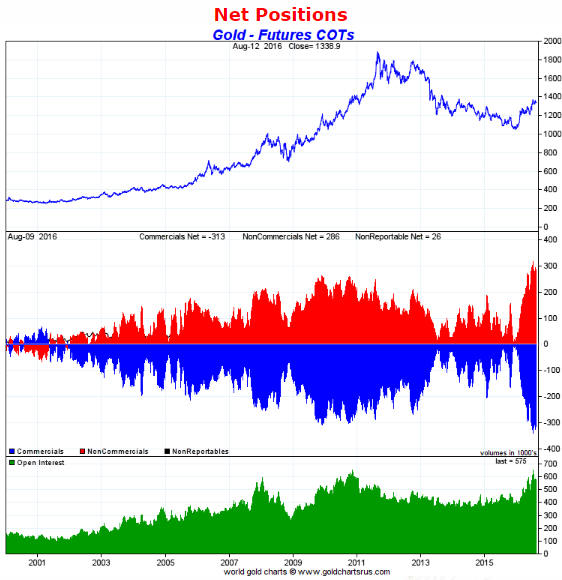

The speculative demand for “paper gold” has certainly ramped up over the past several months. This is partly reflected by the increase in the GLD inventory shown on the above chart, but it is primarily reflected by the rise to an all-time high in futures-related speculation. This is illustrated below.

Chart source:

The extent to which short-term speculators are bullish on gold is a risk. An unusually-elevated level of speculative enthusiasm will never be the cause of a reversal in the price trend from up to down, but it will exacerbate the decline that happens after the price-trend reverses for some other reason.

Disclosure: None

"It is therefore fair to say that although changes in GLD’s gold inventory don’t cause anything, they often reflect changes in speculative sentiment that at least on a short-term basis do have a significant influence on the gold price."

This conclusion seems a bit contradictory. How can a trivial (and questionable) amount of gold movement compared to the metal’s total trading volume be a reliable indicator of sentiment? I also find GLD's holdings to be highly questionable arbitrage or not. How reliable are GLD's holding reports? GLD does not give retail investors the right to redeem for any of its mystery physical gold holdings. This fact alone ensures the GLD shares to be nothing more than paper at the end of the day. GLD also has a glaring audit loophole in their prospectus that states they have no right to audit subcustodial gold holdings. To this day, I have not heard of a single good reason for the existence of this backdoor to the fund. Some other red flags I've stumbled upon, verified and welcome everyone else to verify for themselves:

"Did anyone try calling the GLD hotline at (866) 320 4053 in search of numerical details on GLD's insurance? The prospectus vaguely states "The Custodian maintains insurance with regard to its business on such terms and conditions as it considers appropriate which does not cover the full amount of gold held in custody." When I asked about how much of the gold was insured, the representative proceeded to act as if he didn't know and said they were just the "marketing agent" for GLD. What kind of marketing agent would not know such basic information about a product they are marketing? It seems like they are deliberately hiding information from investors.

I remember there was a highly publicized visit by CNBC's Bob Pisani to GLD's gold vault. This visit was organized by GLD's management to prove the existence of GLD's gold but the gold bar held up by Mr. Pisani had the serial number ZJ6752 which did not appear on the most recent bar list at that time. It was later discovered that this "GLD" bar was actually owned by ETF Securities."

I remember you reporting something like this last week on another GLD related article. I think that is some good DD you have done. And I agree, GLD is an electronic ownership of a paper certificate that marks you to the price of gold and little more.