Income, Education And Inequality In The "Recovery": Prepare To Be Surprised

Note to the higher education industry: issuing diplomas doesn't magically create new jobs in the real world.

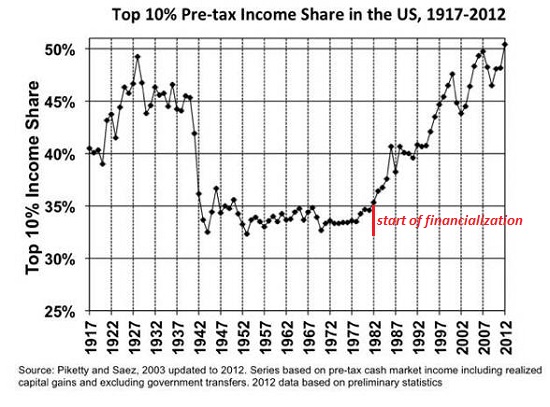

By virtually any standard, wealth inequality has soared to historic levels in the six years of "recovery" since the Great Recession of 2008-09. Economist Emmanuel Saez, who has long collaborated with Thomas Piketty, described the recent extremes of wealth inequality in a recent paper Striking it Richer: The Evolution of Top Incomes in the United States, which provides an in-depth look at the widening gulf between the top 1% and the bottom 90% from 2009 to 2012.

Here is a chart of the top 10% share of income, based on their research (the note in red marking the beginning of financialization in 1982 is my own):

As author David Cay Johnston noted in an insightful review of Piketty's book Capital in the Twenty-First Century, Trickle-Up economics: "The top 1 percent of Americans raked in 95 cents out of every dollar of increased income from 2009, when the Great Recession officially ended, through 2012. Almost a third of the entire national increase went to just 16,000 households, the top 1 percent of the top 1 percent, Piketty and Saez’s analysis of IRS data shows."

Inequality Has Actually Not Risen Since the Financial Crisis: We would naturally expect those with the highest incomes to have fared best in the past six years and those at the bottom to have fared the worst financially--but this not entirely true. Most income analyses, it turns out, do not factor in government-funded social welfare transfers, tax credits and entitlements. Once these sources of income are added, the bottom 90% saw no decline in income at all from 2007 to 2011, while the top 1% suffered a 27% decline and the top 5% took a 7% hit.

"Pretax income for the middle class and poor dropped substantially from 2007 to 2011 – about 10 percent for most groups. Yet including taxes and transfers, incomes fared better: Average income for the bottom fifth of earners rose 2.6 percent, to $24,100, and the average for the middle fifth fell only 2 percent, to $59,000. Such stagnation is hardly good news, but it’s a lot better than a large decline."

Taxes on higher-income households have risen on several fronts: a new tax on high-earners to fund ObamaCare, for example, and a higher tax bracket for the highest-income households.

Social welfare transfers and tax credits/cuts did what they were supposed to do--cushion the blow of recession for lower-income households and transfer more of the tax burden to higher income households. Yes, there are endless debates around the issues of taxes: for example, if most of the benefits of the Bush-era tax cuts flowed to the top income earners, then recent tax increases for the top income bracket are clawbacks rather than new taxes.

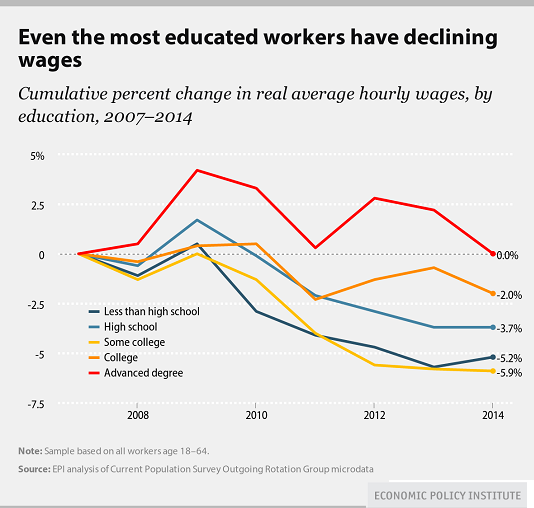

But setting aside the many debates on tax policies and sources of income inequality, another surprising data point has emerged: Even the Most Educated Workers Have Declining Wages (Economic Policy Institute)

The chart accompanying the article clearly shows less educated workers suffered larger wage declines than their more educated peers. The year-over-year data shows something else: "Some commentators are under the false impression that wage inequality is a simple consequence of employers’ demand for increased skills and education—often thought to be driven by advances in technology. But new data from 2014 shows that even college educated workers and workers with advanced degrees are not in demand enough to see their wages rise."

In other words, wages are declining even in fields where advanced degrees are supposed to inoculate the highly educated from declines in earnings. This is not entirely surprising to anyone who has first-hand knowledge of the tremendous glut in workers with advanced degrees, but it does drive a stake in the heart of the argument that the solution to income inequality is more education.

Ironically, all that minting another 5 million Masters degrees, MBAs, law degrees and PhDs will do is increase the oversupply of highly educated workers and thereby exacerbate the decline in wages paid to these workers.

As I often note, issuing diplomas doesn't magically create new jobs in the real world.

Disclosure: None

Thank you for the kind words.

Top incomes always fall the most in a recession because, statistically, the higher up you are there that comes from capital and the less from compensation for services. When the economy recovers these top incomes grow much faster than all others under current government rules.

In 2009, for example, the 400 highest tax returns averaged $202 million, but in 2010 they averaged $265 million or 31% more. Give the stock market performance when we get the 2011 through 2014 data I am sure it will show huge increases in top incomes.

Note: the 400 are not the highest incomes, only the 400 highest on tax returns. Congress lets many people -- executives, movie stars, top athletes, managers of hedge and private equity funds -- to defer reporting their economic incomes and their taxes for decades, as I have been explaining to my readers in many article and columns since Oct. 13, 1996.

A major problem with counting transfers is asymmetrical information, resulting in serious mismeasurements.

The government publishes detailed statistics on downward transfers, but none on the upward transfers. These upward transfers are so massive – and so concentrated among a small segment of the populace -- that I describe our national economic policy not as trickle down, but Niagara up.

How these stealth mechanisms redistribute upwards is explained in detail in my trilogy –Perfectly Legal, Free Lunch and The Fine Print.

You can read my detailed analyses of the latest official data on wages, total incomes and on the shrinking base of stock ownership in my columns dated Aug. 11, 18 and 25 and Oct. 23, 31 and Nov 6. All are available here: america.aljazeera.com/.../david-cay-johnston.html